Question: Alpha Holdings appoint you as their junior quant analyst. The CIO is interested to knowing how the S&P 500 market index is affecting energy

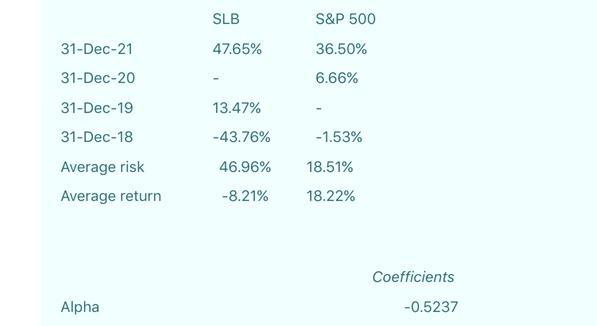

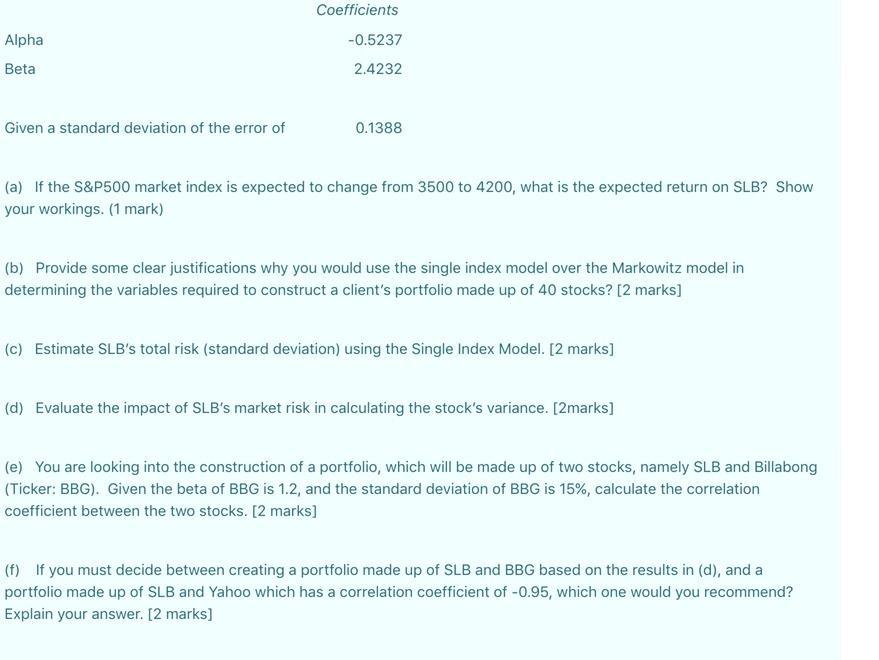

Alpha Holdings appoint you as their junior quant analyst. The CIO is interested to knowing how the S&P 500 market index is affecting energy stock such as Schlumberger (NYSE: SLB). Schlumberger NV engages in the provision of technology for reservoir characterization, drilling, production and processing to the oil and gas industry. It operates through the following business segments: Digital and Integration, Reservoir Performance, Well Construction, and Production Systems. The Digital and Integration segment combines the company's software and seismic businesses with its integrated offering of asset performance solutions. The Reservoir Performance segment consists of reservoir-centric technologies and services that are critical to optimizing reservoir productivity and performance. The Well Construction segment includes the full portfolio of products and services to optimize well placement and performance, maximize drilling efficiency, and improve wellbore assurance. The Production Systems segment develops technologies and provides expertise that enhance production and recovery from subsurface reservoirs to the surface, into pipelines, and to refineries. The company was founded by Conrad Schlumberger and Marcel Schlumberger in 1926 and is headquartered in Houston, TX. The S&P500 market index is used as a good representation of the U.S. equity market. Yearly returns data is used, and the single index model results are as follows: 31-Dec-21 31-Dec-20 31-Dec-19 31-Dec-18 Average risk Average return Alpha SLB 47.65% S&P 500 36.50% 6.66% 13.47% -43.76% -1.53% 46.96% 18.51% -8.21% 18.22% Coefficients -0.5237 Alpha Beta Given a standard deviation of the error of Coefficients -0.5237 2.4232 0.1388 (a) If the S&P500 market index is expected to change from 3500 to 4200, what is the expected return on SLB? Show your workings. (1 mark) (b) Provide some clear justifications why you would use the single index model over the Markowitz model in determining the variables required to construct a client's portfolio made up of 40 stocks? [2 marks] (c) Estimate SLB's total risk (standard deviation) using the Single Index Model. [2 marks] (d) Evaluate the impact of SLB's market risk in calculating the stock's variance. [2marks] (e) You are looking into the construction of a portfolio, which will be made up of two stocks, namely SLB and Billabong (Ticker: BBG). Given the beta of BBG is 1.2, and the standard deviation of BBG is 15%, calculate the correlation coefficient between the two stocks. [2 marks] (f) If you must decide between creating a portfolio made up of SLB and BBG based on the results in (d), and a portfolio made up of SLB and Yahoo which has a correlation coefficient of -0.95, which one would you recommend? Explain your answer. [2 marks] (g) If you want to construct a portfolio based on 30% SLB, 35% Billabong and the rest invested in a risk-free asset, what would be the portfolio beta? Show your workings. [1.5 marks]

Step by Step Solution

3.44 Rating (157 Votes )

There are 3 Steps involved in it

a The expected return on SLB when the SP500 market index is expected to change from 3500 to 4200 is ... View full answer

Get step-by-step solutions from verified subject matter experts