Question: After completing a financial statement audit, the auditor needs to assess the situation to determine the proper type of report to issue. Expressing an independent

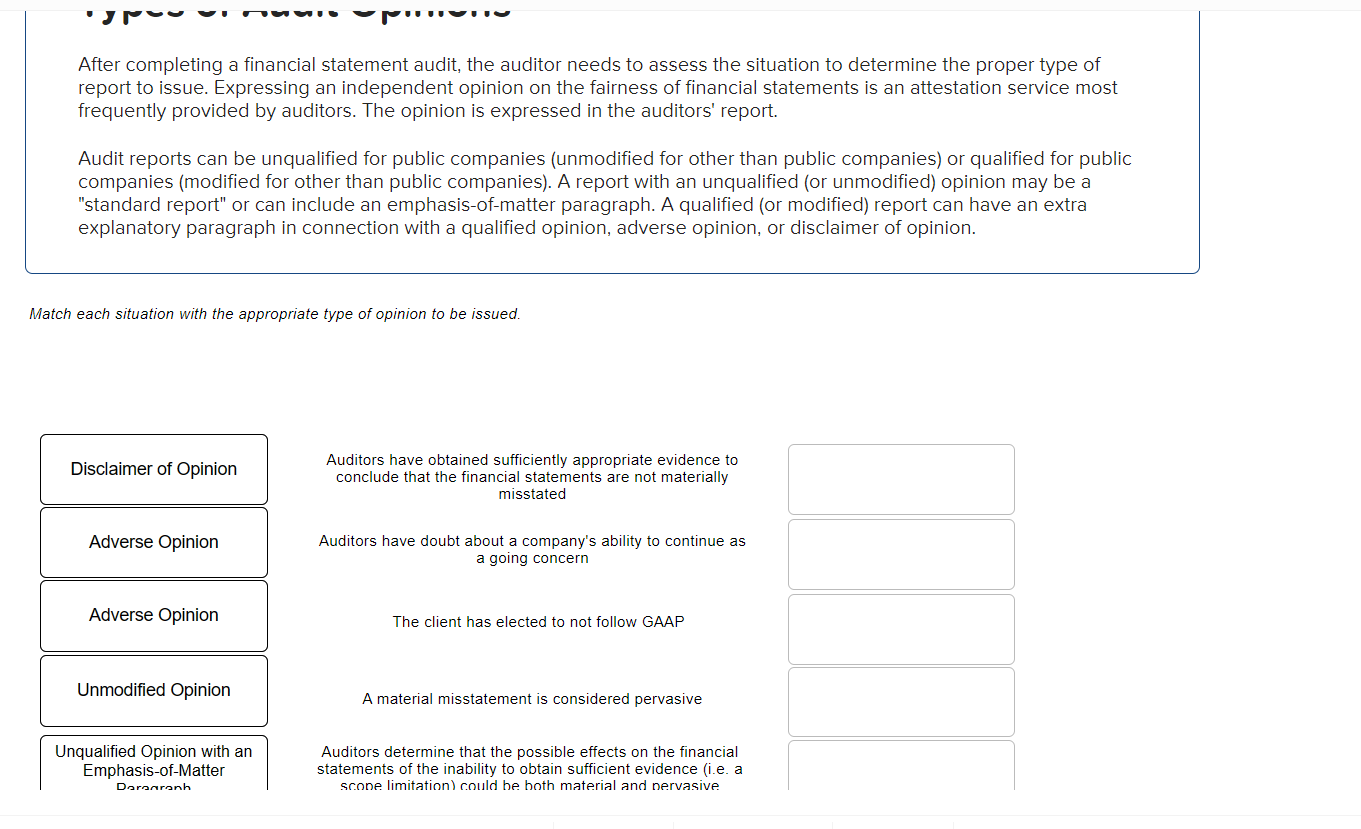

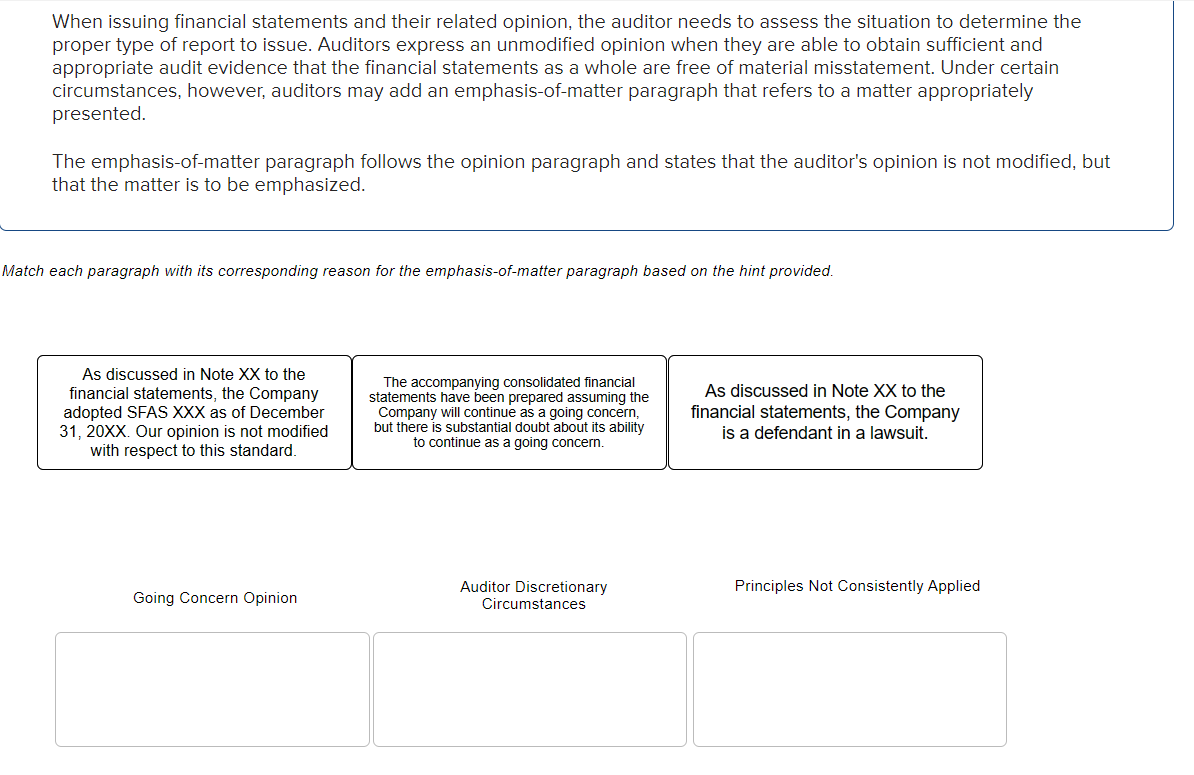

After completing a financial statement audit, the auditor needs to assess the situation to determine the proper type of report to issue. Expressing an independent opinion on the fairness of financial statements is an attestation service most frequently provided by auditors. The opinion is expressed in the auditors' report. Audit reports can be unqualified for public companies (unmodified for other than public companies) or qualified for public companies (modified for other than public companies). A report with an unqualified (or unmodified) opinion may be a "standard report" or can include an emphasis-of-matter paragraph. A qualified (or modified) report can have an extra explanatory paragraph in connection with a qualified opinion, adverse opinion, or disclaimer of opinion. Match each situation with the appropriate type of opinion to be issued. When issuing financial statements and their related opinion, the auditor needs to assess the situation to determine the proper type of report to issue. Auditors express an unmodified opinion when they are able to obtain sufficient and appropriate audit evidence that the financial statements as a whole are free of material misstatement. Under certain circumstances, however, auditors may add an emphasis-of-matter paragraph that refers to a matter appropriately presented. The emphasis-of-matter paragraph follows the opinion paragraph and states that the auditor's opinion is not modified, but that the matter is to be emphasized. Aatch each paragraph with its corresponding reason for the emphasis-of-matter paragraph based on the hint provided. As discussed in Note XX to the financial statements, the Company adopted SFAS XXX as of December 31,20XX. Our opinion is not modified with respect to this standard. The accompanying consolidated financial statements have been prepared assuming the company will continue as a going concern, but there is substantial doubt about its ability to continue as a going concern. As discussed in Note XX to the financial statements, the Company is a defendant in a lawsuit. Going Concern Opinion Auditor Discretionary Circumstances Principles Not Consistently Applied Principles Not Consistently Applied Circumstances

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts