Question: all is there 3. Entimating the inputs using the Black-5choles option pricing model in the option analysis of the imvestment timing option Option analysis involves

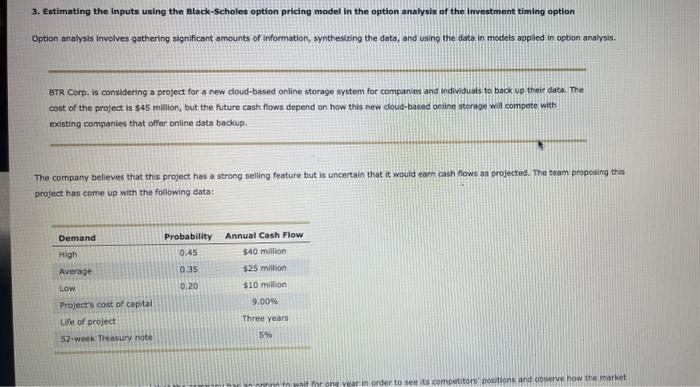

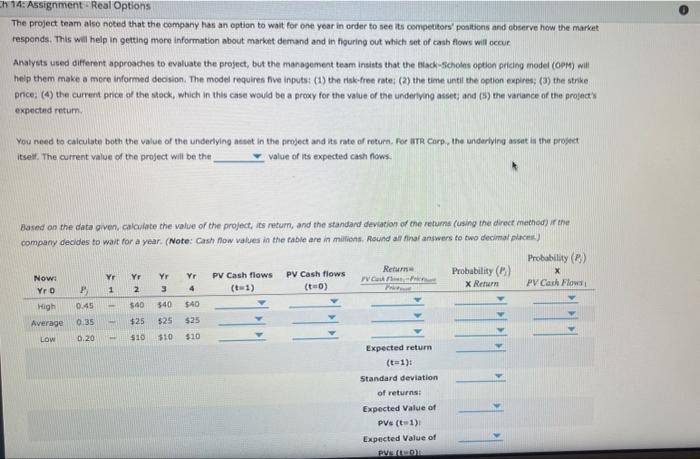

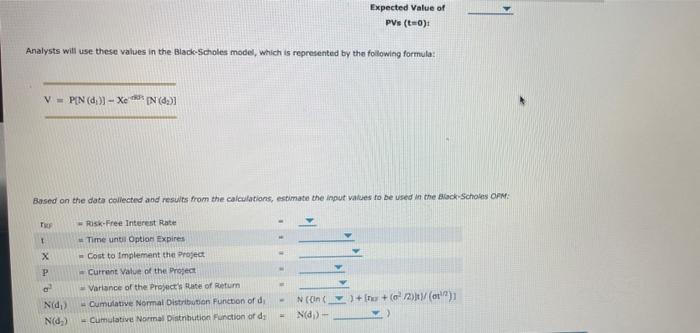

3. Entimating the inputs using the Black-5choles option pricing model in the option analysis of the imvestment timing option Option analysis involves gathering significant amounts of information, synthesiring the data, and using the data, in models appled in option analysis. BTR Corp. is considering a project for a new cloud-based online storage system for companies and individuals to back up theie data. That cost of the project is $45 million, but the future cash flows depend an how this new clodi-based online steraje wil compete with exasting companies that offer ontine data backup. The company believes that this project has a strong selling feature but is uncertain that it would earn cash flows as projected. The team proposing this project has come up with the following data: The project tearm also noted that the company has an option to wait for one yoar in order to see its competitors' positions and observe how the market responds. This wil help in getang more information about market dermand and in fouring out which set of cash flors will occur Analysts used different approaches to evaluate the project, but the man agement team insists that the atack=Gicholes option pricing model (Cop) will help them make a mere informed deoision. The model requires five inputs: (1) the riskofree rate; (2) the time until the option expires: (3) the strke price. (4) the current price of the stock, which in this case would be a proxy for the value of the underlying asset; and (b) the variance of the proledis expectand return. You need to caiculate both the value of the underlying aeset in the project and its rate of rotura. For itra Carp. the underiying asset is the progect itsel. The current value of the project will be the value of its expected cash flows: Dased on the data given. calculate che value of the project, iss retum, and the standand devlation of the retums (ising the direct mechod) ir the company decides to wait for a year. (Note: Cash flow valjes in the fable are in milishs, Round an finar answers to two decimal puceik) PVs(t=0)t Analysts will use these values in the Black-Scholes modes, which is represented by the following formula: V=P[N(d1)]Xe1shs[N(d2)] Based on the dath collected and results from the calculations, estimate the input values fo be used in the Blick-Scholas ofN: 3. Entimating the inputs using the Black-5choles option pricing model in the option analysis of the imvestment timing option Option analysis involves gathering significant amounts of information, synthesiring the data, and using the data, in models appled in option analysis. BTR Corp. is considering a project for a new cloud-based online storage system for companies and individuals to back up theie data. That cost of the project is $45 million, but the future cash flows depend an how this new clodi-based online steraje wil compete with exasting companies that offer ontine data backup. The company believes that this project has a strong selling feature but is uncertain that it would earn cash flows as projected. The team proposing this project has come up with the following data: The project tearm also noted that the company has an option to wait for one yoar in order to see its competitors' positions and observe how the market responds. This wil help in getang more information about market dermand and in fouring out which set of cash flors will occur Analysts used different approaches to evaluate the project, but the man agement team insists that the atack=Gicholes option pricing model (Cop) will help them make a mere informed deoision. The model requires five inputs: (1) the riskofree rate; (2) the time until the option expires: (3) the strke price. (4) the current price of the stock, which in this case would be a proxy for the value of the underlying asset; and (b) the variance of the proledis expectand return. You need to caiculate both the value of the underlying aeset in the project and its rate of rotura. For itra Carp. the underiying asset is the progect itsel. The current value of the project will be the value of its expected cash flows: Dased on the data given. calculate che value of the project, iss retum, and the standand devlation of the retums (ising the direct mechod) ir the company decides to wait for a year. (Note: Cash flow valjes in the fable are in milishs, Round an finar answers to two decimal puceik) PVs(t=0)t Analysts will use these values in the Black-Scholes modes, which is represented by the following formula: V=P[N(d1)]Xe1shs[N(d2)] Based on the dath collected and results from the calculations, estimate the input values fo be used in the Blick-Scholas ofN

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts