Question: All the information is given by the picture For a portfolio of n risky assets with the expected return m = (M1, M2, ..., Men)

All the information is given by the picture

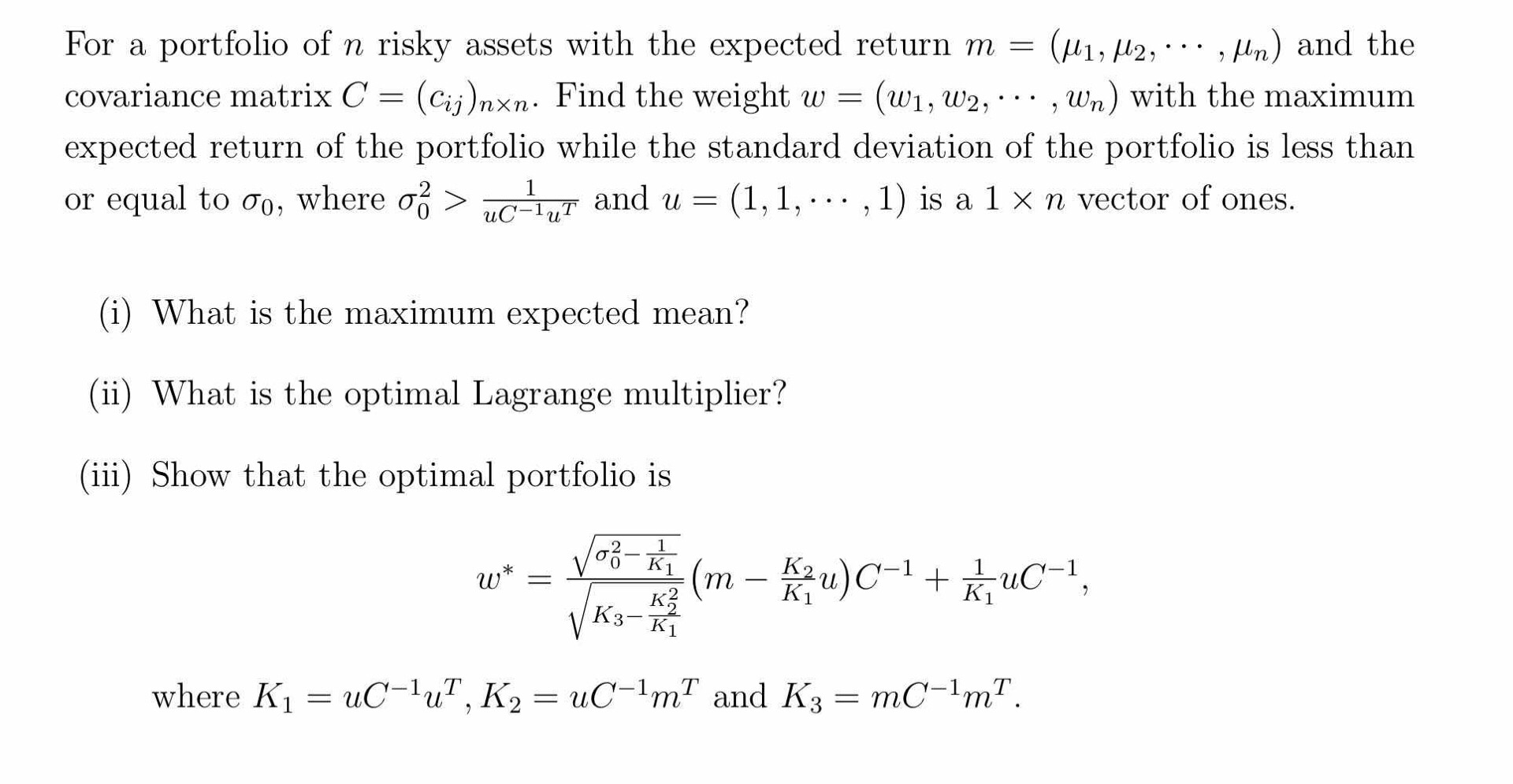

For a portfolio of n risky assets with the expected return m = (M1, M2, ..., Men) and the covariance matrix C = (Cij)nxn. Find the weight w = (W1, W2, ... , Wn) with the maximum expected return of the portfolio while the standard deviation of the portfolio is less than or equal to do, where o > C-1,T and u = (1,1,...,1) is a 1 x n vector of ones. (i) What is the maximum expected mean? (ii) What is the optimal Lagrange multiplier? (iii) Show that the optimal portfolio is VC (m - Eu)C-1+2 uc-, V K3-K where Ki = uC-147, K2 = uC-lmand K3 = mC-Im?'. For a portfolio of n risky assets with the expected return m = (M1, M2, ..., Men) and the covariance matrix C = (Cij)nxn. Find the weight w = (W1, W2, ... , Wn) with the maximum expected return of the portfolio while the standard deviation of the portfolio is less than or equal to do, where o > C-1,T and u = (1,1,...,1) is a 1 x n vector of ones. (i) What is the maximum expected mean? (ii) What is the optimal Lagrange multiplier? (iii) Show that the optimal portfolio is VC (m - Eu)C-1+2 uc-, V K3-K where Ki = uC-147, K2 = uC-lmand K3 = mC-Im

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts