Question: * * * * * ALL INFORMATION NEEDED IS IN THE PICTURE PROVIDED * * * * a . What is State Bank's repricing gap

ALL INFORMATION NEEDED IS IN THE PICTURE PROVIDED a What is State Bank's repricing gap if the planning period is six months? One year? Integrated Mini Case:

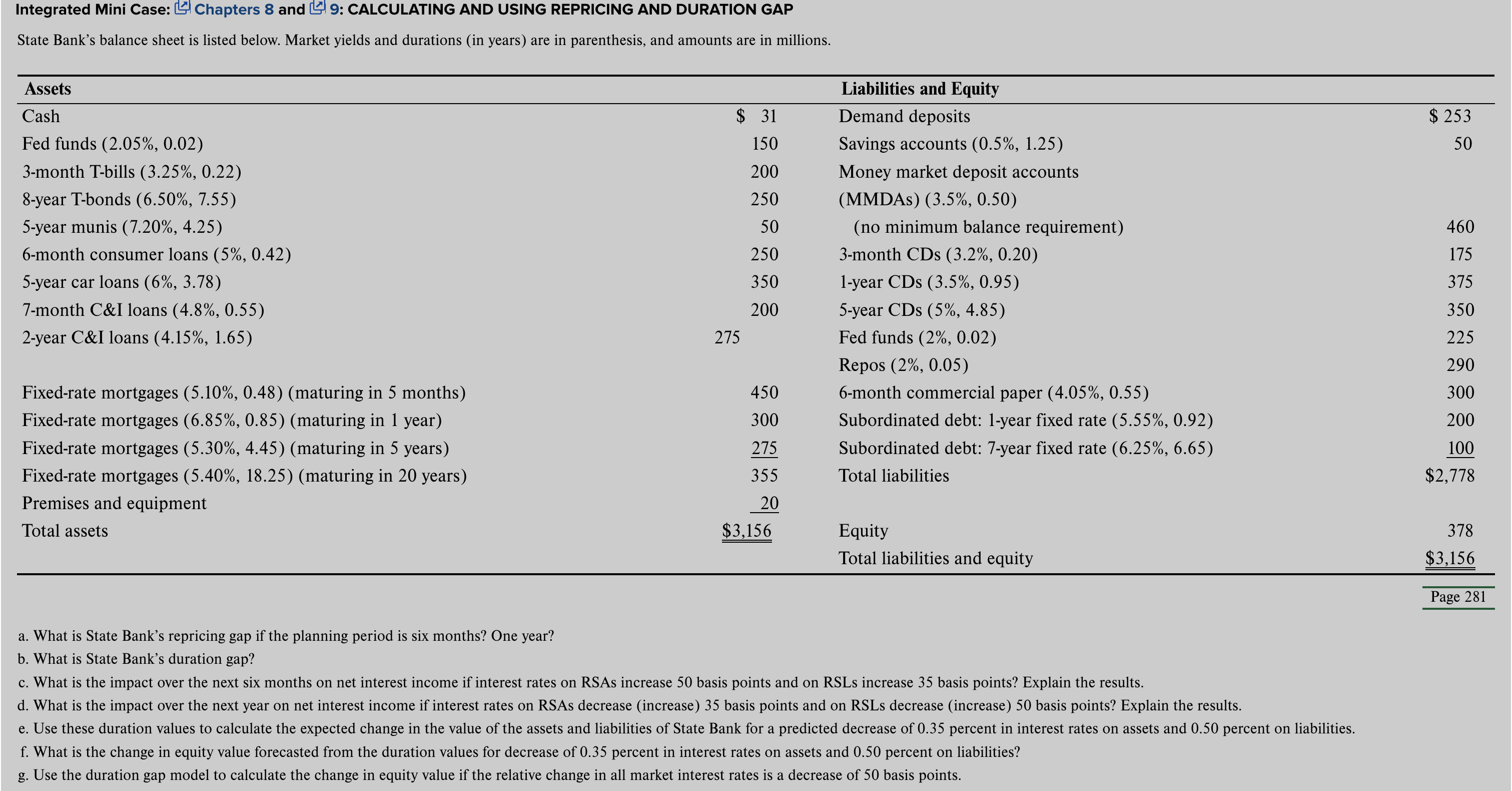

State Bank's balance sheet is listed below. Market yields and durations in years are in parenthesis, and amounts are in millions.

a What is State Bank's repricing gap if the planning period is six months? One year?

b What is State Bank's duration gap?

c What is the impact over the next six months on net interest income if interest rates on RSAs increase basis points and on RSLs increase basis points? Explain the results.

d What is the impact over the next year on net interest income if interest rates on RSAs decrease increase basis points and on RSLs decrease increase basis points? Explain the results.

e Use these duration values to calculate the expected change in the value of the assets and liabilities of State Bank for a predicted decrease of percent in interest rates on assets and percent on liabilities.

f What is the change in equity value forecasted from the duration values for decrease of percent in interest rates on assets and percent on liabilities?

g Use the duration gap model to calculate the change in equity value if the relative change in all market interest rates is a decrease of basis points.

b What is State Bank's duration gap?

c What is the impact over the next six months on net interest income if interest rates on RSAs increase basis points and on RSLs increase basis points? Explain the results.

d What is the impact over the next year on net interest income if interest rates on RSAs decrease increase basis points and on RSLs decrease increase basis points? Explain the results.

e Use these duration values to calculate the expected change in the value of the assets and liabilities of State Bank for a predicted decrease of percent in interest rates on assets and percent on liabilities.

f What is the change in equity value forecasted from the duration values for decrease of percent in interest rates on assets and percent on liabilities?

g Use the duration gap model to calculate the change in equity value if the relative change in all market interest rates is a decrease of basis points.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock