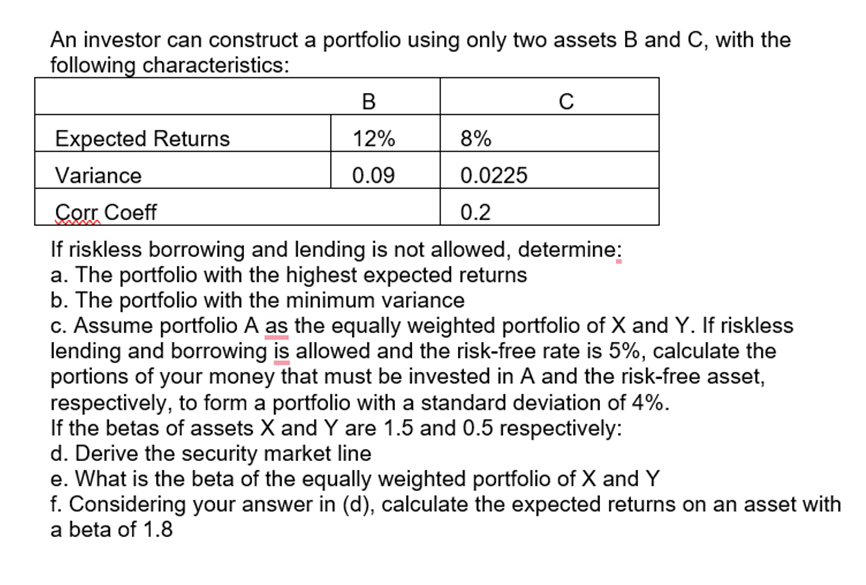

Question: An investor can construct a portfolio using only two assets B and C, with the following characteristics: If riskless borrowing and lending is not allowed,

An investor can construct a portfolio using only two assets B and C, with the following characteristics: If riskless borrowing and lending is not allowed, determine: a. The portfolio with the highest expected returns b. The portfolio with the minimum variance c. Assume portfolio A as the equally weighted portfolio of X and Y. If riskless lending and borrowing is allowed and the risk-free rate is 5%, calculate the portions of your money that must be invested in A and the risk-free asset, respectively, to form a portfolio with a standard deviation of 4%. If the betas of assets X and Y are 1.5 and 0.5 respectively: d. Derive the security market line e. What is the beta of the equally weighted portfolio of X and Y f. Considering your answer in (d), calculate the expected returns on an asset with a beta of 1.8

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts