Question: Answer is 1.4. Please explain how to solve, thank you. LCL - Lower confidence interval (95%) UCL - Upper confidence interval (95%) The table above

Answer is 1.4. Please explain how to solve, thank you.

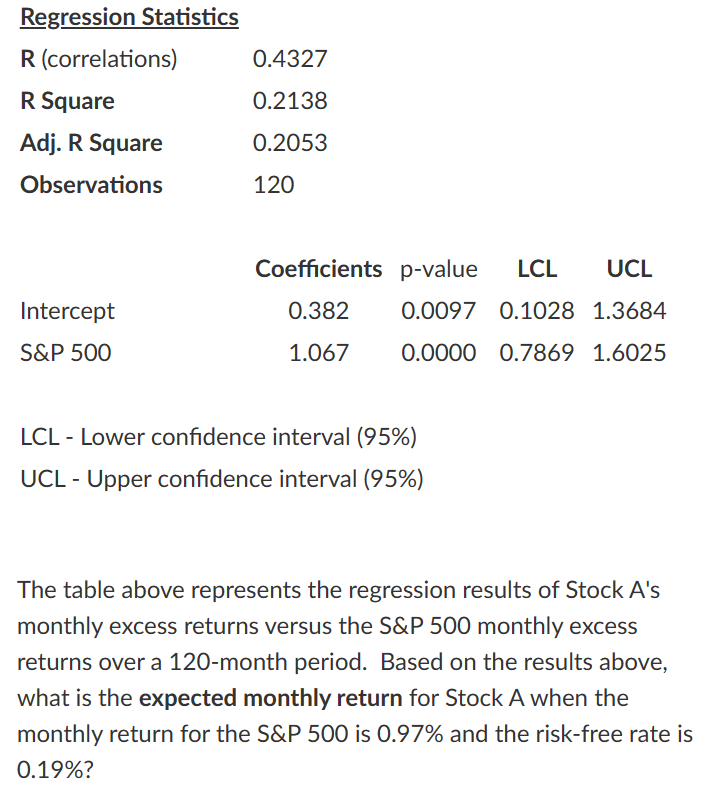

LCL - Lower confidence interval (95\%) UCL - Upper confidence interval (95\%) The table above represents the regression results of Stock A's monthly excess returns versus the S\&P 500 monthly excess returns over a 120-month period. Based on the results above, what is the expected monthly return for Stock A when the monthly return for the S\&P 500 is 0.97% and the risk-free rate is 0.19%

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock