Question: Ann Arbor Railroad Company case Learning Objectives 1. Practice how to map and allocate costs into services/products. 2. Practice the concept of relevant cost and

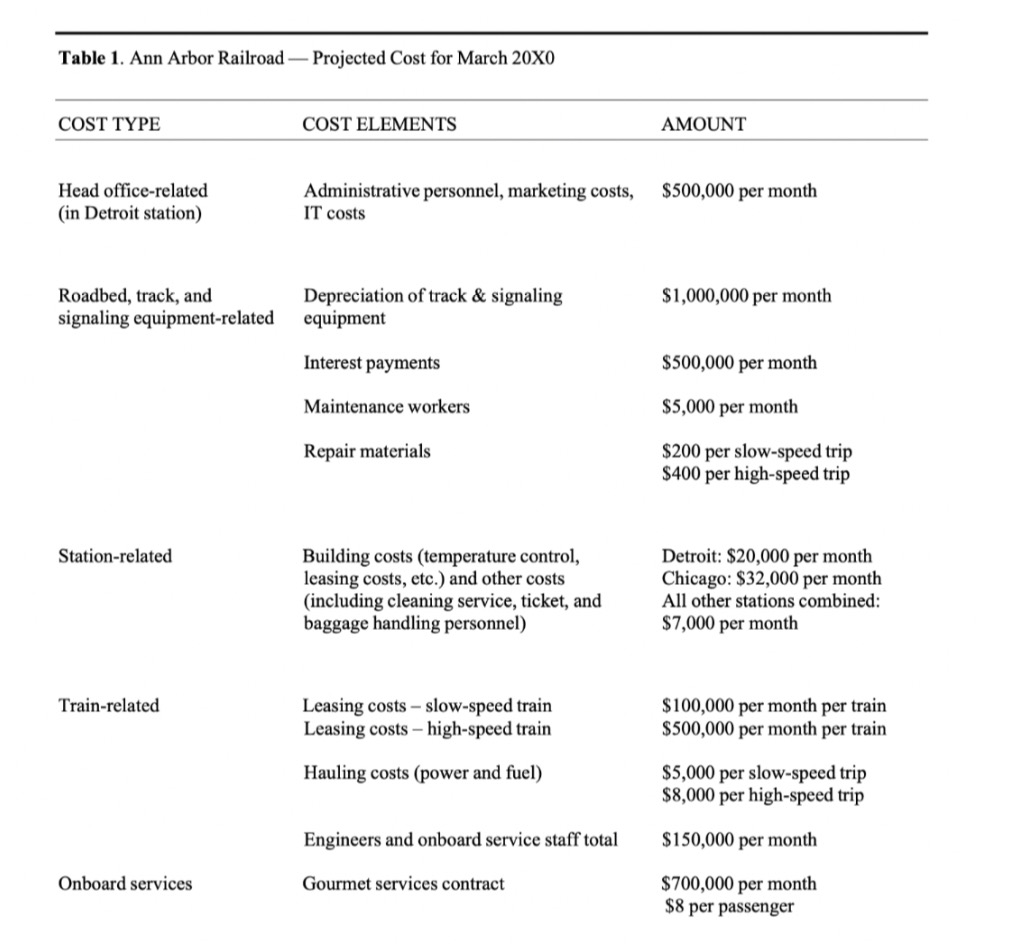

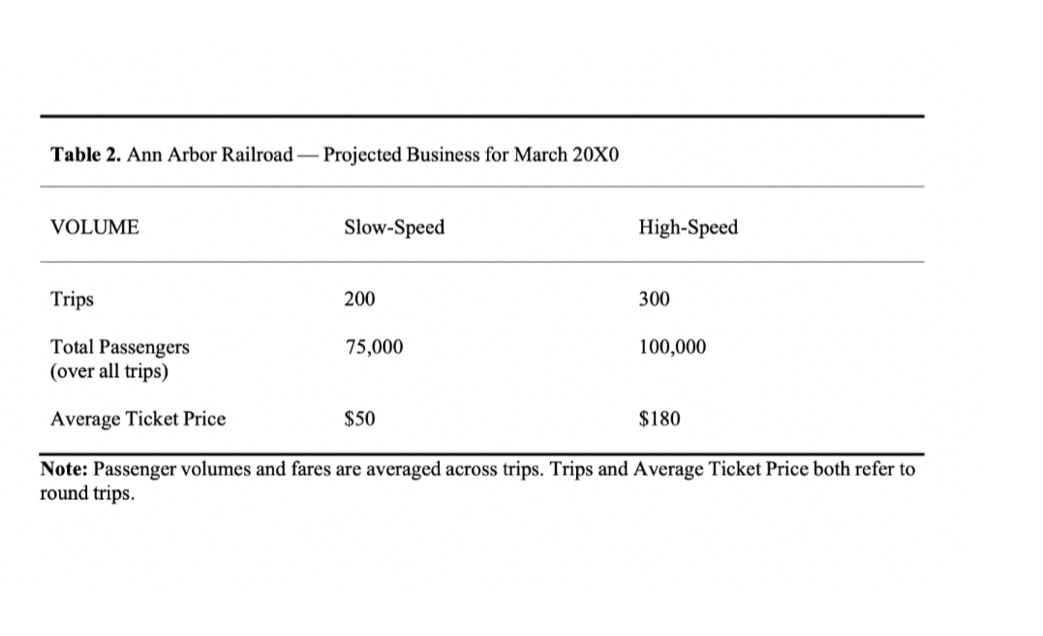

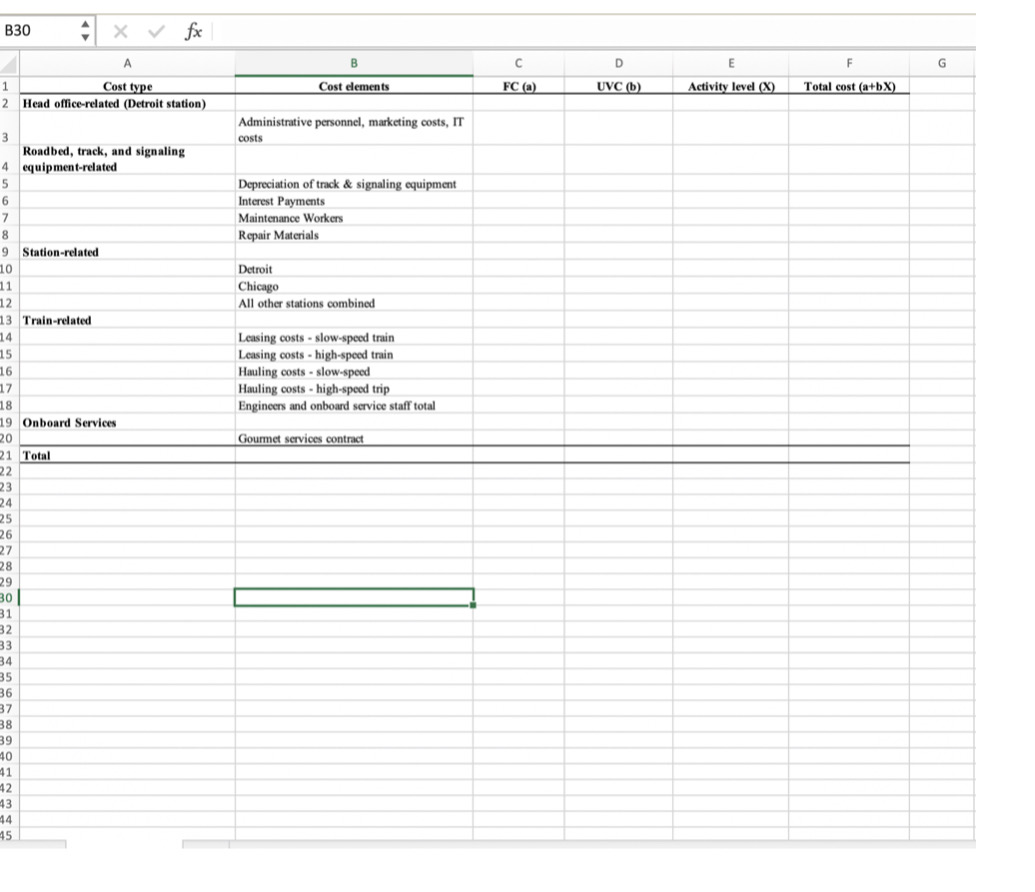

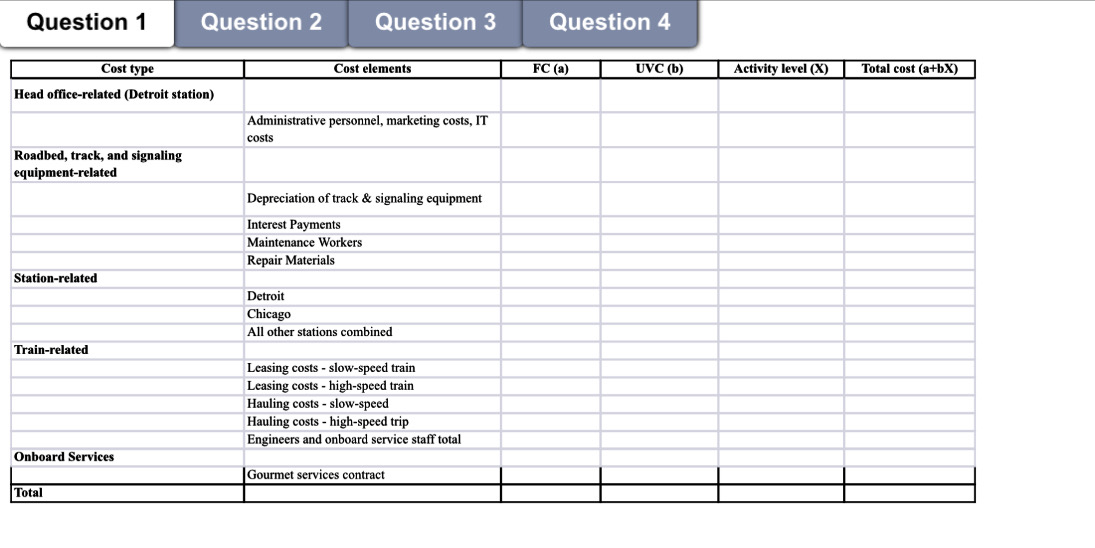

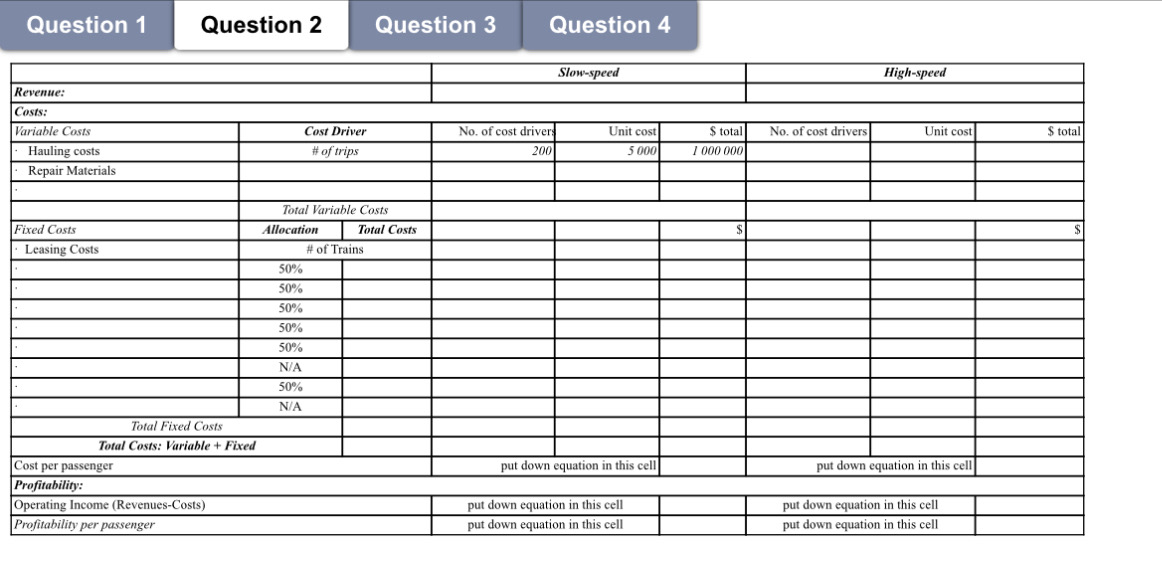

Ann Arbor Railroad Company case Learning Objectives 1. Practice how to map and allocate costs into services/products. 2. Practice the concept of relevant cost and apply it to differential analysis in a decision-making context of special order. 3. Practice building different cost congurations for different purposes in Excel. Background Ann Arbor Railroad (AAR) is a railroad company that is partly nanced by the US Department of Transportation through its high-speed rail stimulus initiative. AAR operates daily train service between Detroit, MI and Chicago, IL. The Company operates two classes of passenger trains: slow-speed and high-speed. AAR built and currently maintains a roadbed and tracks between the two cities as well as stations in both Detroit, MI and Chicago, IL. The tracks and signaling equipment cost approximately $1 million per mile to build and will be depreciated over thirty years. The bulk of the Company's station-related costs arise from the Detroit and Chicago stations. Costs for the intermediate stations, which are ouly used by the slow-speed trains, are largely paid for by the local municipalities. AAR does not own any trains, but leases them. Specically, it leases 10 high-speed trains (locomotives plus carriages) 'om Siemens AG and 10 slow-speed trains (locomotives plus carriages) from GE. Locomotives refer to the motorized entity pulling the caniages. Carriages carry passengers but are unable to move autonomously. The Company is responsible for maintaining the trains. The highspeed trains are technologically advanced and more costly than the slow-speed trains, which are technologically simpler and older. AAR employs the train engineers and the onboard service staff. The Company has contracted with Gourmet Services to provide complimentary food and drinks to high-speed passengers. The contract entails a xed monthly payment of $700,000 plus $8 per passenger. Slow-speed train passengers receive no complimentary items; they can buy food and beverages from an independent catering company with no prot or loss for MR. Projected cost and travel volume data appear in Tables 1 and 2. Please refer to these to answer the following questions. The data are only approximate and have been modied to ease computations. Table 1. Ann Arbor Railroad - Projected Cost for March 20X0 COST TYPE COST ELEMENTS AMOUNT Head office-related Administrative personnel, marketing costs, $500,000 per month (in Detroit station) IT costs Roadbed, track, and Depreciation of track & signaling $1,000,000 per month signaling equipment-related equipment Interest payments $500,000 per month Maintenance workers $5,000 per month Repair materials $200 per slow-speed trip $400 per high-speed trip Station-related Building costs (temperature control, Detroit: $20,000 per month leasing costs, etc.) and other costs Chicago: $32,000 per month (including cleaning service, ticket, and All other stations combined: baggage handling personnel) $7,000 per month Train-related Leasing costs - slow-speed train $100,000 per month per train Leasing costs - high-speed train $500,000 per month per train Hauling costs (power and fuel) $5,000 per slow-speed trip $8,000 per high-speed trip Engineers and onboard service staff total $150,000 per month Onboard services Gourmet services contract $700,000 per month $8 per passengerTable 2. Ann Arbor Railroad Projected Business for March 20x0 VOLUME Slow-Speed High-Speed Trips 200 300 Total Passengers 75,000 100,000 (over all trips) Average Ticket Price $50 $180 Note: Passenger volumes and fares are averaged across trips. Trips and Average Ticket Price both refer to round trips. Case Requirements: 1. What is the total projected cost for March 20KB? (5 points) 2. What is the projected profitability per passenger (revenues minus costs) for the high-speed and slow-speed services for March 20KB? (5 points) Hint: you need to come up with reasonable assumptions to allocate all the common costs to the high-speed and slow-speed services. Make sure you clearly explain your assumptions. 3. Assume that you are the manager in charge of the high-speed service. On March 20th, MBA students from the Detroit area who are taking an Entrepreneurial Management elective course approach you with the following offer. The students want to reserve 20 seats for a round trip from Detroit to Chicago on March 2] st to conduct a market research study for their nal project. Specically, the MBA students have arranged for undergraduates to participate in the study, which is aimed at identifying factors that make train travel more attractive to customers. The MBA students are on a limited budget and propose to pay Ann Arbor Railroad $1,000 for the round trip for the 20 seats. Tickets sales for March let have been low, and, as of today, there are still over 100 seats available. Would you accept the students' offer? ( 3 points) 4. Using the information from Table 2, what is the number of tickets that Ann Arbor Railroad must sell to breakeven in each service line? What is volume of sales that Ann Arbor Railroad must generate to breakeven overall? (Low-speed BEP: 3 points; High speed REF: 3 points; overall REF: 3 points) Hint: to compute the breakeven point in each service line, do not allocate common costs to the two services. 5. Question 2 asked the projected protability per passenger. Why do we need projected cost and revenue gures? Why do we not just wait until the end of the mount/year to compute actual costs and revenues? (3 points) 1. Your Excel spreadsheet for your computations for Questions 1, 2, 3 and 4, with a separate tab for each question. 2. Your Word document, where you use those numbers obtained from your Excel spreadsheet B30 X V fx B C D E G Cost type Cost elements FC (@) UVC (b) Activity level (X) Total cost (a+bX) Head office-related (Detroit station) Administrative personnel, marketing costs, IT costs Roadbed, track, and signaling equipment-related Depreciation of track & signaling equipment Interest Payments Maintenance Workers Repair Materials Station-related Detroit Chicago All other stations combined Train-related Leasing costs - slow-speed train Leasing costs - high-speed train Hauling costs - slow-speed Hauling costs - high-speed trip Engineers and onboard service staff total Onboard Services Gourmet services contract TotalQuestion 1 Question 2 Question 3 Question 4 Cost type Cost elements FC (a) UVC (b) Activity level (X) Total cost (a+bX) Head office-related (Detroit station) Administrative personnel, marketing costs, IT costs Roadbed, track, and signaling equipment-related Depreciation of track & signaling equipment Interest Payments Maintenance Workers Repair Materials Station-related Detroit Chicago All other stations combined Train-related Leasing costs - slow-speed train Leasing costs - high-speed train Hauling costs - slow-speed Hauling costs - high-speed trip Engineers and onboard service staff total Onboard Services Gourmet services contract TotalQuestion 1 Question 2 Question 3 Question 4 Slow-speed High-speed Revenue: Costs: Variable Costs Cost Driver No. of cost drivers Unit cost $ total No. of cost drivers Unit cost $ total Hauling costs # of trips 200 5 000 1 000 000 Repair Materials Total Variable Costs Fixed Costs Allocation Total Costs $ Leasing Costs # of Trains 50% 50% 50% 50% 50% N/A 50% N/A Total Fixed Costs Total Costs: Variable + Fixed Cost per passenger put down equation in this cell put down equation in this cell Profitability: Operating Income (Revenues-Costs) put down equation in this cell put down equation in this cell Profitability per passenger put down equation in this cell put down equation in this cellQuestion 1 Question 2 Question 3 Question 4 Special-order decision Accept Reject Per passenger Number of Total Per passenger Number of Total (Round trip) passengers (Round trip) passengers Relevant revenue: Ticket sales revenues Relevant cost: Complimentary catering Net benefitQuestion 1 Question 2 Question 3 Question 4 Slow-speed % High-speed % Total % Revenue Costs: Variable Costs Contribution Margin Traceable Fixed Costs Segment Margin Common Fixed Costs Operating Income Sales Mix Slow-speed High-speed Segments Breakeven # Of Tickets Sales # Of Tickets Sales Sales Company Breakeven

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts