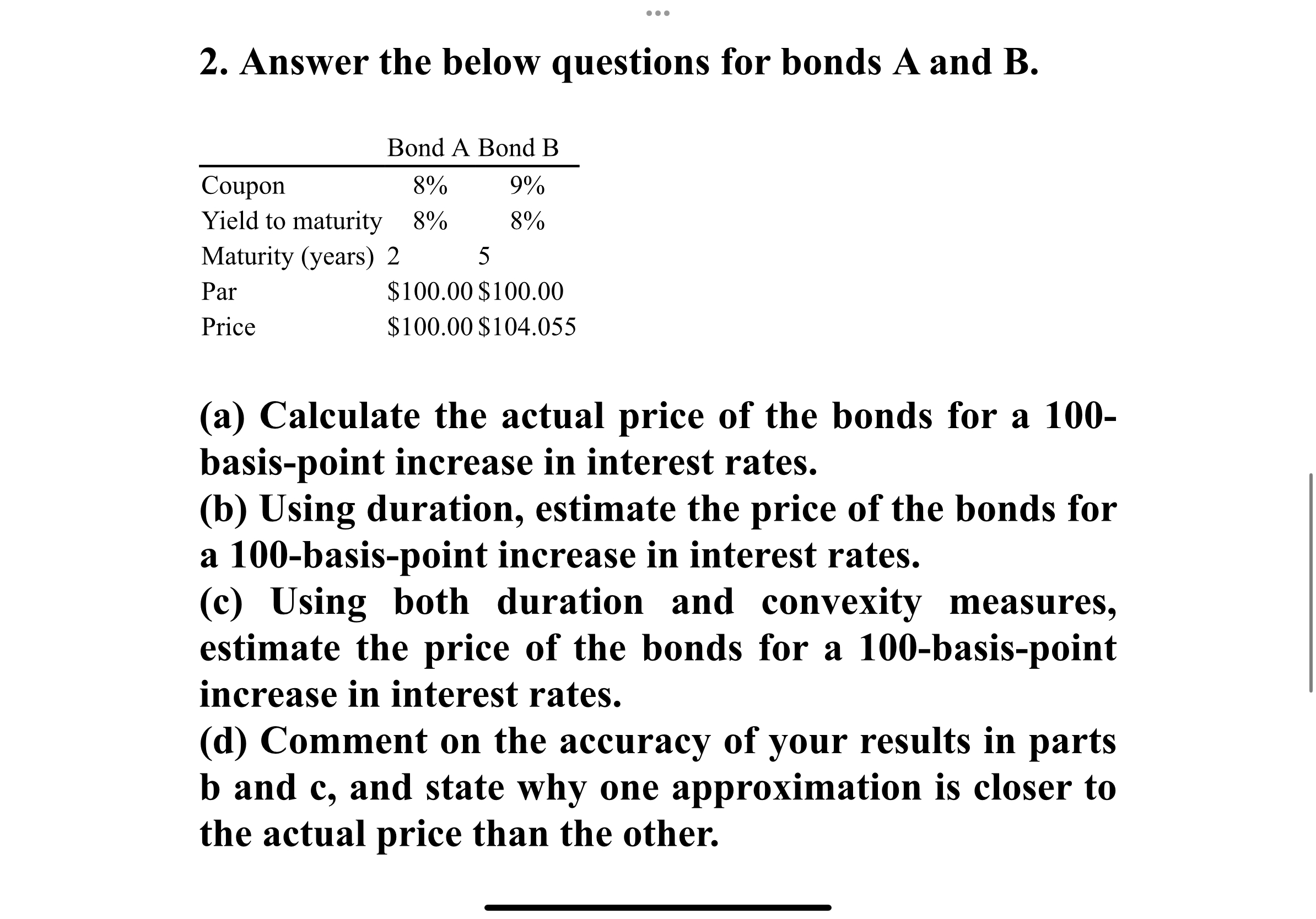

Question: Answer the below questions for bonds A and B . table [ [ , Bond A Bond B ] , [ Coupon , 8

Answer the below questions for bonds A and

tableBond A Bond BCouponYield to maturity,Maturity yearsPar$$Price$$

a Calculate the actual price of the bonds for a basispoint increase in interest rates.

b Using duration, estimate the price of the bonds for a basispoint increase in interest rates.

c Using both duration and convexity measures, estimate the price of the bonds for a basispoint increase in interest rates.

d Comment on the accuracy of your results in parts and and state why one approximation is closer to the actual price than the other.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock