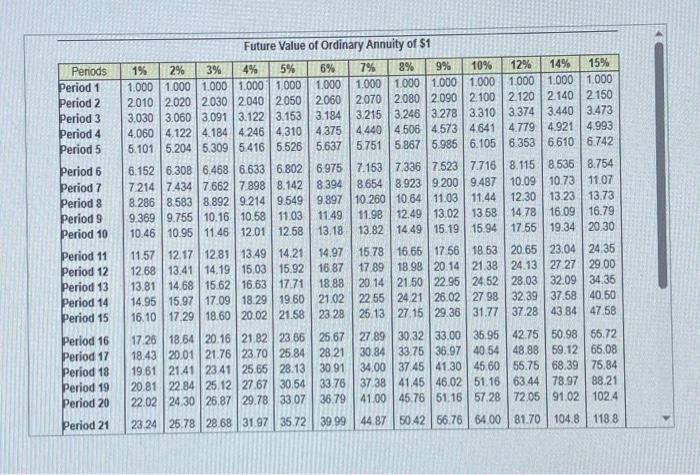

Question: Amy wants to take the next five years off work to travel around the world. She estimates her annual cash needs at $34,000 (if

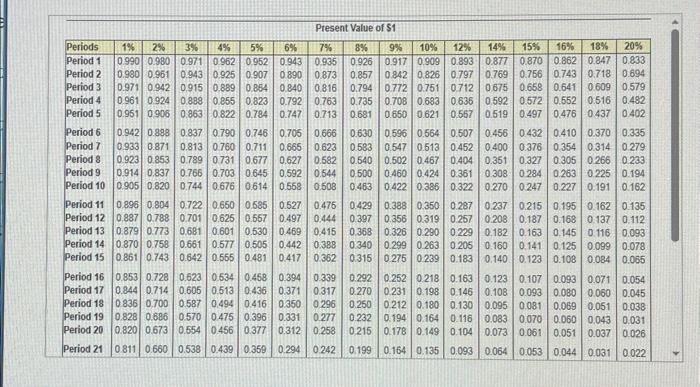

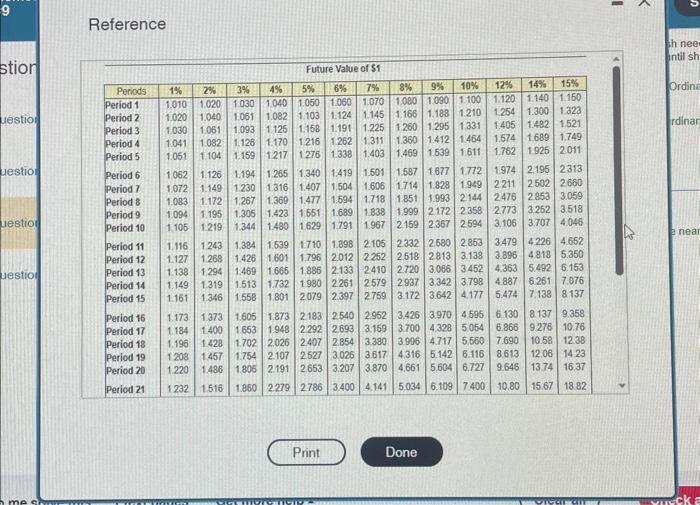

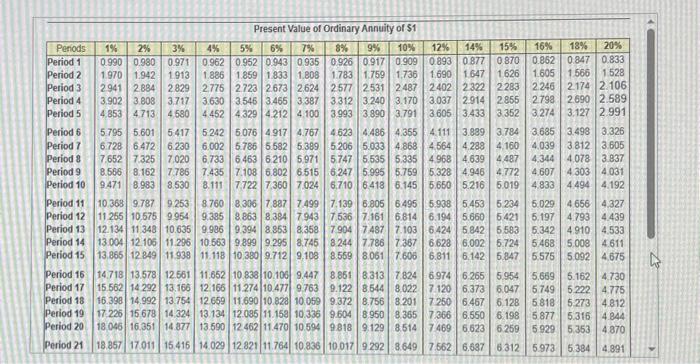

Amy wants to take the next five years off work to travel around the world. She estimates her annual cash needs at $34,000 (if she needs more, she will work odd jobs). Amy believes she can invest her savings at 10% until she depletes her funds. (Click the icon to view Present Value of $1 table.) Annuity of $1 table.) (Click the icon to view Future Value of $1 table.) of $1 table.) Read the requirements (Click the icon to view Present Value of Ordinary (Click the icon to view Future Value of Ordinary Annuity Requirement 1. How much money does Amy need now to fund her travels? (Round your answer to the nearest whole dollar.) With the 10% interest rate, Amy needs I Requirements 1. How much money does Amy need now to fund her travels? 2. After speaking with a number of banks, Amy learns she will only be able to invest her funds at 6%. How much does she need now to fund her travels? X Present Value of $1 Periods Period 1 1% 2% 3% 4% 5% 6% 8% 0.990 0.980 0.971 0.962 0.952 Period 2 0.980 0.961 0.943 0.925 Period 3 0.971 0.942 0.915 0.889 Period 4 0.961 0.924 0.888 Period 5 0.951 0.906 0.863 0.907 0.890 0.854 0.840 0.816 0.855 0.823 0.792 0.763 0.822 0.784 0.747 0.713 7% 9% 10% 12% 14% 15% 16% 18% 20% 0.943 0.935 0.926 0.917 0.909 0.893 0.877 0.870 0.862 0.847 0.833 0.873 0.857 0.842 0.826 0.797 0.769 0.756 0.743 0.718 0.694 0.794 0.772 0.751 0.712 0.675 0.658 0.641 0.609 0.579 0.735 0.708 0.683 0.636 0.592 0.572 0.552 0.516 0.482 0.681 0.650 0.621 0.567 0.519 0.497 0.476 0.437 0.402 Period 6 0.942 0.888 0.837 0.790 0.746 Period 7 0.933 0.871 0.813 0.760 0.711 0.665 Period 8 0.923 0.853 0.789 0731 0.677 0.705 0.666 0.623 0.627 0.582 Period 9 0.914 0.837 0.766 0.703 Period 10 0.905 0.820 0.744 0.676 0.614 0.645 0.592 0.544 0.558 0.508 Period 11 0.896 0.804 0.722 0.650 0.585 0.527 0.475 Period 12 0.887 0.788 0.701 0.625 0.557 0.497 0.444 Period 13 0.879 0.773 0.681 0.601 0.530 0.469 0.415 Period 14 0.870 0.758 0.661 0.577 0.505 0.442 0.388 Period 15 0.861 0.743 0.642 0.555 0.481 0.417 0.362 Period 16 0.853 0.728 0.623 0.534 0.458 0.394 0.339 Period 17 0.844 0.714 0.605 0.513 0.436 0.371 0.317 Period 18 0.836 0.700 0.587 0.494 0.416 0.350 0.296 Period 19 0.828 0.686 0.570 0.475 0.396 0.331 0.277 Period 20 0.820 0.673 0.554 0.456 0.377 0.312 0.258 Period 21 0811 0.660 0.538 0.439 0.359 0.294 0.242 0.630 0.596 0.564 0.507 0.456 0.432 0.410 0.370 0.335 0.583 0.547 0.513 0.452 0.400 0.376 0.354 0.314 0.279 0.540 0.502 0.467 0.404 0.351 0.327 0.305 0.266 0.233 0.500 0.460 0.424 0.361 0.308 0.284 0.263 0.225 0.194 0.463 0.422 0.386 0.322 0.270 0.247 0.227 0.191 0.162 0.429 0.388 0.350 0.287 0.237 0.215 0.195 0.162 0.135 0.397 0.356 0.319 0.257 0.208 0.187 0.168 0.137 0.112 0.368 0.326 0.290 0.229 0.182 0.163 0.145 0.116 0.093 0.340 0.299 0.263 0.205 0.160 0.141 0.125 0.099 0.078 0.315 0.275 0.239 0.183 0.140 0.123 0.108 0.084 0.065 0.292 0.252 0.218 0.163 0.270 0.231 0.198 0.146 0.250 0.212 0.180 0.130 0.232 0.194 0.164 0.116 0.215 0.178 0.149 0.104 0.123 0.107 0.093 0.071 0.054 0.108 0.093 0.080 0.060 0.045 0.095 0.081 0.069 0.051 0.038 0.083 0.070 0.060 0.043 0.031 0.073 0.061 0.051 0.037 0.026 0.199 0.164 0.135 0.093 0.064 0.053 0.044 0.031 0.022 6 Reference I stion h nee until shi Future Value of $1 Periods 1% 2% 3% 4% Period 1 1.010 1.020 1.030 1.040 uestion Period 21 1.020 1.040 1.061 Period 3 1.030 1.061 1.093 Period 4 Period 5 1.051 1.041 1.082 1.104 1.159 1.126 10% 9% 8% 5% 6% 1.050 1.060 1.070 1.080 1.090 1.100 1.082 1.103 1.124 1.145 1.166 1.188 1.210 1.125 1.158 1.191 1.225 1.260 1.295 1.331 1.170 1.216 1.262 1.311 1.360 1.412 1.464 1217 1276 1.338 1.403 1.469 1.539 1.611 7% 12% 14% 1.120 1.140 1.150 15% Ordina 1.254 1.300 1.323 1.405 1.482 1.521 rdinar 1.574 1.689 1,749 1.762 1.925 2011 uestion Period 6 1.062 Period 7 1.072 Period & 1.083 1.172 1.126 1.194 1.149 1.230 1.267 Period 9 1.094 1.195 uestion Period 10 1.105 1.219 Period 11 1.116 1.243 Period 12 1.127 1.268 uestion Period 13 Period 14 Period 15 1.138 1.294 1.149 1.319 1.161 1.346 1.265 1.340 1.419 1.501 1.587 1677 1772 1974 2.195 2313 1.316 1.407 1.504 1.606 1.714 1.828 1.949 2.211 2.502 2.660 1.369 1.477 1.594 1.718 1851 1.993 2144 2476 2.853 3.059 1.305 1.423 1.551 1.689 1.838 1.999 2172 2.358 2.773 3.252 3.518 1.344 1.480 1.629 1.791 1.967 2.159 2.367 2.594 3.106 3.707 4.046 1.384 1.539 1.710 1.898 2.105 2.332 2.580 2.853 3.479 4.226 4.652 1.426 1.601 1.796 2012 2.252 2518 2.813 3.138 3.896 4.818 5.350 1.469 1.665 1.886 2.133 2.410 2.720 3.066 3.452 4.363 5.492 6.153 1.513 1.732 1.980 2.261 2.579 2937 3.342 3.798 4.887 6.261 7.076 1.558 1.801 2079 2.397 2.759 3.172 3.642 4.177 5.474 7.138 8137 Period 16 1.173 1.373 1.606 1.873 2.183 2.540 2.962 3.426 3.970 4.595 6.130 8137 9.358 Period 17 1.184 1.400 1.653 1.948 2.292 2.693 3.159 3.700 4.328 5.054 6.866 9.276 10.76 Period 18 1.196 1.428 1.702 2.026 2.407 2.854 3.380 3.996 4.717 5.560 7.690 10.58 12.38 Period 19 1.208 1.457 1.754 2.107 2.527 3.026 3.617 4.316 5.142 6.116 8.613 12.06 14.23 Period 20 1.220 1.486 1.806 2.191 2.653 3.207 3.870 4.661 5.604 6.727 9.646 13.74 16.37 Period 21 1232 1.516 1.860 2.279 2.786 3.400 4.141 5.034 6.109 7.400 10.80 15.67 18.82 e near Print Done a me sh OGLIUTC TICTO SiCar CITT 13 Periods Period 1 Period 2 Period 3 Period 4 Period 5 1% Present Value of Ordinary Annuity of $1 3% 4% 5% 20% 2% 6% 7% 8% 9% 10% 12% 14% 15% 16% 18% 0.990 0.980 0.971 0.962 0.952 0.943 0.935 0.926 0.917 0.909 0.893 0.877 0870 0.862 0.847 0.833 1.970 1.942 1913 1.886 1.859 1.833 1.808 1.783 1.759 1.736 1.690 1.647 1.626 1.605 1.566 1.528 2.941 2.884 2.829 2.775 2.723 2.673 2.624 2.577 2.531 2487 2.402 2.322 2283 2.246 2.174 2.106 3.902 3.808 3.717 3.630 3.546 3.465 3.387 3.312 3.240 3.170 3.037 2.914 2.855 2.798 2.690 2.589 4.853 4.713 4.580 4.452 4.329 4.212 4.100 3.993 3.890 3.791 3.605 3.433 3.352 3.274 3.127 2.991 Period 6 5.795 5.601 5417 5.242 5.076 4917 4.767 4.623 4.486 4.355 4.111 3.889 3.784 3.685 3.498 3.326 Period 7 6.728 6.472 6.230 6.002 5.786 5.582 5.389 5.206 5.033 4.868 4.564 4.288 4.160 4.039 3812 3.605 Period 8 7.652 7.325 7.020 6.733 6.463 6.210 5.971 5.747 5.535 5.335 4.968 4.639 4.487 4.344 4.078 3.837 Period 9 8.566 8.162 7.786 7.435 7.108 6.802 6.515 6.247 5.995 5.759 5.328 4.946 4.772 4.607 4.303 4.031 Period 10 9.471 8.983 8.530 8.111 7722 7.360 7.024 6,710 6.418 6.145 5.650 5.216 5.019 4.833 4.494 4.192 Period 11 10.368 9.787 9.253 8.760 8.306 7.887 7.499 7.139 6.805 6.495 5.938 5.453 5.234 5.029 4.656 4.327 Period 12 11 255 10.575 9.954 9.385 8.863 8.384 7.943 7.536 7.161 6.814 6.194 5.660 5.421 5.197 4.793 4.439 Period 13 12.134 11 348 10.635 9.986 9.394 8.853 8.358 7.904 7.487 7.103 6.424 5.842 5.583 5.342 4.910 4.533 Period 14 13.004 12.106 11.296 10.563 9.899 9.295 8.745 8.244 7.786 7.367 6.628 6.002 5.724 5.468 5.008 4.611 Period 15 13.865 12.849 11.938 11.118 10.380 9.712 9.108 8.559 8.061 7.606 6.811 6.142 5.847 5.575 5.092 4,675 Period 16 14.718 13.578 12.561 11.652 10.838 10.106 9.447 8.851 8.313 7.824 6.974 6.265 5.954 5.669 5.162 4.730 Period 17 15.562 14 292 13.166 12.166 11.274 10.477 9.763 9.122 8.544 8.022 7.120 6.373 6.047 5.749 5.222 4.775 Period 18 16.398 14.992 13.754 12.659 11.690 10.828 10.059 9.372 8.756 8.201 7.250 6.467 6.128 5.818 5.273 4.812 Period 19 17.226 15 678 14.324 13.134 12.085 11.158 10.336 9.604 8.950 8.365 7.366 6.550 6.198 5.877 5.316 4.844 Period 20 18,046 16.351 14.877 13.590 12.462 11.470 10.594 9818 9.129 8.514 7.469 6.623 6.259 5.929 5.353 4.870 Period 21 18.857 17.011 15.415 14.029 12.821 11.764 10.836 10.017 9.292 8.649 7.562 6.687 6.312 5.973 5.384 4.891 Periods 1% 2% 4% 3% 5% Period 1 1.000 1.000 1.000 1.000 1.000 Period 2 2010 2.020 2030 2040 2050 Period 3 3.030 3.060 3.091 3.122 3.153 Period 4 4.060 4.122 4.184 4.246 4.310 Period 5 5.101 5.204 5.309 5.416 5.526 6% 1.000 2060 3.184 4.375 5.637 Future Value of Ordinary Annuity of $1 9% 12% 15% 14% 10% 7% 8% 1.000 1.000 1.000 1.000 1.000 1.000 1.000 2.070 2.080 2.090 2100 2.120 2.140 2.150 3.215 3.246 3.278 3.310 3.374 3.440 3.473 4.440 4.506 4.573 4.641 4.779 4.921 4.993) 5.751 5.867 5.985 6.105 6.353 6.610 6.742 Period 6 Period 7 Period & Period 9 Period 10 6.152 6.308 6.468 6.633 6.802 7.214 7.434 7.662 7.898 8.142 8.286 8.583 8.892 9.214 9.549 9.369 9.755 10.16 10.58 11.03 10.46 10.95 11.46 12.01 12.58 6.975 8.394 9.897 11.49 13.18 Period 11 11.57 12.17 12.81 13.49 14.21 Period 12 12.68 13.41 14,19 15.03 15.92 Period 13 13.81 14.68 15.62 16.63 17.71 Period 14 14.95 15.97 17.09 18.29 19.60 Period 15 16.10 17.29 18.60 20.02 21.58 14.97 16.87 18.88 21.02 23.28 7.153 7.336 7.523 7.716 8.115 8.536 8.754. 8.654 8.923 9.200 9.487 10.09 10.73 11.07 10.260 10.64 11.03 11.44 12.30 13.23 13.73 11.98 12.49 13.02 13.58 14.78 16.09 16.79 13.82 14.49 15.19 15.94 17.55 19.34 20.30 15.78 16.65 17.56 18.53 20.65 23.04 24.35 17.89 18.98 20.14 21.38 24.13 27.27 29.00 20 14 21.50 22.95 24.52 22.55 24.21 26.02 27 98 25.13 27.15 29.36 31.77 28.03 32.09 34.35 32.39 37.58 40.50 37.28 43.84 47.58 Period 17 Period 18 Period 16 17.26 18.64 20.16 21.82 23.66 18.43 20.01 21.76 23.70 25.84 19.61 21.41 23.41 25.65 28.13 25.67 28.21 30.91 Period 19 Period 20 20.81 22.84 25.12 27.67 30.54 22.02 24.30 26.87 29.78 33.07 33.76 36.79 Period 21 23.24 25.78 28.68 31.97 35.72 39.99 27.89 30.32 33.00 35.95 30.84 33.75 36.97 40.54 48.88 59.12 65.08 34.00 37.45 41.30 45.60 55.75 68.39 75.84 37 38 41.45 46.02 51.16 63.44 78.97 88.21 41.00 45.76 51.16 57.28 72.05 91.02 102.4 44.87 50.42 56.76 64.00 81.70 104.8 118.8 42.75 50.98 55.72

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts