Question: answer the highlighted please Assuming a correlation coefficient of -1.00 and the information given below, compute the following information regarding the minimum variance portfolio (MINVAR).

answer the highlighted please

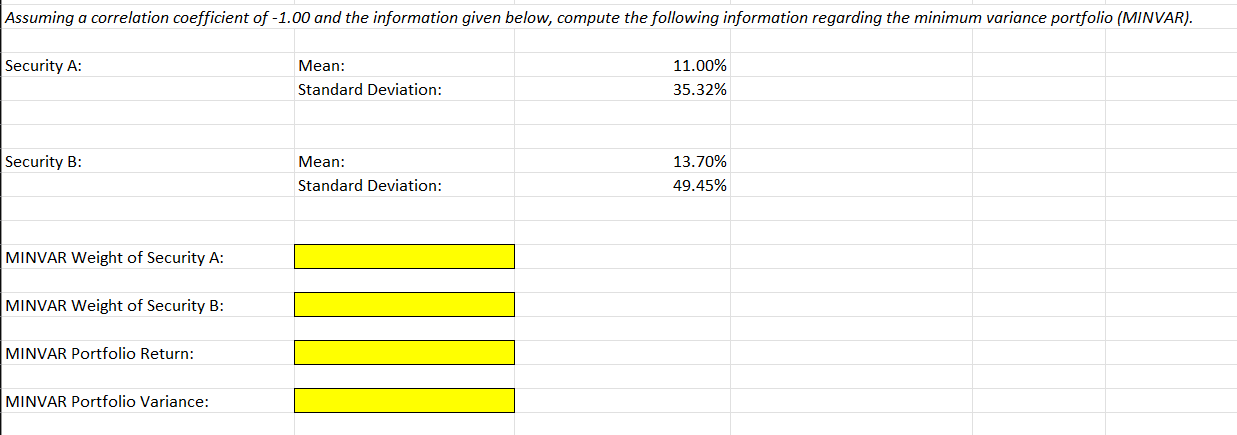

Assuming a correlation coefficient of -1.00 and the information given below, compute the following information regarding the minimum variance portfolio (MINVAR). Security A : \begin{tabular}{l|l} \hline Mean: & 11.00% \\ \hline Standard Deviation: & 35.32% \end{tabular} Security B: \begin{tabular}{l|r} \hline Mean: & 13.70% \\ \hline Standard Deviation: & 49.45% \\ \hline \end{tabular} MINVAR Weight of Security A: MINVAR Weight of Security B: MINVAR Portfolio Return: MINVAR Portfolio Variance

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock