Question: Answer c branch only, provided that the answer is on excel Consider the following probability distribution for stocks X and Y: Return on Stock X

Answer c branch only, provided that the answer is on excel

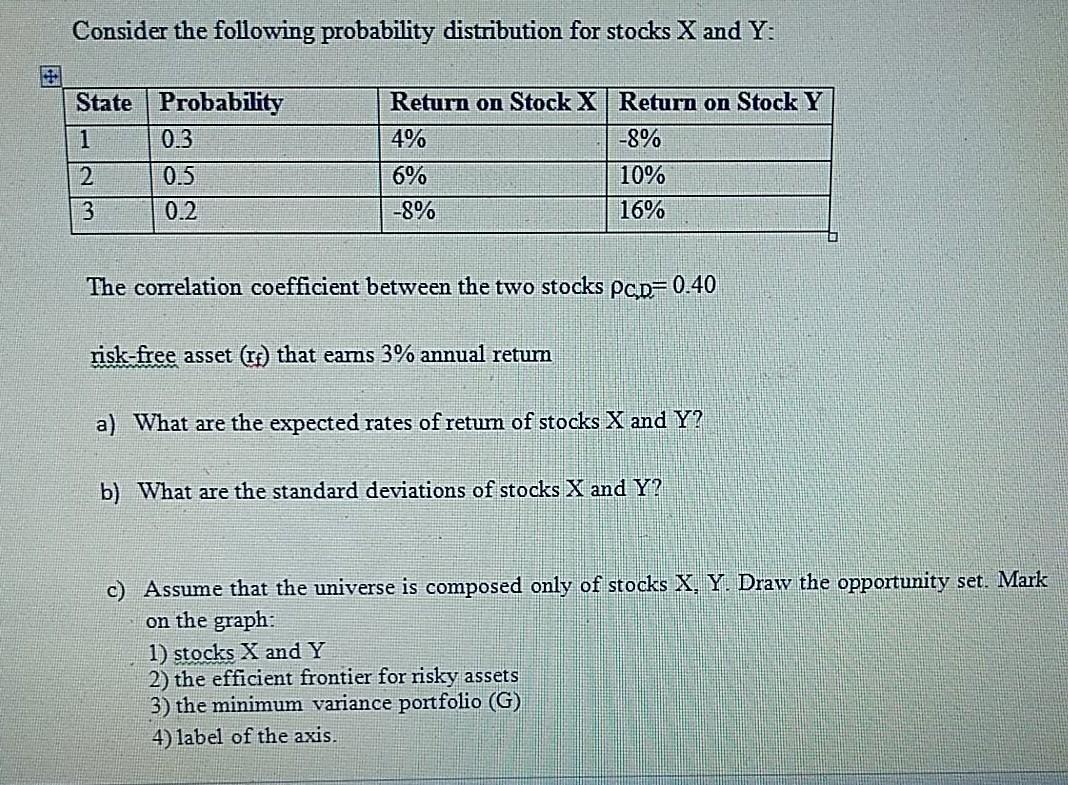

Consider the following probability distribution for stocks X and Y: Return on Stock X Return on Stock Y State Probability 1 0.3 4% -8% 2 0.5 6% 10% 3 0.2 -8% 16% The correlation coefficient between the two stocks PCD=0.40 risk-free asset (If) that eams 3% annual retum a) What are the expected rates of retum of stocks X and Y? b) What are the standard deviations of stocks X and Y? c) Assume that the universe is composed only of stocks X, Y. Draw the opportunity set. Mark on the graph: 1) stocks X and Y 2) the efficient frontier for risky assets 3) the minimum variance portfolio (G) 4) label of the axis

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts