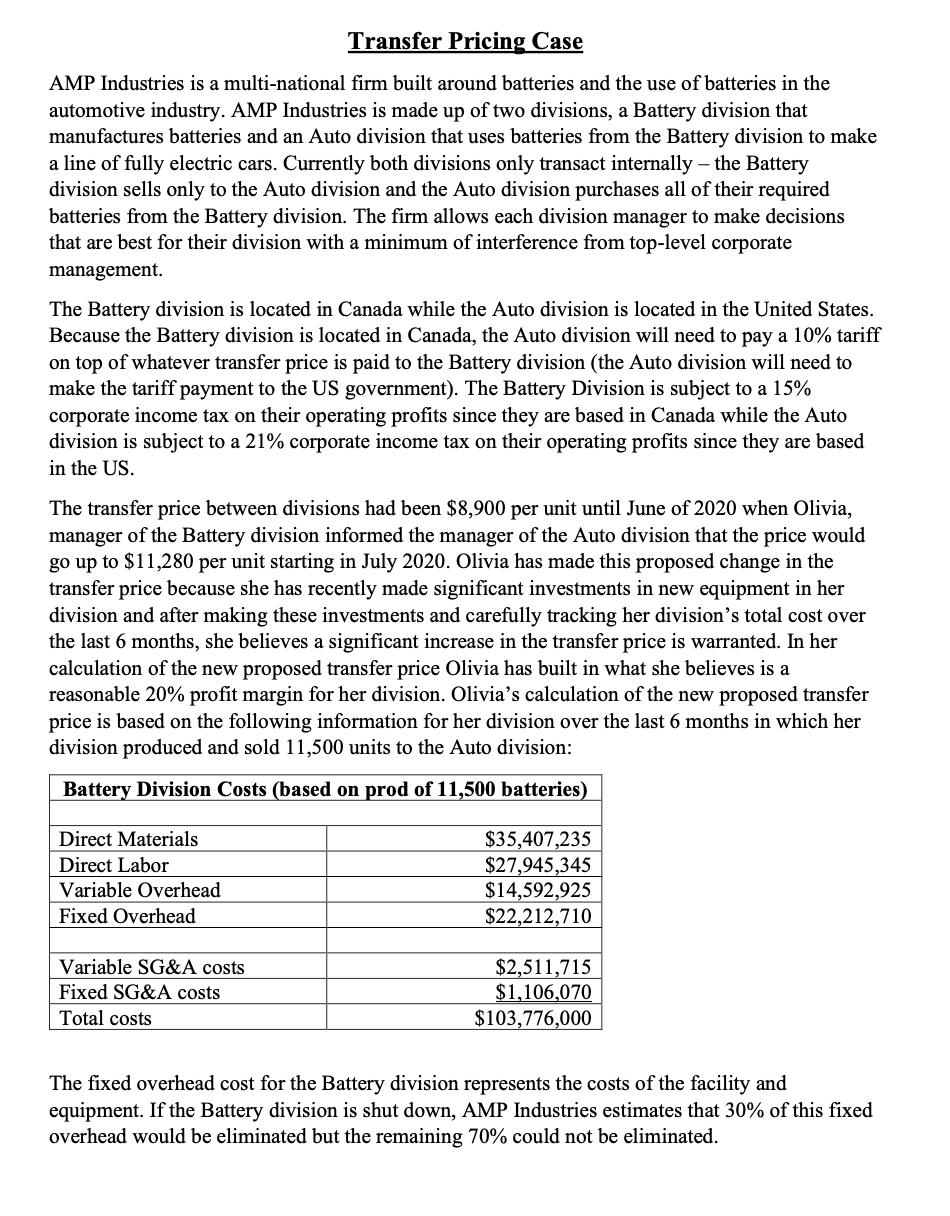

Transfer Pricing Case AMP Industries is a multi-national firm built around batteries and the use of...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

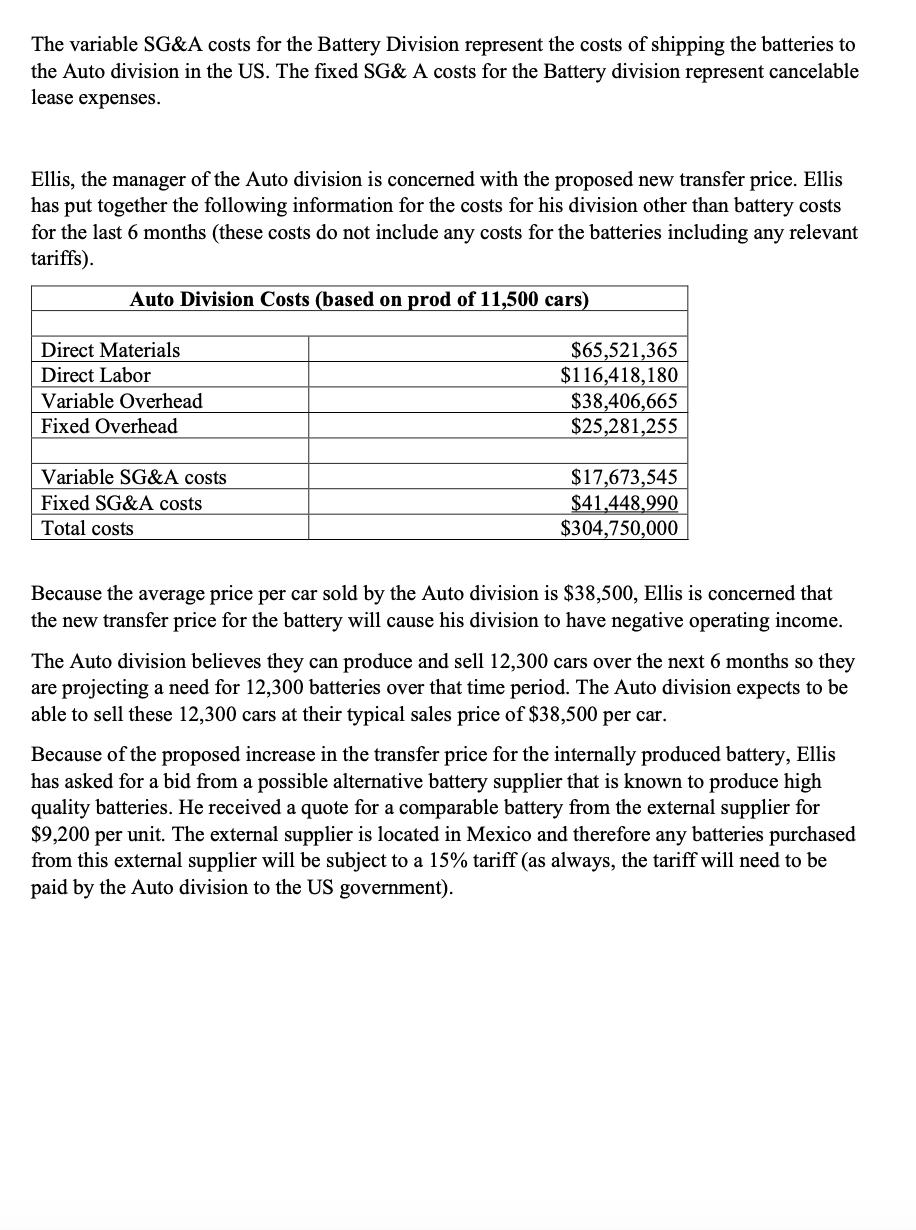

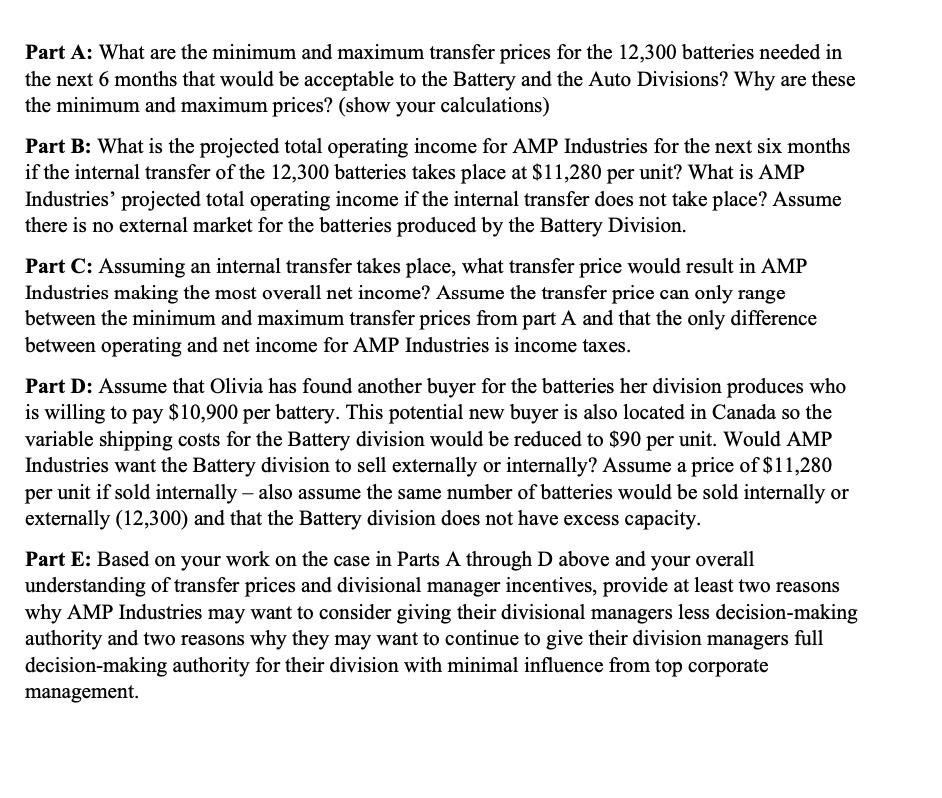

Transfer Pricing Case AMP Industries is a multi-national firm built around batteries and the use of batteries in the automotive industry. AMP Industries is made up of two divisions, a Battery division that manufactures batteries and an Auto division that uses batteries from the Battery division to make a line of fully electric cars. Currently both divisions only transact internally - the Battery division sells only to the Auto division and the Auto division purchases all of their required batteries from the Battery division. The firm allows each division manager to make decisions that are best for their division with a minimum of interference from top-level corporate management. The Battery division is located in Canada while the Auto division is located in the United States. Because the Battery division is located in Canada, the Auto division will need to pay a 10% tariff on top of whatever transfer price is paid to the Battery division (the Auto division will need to make the tariff payment to the US government). The Battery Division is subject to a 15% corporate income tax on their operating profits since they are based in Canada while the Auto division is subject to a 21% corporate income tax on their operating profits since they are based in the US. The transfer price between divisions had been $8,900 per unit until June of 2020 when Olivia, manager of the Battery division informed the manager of the Auto division that the price would go up to $11,280 per unit starting in July 2020. Olivia has made this proposed change in the transfer price because she has recently made significant investments in new equipment in her division and after making these investments and carefully tracking her division's total cost over the last 6 months, she believes a significant increase in the transfer price is warranted. In her calculation of the new proposed transfer price Olivia has built in what she believes is a reasonable 20% profit margin for her division. Olivia's calculation of the new proposed transfer price is based on the following information for her division over the last 6 months in which her division produced and sold 11,500 units to the Auto division: Battery Division Costs (based on prod of 11,500 batteries) Direct Materials $35,407,235 $27,945,345 $14,592,925 $22,212,710 Direct Labor Variable Overhead Fixed Overhead Variable SG&A costs $2,511,715 $1,106,070 $103,776,000 Fixed SG&A costs Total costs The fixed overhead cost for the Battery division represents the costs of the facility and equipment. If the Battery division is shut down, AMP Industries estimates that 30% of this fixed overhead would be eliminated but the remaining 70% could not be eliminated. The variable SG&A costs for the Battery Division represent the costs of shipping the batteries to the Auto division in the US. The fixed SG& A costs for the Battery division represent cancelable lease expenses. Ellis, the manager of the Auto division is concerned with the proposed new transfer price. Ellis has put together the following information for the costs for his division other than battery costs for the last 6 months (these costs do not include any costs for the batteries including any relevant tariffs). Auto Division Costs (based on prod of 11,500 cars) Direct Materials $65,521,365 $116,418,180 $38,406,665 $25,281,255 Direct Labor Variable Overhead Fixed Overhead Variable SG&A costs Fixed SG&A costs Total costs $17,673,545 $41,448,990 $304,750,000 Because the average price per car sold by the Auto division is $38,500, Ellis is concerned that the new transfer price for the battery will cause his division to have negative operating income. The Auto division believes they can produce and sell 12,300 cars over the next 6 months so they are projecting a need for 12,300 batteries over that time period. The Auto division expects to be able to sell these 12,300 cars at their typical sales price of $38,500 per car. Because of the proposed increase in the transfer price for the internally produced battery, Ellis has asked for a bid from a possible alternative battery supplier that is known to produce high quality batteries. He received a quote for a comparable battery from the external supplier for $9,200 per unit. The external supplier is located in Mexico and therefore any batteries purchased from this external supplier will be subject to a 15% tariff (as always, the tariff will need to be paid by the Auto division to the US government). Part A: What are the minimum and maximum transfer prices for the 12,300 batteries needed in the next 6 months that would be acceptable to the Battery and the Auto Divisions? Why are these the minimum and maximum prices? (show your calculations) Part B: What is the projected total operating income for AMP Industries for the next six months if the internal transfer of the 12,300 batteries takes place at $11,280 per unit? What is AMP Industries' projected total operating income if the internal transfer does not take place? Assume there is no external market for the batteries produced by the Battery Division. Part C: Assuming an internal transfer takes place, what transfer price would result in AMP Industries making the most overall net income? Assume the transfer price can only range between the minimum and maximum transfer prices from part A and that the only difference between operating and net income for AMP Industries is income taxes. Part D: Assume that Olivia has found another buyer for the batteries her division produces who is willing to pay $10,900 per battery. This potential new buyer is also located in Canada so the variable shipping costs for the Battery division would be reduced to $90 per unit. Would AMP Industries want the Battery division to sell externally or internally? Assume a price of $11,280 per unit if sold internally – also assume the same number of batteries would be sold internally or externally (12,300) and that the Battery division does not have excess capacity. Part E: Based on your work on the case in Parts A through D above and your overall understanding of transfer prices and divisional manager incentives, provide at least two reasons why AMP Industries may want to consider giving their divisional managers less decision-making authority and two reasons why they may want to continue to give their division managers full decision-making authority for their division with minimal influence from top corporate management. Transfer Pricing Case AMP Industries is a multi-national firm built around batteries and the use of batteries in the automotive industry. AMP Industries is made up of two divisions, a Battery division that manufactures batteries and an Auto division that uses batteries from the Battery division to make a line of fully electric cars. Currently both divisions only transact internally - the Battery division sells only to the Auto division and the Auto division purchases all of their required batteries from the Battery division. The firm allows each division manager to make decisions that are best for their division with a minimum of interference from top-level corporate management. The Battery division is located in Canada while the Auto division is located in the United States. Because the Battery division is located in Canada, the Auto division will need to pay a 10% tariff on top of whatever transfer price is paid to the Battery division (the Auto division will need to make the tariff payment to the US government). The Battery Division is subject to a 15% corporate income tax on their operating profits since they are based in Canada while the Auto division is subject to a 21% corporate income tax on their operating profits since they are based in the US. The transfer price between divisions had been $8,900 per unit until June of 2020 when Olivia, manager of the Battery division informed the manager of the Auto division that the price would go up to $11,280 per unit starting in July 2020. Olivia has made this proposed change in the transfer price because she has recently made significant investments in new equipment in her division and after making these investments and carefully tracking her division's total cost over the last 6 months, she believes a significant increase in the transfer price is warranted. In her calculation of the new proposed transfer price Olivia has built in what she believes is a reasonable 20% profit margin for her division. Olivia's calculation of the new proposed transfer price is based on the following information for her division over the last 6 months in which her division produced and sold 11,500 units to the Auto division: Battery Division Costs (based on prod of 11,500 batteries) Direct Materials $35,407,235 $27,945,345 $14,592,925 $22,212,710 Direct Labor Variable Overhead Fixed Overhead Variable SG&A costs $2,511,715 $1,106,070 $103,776,000 Fixed SG&A costs Total costs The fixed overhead cost for the Battery division represents the costs of the facility and equipment. If the Battery division is shut down, AMP Industries estimates that 30% of this fixed overhead would be eliminated but the remaining 70% could not be eliminated. The variable SG&A costs for the Battery Division represent the costs of shipping the batteries to the Auto division in the US. The fixed SG& A costs for the Battery division represent cancelable lease expenses. Ellis, the manager of the Auto division is concerned with the proposed new transfer price. Ellis has put together the following information for the costs for his division other than battery costs for the last 6 months (these costs do not include any costs for the batteries including any relevant tariffs). Auto Division Costs (based on prod of 11,500 cars) Direct Materials $65,521,365 $116,418,180 $38,406,665 $25,281,255 Direct Labor Variable Overhead Fixed Overhead Variable SG&A costs Fixed SG&A costs Total costs $17,673,545 $41,448,990 $304,750,000 Because the average price per car sold by the Auto division is $38,500, Ellis is concerned that the new transfer price for the battery will cause his division to have negative operating income. The Auto division believes they can produce and sell 12,300 cars over the next 6 months so they are projecting a need for 12,300 batteries over that time period. The Auto division expects to be able to sell these 12,300 cars at their typical sales price of $38,500 per car. Because of the proposed increase in the transfer price for the internally produced battery, Ellis has asked for a bid from a possible alternative battery supplier that is known to produce high quality batteries. He received a quote for a comparable battery from the external supplier for $9,200 per unit. The external supplier is located in Mexico and therefore any batteries purchased from this external supplier will be subject to a 15% tariff (as always, the tariff will need to be paid by the Auto division to the US government). Part A: What are the minimum and maximum transfer prices for the 12,300 batteries needed in the next 6 months that would be acceptable to the Battery and the Auto Divisions? Why are these the minimum and maximum prices? (show your calculations) Part B: What is the projected total operating income for AMP Industries for the next six months if the internal transfer of the 12,300 batteries takes place at $11,280 per unit? What is AMP Industries' projected total operating income if the internal transfer does not take place? Assume there is no external market for the batteries produced by the Battery Division. Part C: Assuming an internal transfer takes place, what transfer price would result in AMP Industries making the most overall net income? Assume the transfer price can only range between the minimum and maximum transfer prices from part A and that the only difference between operating and net income for AMP Industries is income taxes. Part D: Assume that Olivia has found another buyer for the batteries her division produces who is willing to pay $10,900 per battery. This potential new buyer is also located in Canada so the variable shipping costs for the Battery division would be reduced to $90 per unit. Would AMP Industries want the Battery division to sell externally or internally? Assume a price of $11,280 per unit if sold internally – also assume the same number of batteries would be sold internally or externally (12,300) and that the Battery division does not have excess capacity. Part E: Based on your work on the case in Parts A through D above and your overall understanding of transfer prices and divisional manager incentives, provide at least two reasons why AMP Industries may want to consider giving their divisional managers less decision-making authority and two reasons why they may want to continue to give their division managers full decision-making authority for their division with minimal influence from top corporate management.

Expert Answer:

Answer rating: 100% (QA)

A Direct Materials3540723511500307889 Direct labor2794534511500243003 Variable Overhead1459292511500126895 Fixed Overhead based on allocation of 30222... View the full answer

Related Book For

Foundations of the Legal Environment of Business

ISBN: 978-1305117457

3rd edition

Authors: Marianne M. Jennings

Posted Date:

Students also viewed these accounting questions

-

In applications involving the use of quadtrees in memory-constrained devices, such as smartphones, we often want to optimize the data structure to make it more space efficient. One obvious...

-

In this exercise, you explore the use of integers in monetary calculations. a. Follow the instructions for starting C++ and opening the Advanced16.cpp file. Run the program. Enter 256.7 and 223.3 as...

-

The use of snowmobiles in Yellowstone and Grand Teton National Parks has been a topic of ongoing concern because of their impact on park resources. In 2003, the National Park Service (NPS) groomed...

-

The graph of f is given. (a) Why is f one-to-one? (b) What are the domain and range of f 1 ? (c) What is the value of f 1 (2)? (d) Estimate the value of f -1 (0). 1

-

Using the Explore procedure, separate the statistics for AGEKDBRN for men and women, selecting SEX as a factor variable in the Explore window. Click on Analyze, Descriptive Statistics, Explore, and...

-

Give a specific example of a system with the energy transformation shown. In these questions, \(W\) is the work done on the system, and \(K, U\), and \(E_{\mathrm{th}}\) are the kinetic, potential,...

-

Teller Crackers & Snacks (TCS) recently held a contest in which it awarded each of ten randomly drawn entrants a large box of assorted crackers each week for a year. The names and addresses of the...

-

World- famous mining mogul Steve Wilsey hired the public accounting firm of Joe Wang Associates, PC, to conduct an audit of his new acquisition, Cougar Goldust, Inc. The gold inventory was scheduled...

-

mment T4075 As CIT-1075 (1%) Consider ment CCIT 1075 Assignmes m-1 n=0 Consider the dataset {9}-0 Assume m is a multiple of (a) (1%) Suppose 9 = cos(2/3). Estimate the pmf of the random variable...

-

Create and insert an ERD showing the constellation ERD schema below. Please see requirements in the next two sections. Determine four to five (non-date/time) dimension tables a. SCDs need to be...

-

The graph of y = f(x) is illustrated below: -6 0 Identify which of the graphs below represent the following transformations: y = f(x) : y = f(x 3) : - y = f() : y = f(2(x+2)) :

-

Swifty Company has an old factory machine that cost $52,000. The machine has accumulated depreciation of $29,120. Swifty has decided to sell the machine. (a) Prepare a tabular summary to record the...

-

Discuss how deadlock scenarios can arise in transactional database systems, particularly in the context of concurrent transactions. What are the common techniques used by database management systems...

-

Explain the relationship between concurrency and deadlock. In what ways does increased concurrency in a system contribute to the risk of deadlock, and what mechanisms can be employed to ensure that...

-

Both firms are 100% equity-financed. Firm A can acquire firm B for $82,500 in the form of either cash or stock. The synergy value of the deal is $12,500. Number of Shares Price per Share Firm A...

-

Kapono Farms exchanged an old tractor for a newer model. The old tractor had a book value of $15,000 (original cost of $34,000 less accumulated depreciation of $19,000) and a fair value of $9,600....

-

Define psychology as a science and its components? Also write 10 reasons why psychology is a science ?

-

The words without recourse on an indorsement means the indorser is: a. not liable for any problems associated with the instrument. b. not liable if the instrument is dishonored. c. liable personally...

-

Amazon.com closed its Irvine, Texas center because of a dispute with the Texas state comptroller over $ 269 million that the controller says Amazon owes to the state in sales taxes for goods shipped...

-

Smith & Smith, a U. S. computer firm, contracted to install a computer system for Volkswagen in the companys headquarters in Berlin, Germany. Smiths contract included the following liability...

-

Dr. Bryan Cook is a licensed dentist who fitted and made a set of dentures for Mrs. Iris Downing, a patient of Dr. Cook who was fitted for dentures. After Mrs. Downing received her dentures from Dr....

-

Vertical analysis would rarely be performed on which of the following statements or schedules? a. Income statement b. Adjusting entry worksheet c. Balance sheet d. All of the above are common targets...

-

A statement that lists the assets, liabilities, and stockholders equity of a company in percentages only with no dollar amounts is a a. common-size income statement. b. benchmarking analysis. c....

-

In vertical analysis, the base used for comparison on the income statement is a. total expenses. b. total assets. c. net sales. d. gross profit.

Study smarter with the SolutionInn App