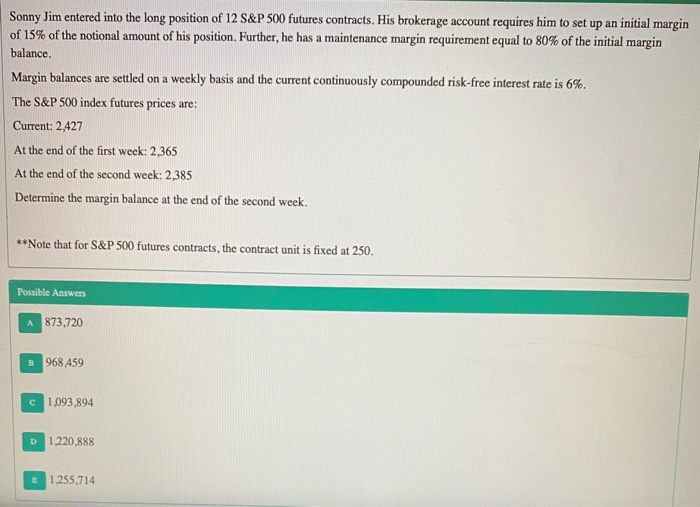

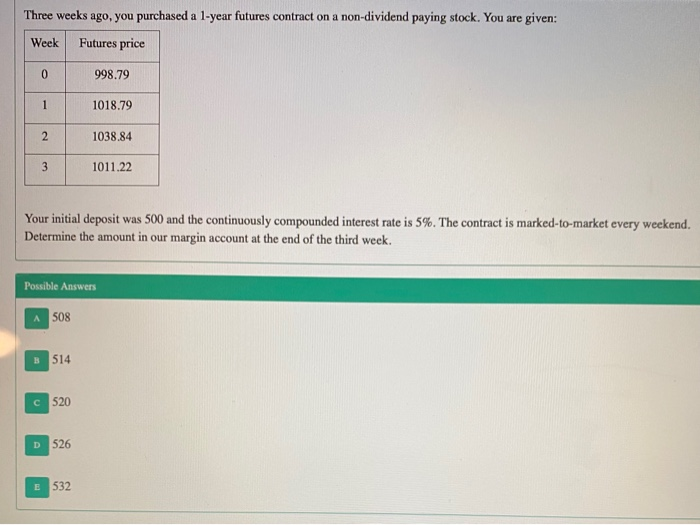

Question: answer all 3 for an upvote Three weeks ago, you purchased a 1-year futures contract on a non-dividend paying stock. You are given: Week Futures

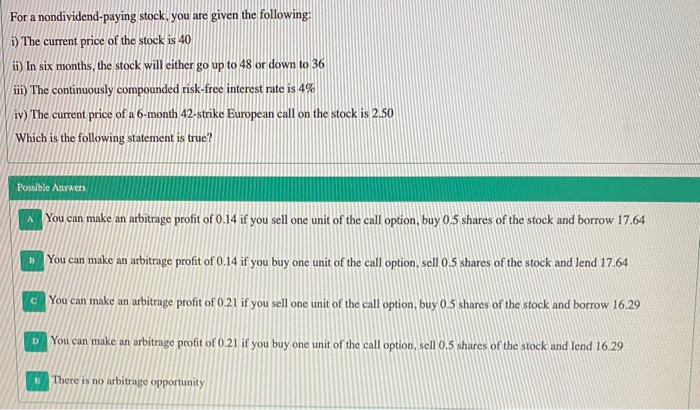

Three weeks ago, you purchased a 1-year futures contract on a non-dividend paying stock. You are given: Week Futures price 0 998.79 1 1018.79 2 1038.84 3 1011.22 Your initial deposit was 500 and the continuously compounded interest rate is 5%. The contract is marked-to-market every weekend. Determine the amount in our margin account at the end of the third week. Possible Answers 508 3514 C 520 D 526 E532 For a nondividend-paying stock, you are given the following: i) The current price of the stock is 40 ii) In six months, the stock will either go up to 48 or down to 36 iii) The continuously compounded risk-free interest rate is 4% iv) The current price of a 6-month 42-strike European call on the stock is 2.50 Which is the following statement is true? Possible Answers A You can make an arbitrage profit of 0.14 if you sell one unit of the call option, buy 0.5 shares of the stock and borrow 17.64 You can make an arbitrage profit of 0.14 if you buy one unit of the call option, sell 0.5 shares of the stock and lend 17.64 c You can make an arbitrage profit of 0.21 if you sell one unit of the call option, buy 0.5 shares of the stock and borrow 16.29 You can make an arbitrage profit of 0 21 if you buy one unit of the call option, sell 0.5 shares of the stock and lend 16.29 There is no arbitrage opportunity

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts