Question: Answer the whole thing please, its all one question. Thank you for helping 1) The current price of a share of stock is 100 .

Answer the whole thing please, its all one question. Thank you for helping

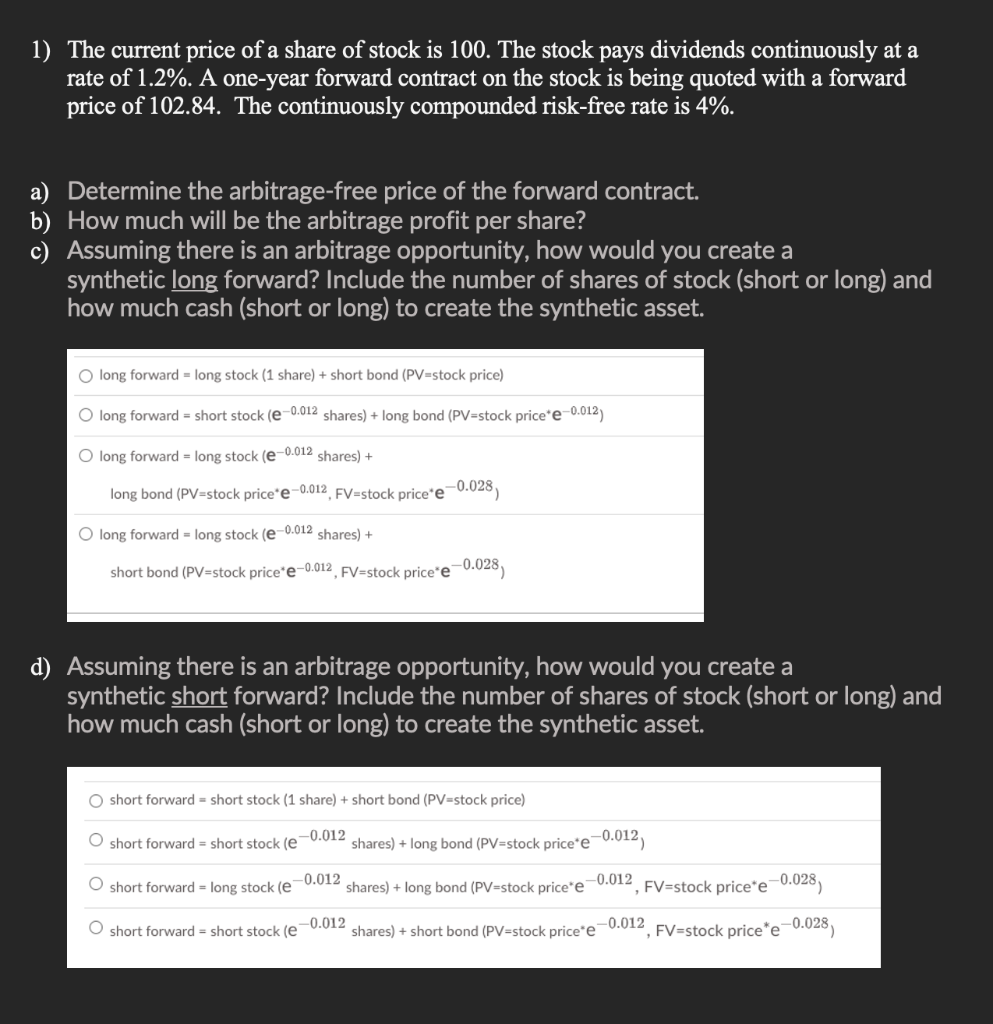

1) The current price of a share of stock is 100 . The stock pays dividends continuously at a rate of 1.2%. A one-year forward contract on the stock is being quoted with a forward price of 102.84. The continuously compounded risk-free rate is 4%. a) Determine the arbitrage-free price of the forward contract. b) How much will be the arbitrage profit per share? c) Assuming there is an arbitrage opportunity, how would you create a synthetic long forward? Include the number of shares of stock (short or long) and how much cash (short or long) to create the synthetic asset. long forward = long stock ( 1 share )+ short bond (PV=stock price) long forward = short stock (e0.012 shares )+ long bond (PV= stock price +e0.012) long forward = long stock (e0.012 shares )+ long bond ( PV= stock price e0.012,FV= stock price e0.028 ) long forward = long stock (e0.012 shares )+ short bond (PV= stock price e0.012,FV= stock price e0.028) d) Assuming there is an arbitrage opportunity, how would you create a synthetic short forward? Include the number of shares of stock (short or long) and how much cash (short or long) to create the synthetic asset. short forward = short stock (1 share )+ short bond (PV= stock price) shortforward=shortstock(e0.012shares)+longbond(PV=stockpricee0.012)shortforward=longstock(e0.012shares)+longbond(PV=stockpricee0.012,FV=stockpricee0.028)shortforward=shortstock(e0.012shares)+shortbond(PV=stockprice*e0.012,FV=stockprice*e0.028)

Step by Step Solution

There are 3 Steps involved in it

To solve these questions well go step by step a Determine the arbitragefree price of the forward con... View full answer

Get step-by-step solutions from verified subject matter experts