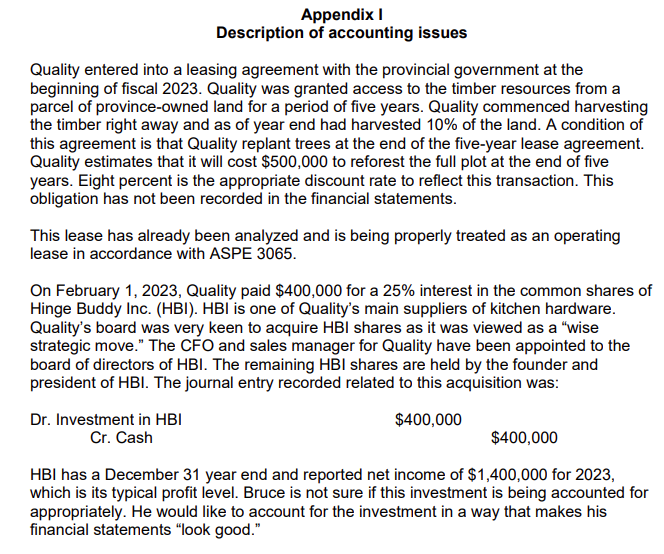

Appendix I Description of accounting issues Quality entered into a leasing agreement with the provincial government...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

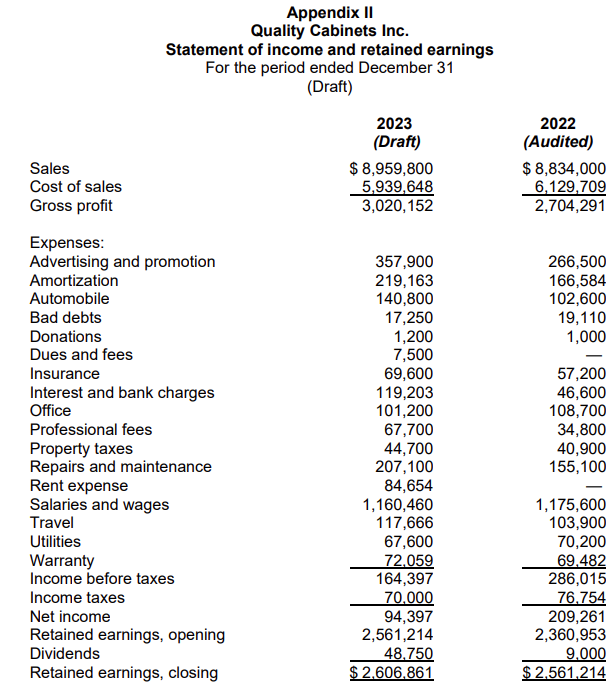

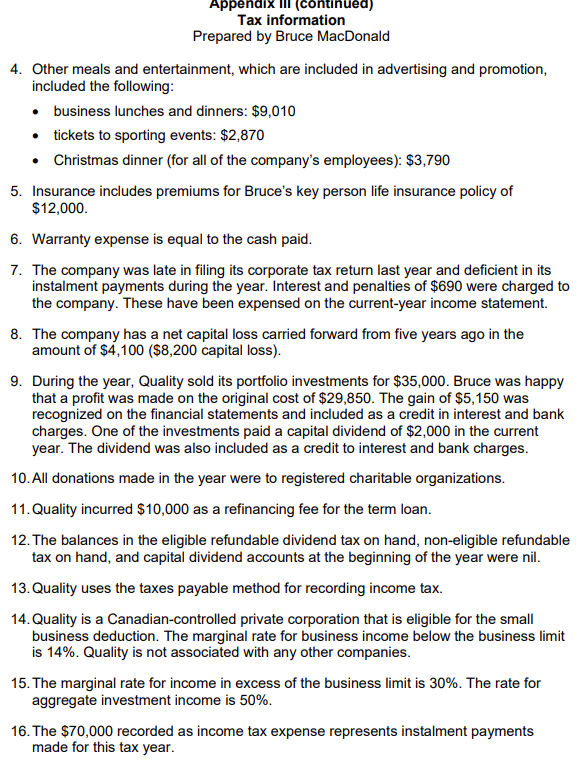

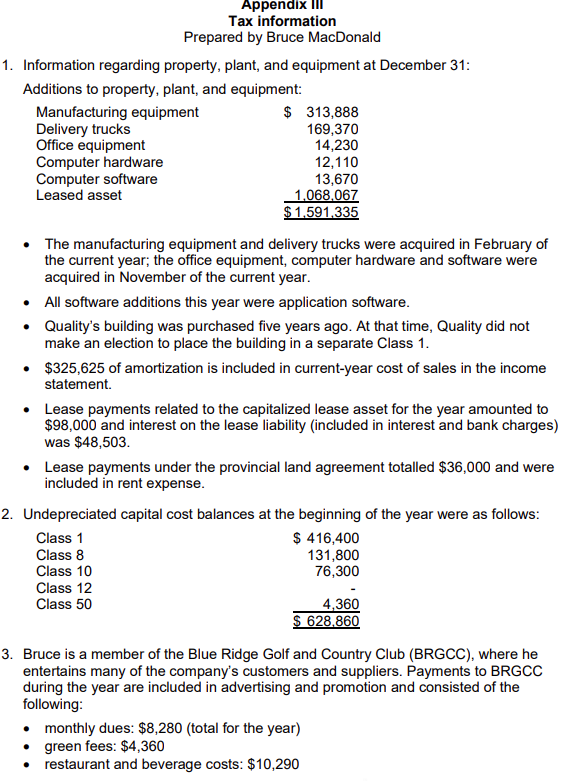

Appendix I Description of accounting issues Quality entered into a leasing agreement with the provincial government at the beginning of fiscal 2023. Quality was granted access to the timber resources from a parcel of province-owned land for a period of five years. Quality commenced harvesting the timber right away and as of year end had harvested 10% of the land. A condition of this agreement is that Quality replant trees at the end of the five-year lease agreement. Quality estimates that it will cost $500,000 to reforest the full plot at the end of five years. Eight percent is the appropriate discount rate to reflect this transaction. This obligation has not been recorded in the financial statements. This lease has already been analyzed and is being properly treated as an operating lease in accordance with ASPE 3065. On February 1, 2023, Quality paid $400,000 for a 25% interest in the common shares of Hinge Buddy Inc. (HBI). HBI is one of Quality's main suppliers of kitchen hardware. Quality's board was very keen to acquire HBI shares as it was viewed as a "wise strategic move." The CFO and sales manager for Quality have been appointed to the board of directors of HBI. The remaining HBI shares are held by the founder and president of HBI. The journal entry recorded related to this acquisition was: Dr. Investment in HBI Cr. Cash $400,000 $400,000 HBI has a December 31 year end and reported net income of $1,400,000 for 2023, which is its typical profit level. Bruce is not sure if this investment is being accounted for appropriately. He would like to account for the investment in a way that makes his financial statements "look good." Sales Cost of sales Appendix II Quality Cabinets Inc. Statement of income and retained earnings For the period ended December 31 (Draft) 2023 (Draft) $ 8,959,800 5,939,648 3,020,152 2022 (Audited) $ 8,834,000 6,129,709 2,704,291 Gross profit Expenses: Advertising and promotion 357,900 266,500 Amortization 219,163 166,584 Automobile 140,800 102,600 Bad debts 17,250 19,110 Donations 1,200 1,000 Dues and fees 7,500 Insurance 69,600 57,200 Interest and bank charges 119,203 46,600 Office 101,200 108,700 Professional fees 67,700 34,800 Property taxes 44,700 40,900 Repairs and maintenance 207,100 155,100 Rent expense 84,654 Salaries and wages 1,160,460 1,175,600 Travel 117,666 103,900 Utilities 67,600 70,200 Warranty 72,059 69,482 Income before taxes Income taxes Net income Retained earnings, opening Dividends Retained earnings, closing $ 2,606,861 164,397 286,015 70,000 76,754 94,397 209,261 2,561,214 2,360,953 48,750 9,000 $2,561,214 Appendix III (continued) Tax information Prepared by Bruce MacDonald 4. Other meals and entertainment, which are included in advertising and promotion, included the following: business lunches and dinners: $9,010 tickets to sporting events: $2,870 Christmas dinner (for all of the company's employees): $3,790 5. Insurance includes premiums for Bruce's key person life insurance policy of $12,000. 6. Warranty expense is equal to the cash paid. 7. The company was late in filing its corporate tax return last year and deficient in its instalment payments during the year. Interest and penalties of $690 were charged to the company. These have been expensed on the current-year income statement. 8. The company has a net capital loss carried forward from five years ago in the amount of $4,100 ($8,200 capital loss). 9. During the year, Quality sold its portfolio investments for $35,000. Bruce was happy that a profit was made on the original cost of $29,850. The gain of $5,150 was recognized on the financial statements and included as a credit in interest and bank charges. One of the investments paid a capital dividend of $2,000 in the current year. The dividend was also included as a credit to interest and bank charges. 10. All donations made in the year were to registered charitable organizations. 11. Quality incurred $10,000 as a refinancing fee for the term loan. 12. The balances in the eligible refundable dividend tax on hand, non-eligible refundable tax on hand, and capital dividend accounts at the beginning of the year were nil. 13. Quality uses the taxes payable method for recording income tax. 14. Quality is a Canadian-controlled private corporation that is eligible for the small business deduction. The marginal rate for business income below the business limit is 14%. Quality is not associated with any other companies. 15. The marginal rate for income in excess of the business limit is 30%. The rate for aggregate investment income is 50%. 16. The $70,000 recorded as income tax expense represents instalment payments made for this tax year. Appendix III Tax information Prepared by Bruce MacDonald 1. Information regarding property, plant, and equipment at December 31: Additions to property, plant, and equipment: Manufacturing equipment Delivery trucks Office equipment Computer hardware Computer software Leased asset $ 313,888 169,370 14,230 12,110 13,670 1,068,067 $1,591,335 The manufacturing equipment and delivery trucks were acquired in February of the current year; the office equipment, computer hardware and software were acquired in November of the current year. All software additions this year were application software. Quality's building was purchased five years ago. At that time, Quality did not make an election to place the building in a separate Class 1. $325,625 of amortization is included in current-year cost of sales in the income statement. Lease payments related to the capitalized lease asset for the year amounted to $98,000 and interest on the lease liability (included in interest and bank charges) was $48,503. Lease payments under the provincial land agreement totalled $36,000 and were included in rent expense. 2. Undepreciated capital cost balances at the beginning of the year were as follows: Class 1 Class 8 Class 10 Class 12 $ 416,400 131,800 76,300 Class 50 4,360 $ 628,860 3. Bruce is a member of the Blue Ridge Golf and Country Club (BRGCC), where he entertains many of the company's customers and suppliers. Payments to BRGCC during the year are included in advertising and promotion and consisted of the following: monthly dues: $8,280 (total for the year) green fees: $4,360 restaurant and beverage costs: $10,290 Appendix I Description of accounting issues Quality entered into a leasing agreement with the provincial government at the beginning of fiscal 2023. Quality was granted access to the timber resources from a parcel of province-owned land for a period of five years. Quality commenced harvesting the timber right away and as of year end had harvested 10% of the land. A condition of this agreement is that Quality replant trees at the end of the five-year lease agreement. Quality estimates that it will cost $500,000 to reforest the full plot at the end of five years. Eight percent is the appropriate discount rate to reflect this transaction. This obligation has not been recorded in the financial statements. This lease has already been analyzed and is being properly treated as an operating lease in accordance with ASPE 3065. On February 1, 2023, Quality paid $400,000 for a 25% interest in the common shares of Hinge Buddy Inc. (HBI). HBI is one of Quality's main suppliers of kitchen hardware. Quality's board was very keen to acquire HBI shares as it was viewed as a "wise strategic move." The CFO and sales manager for Quality have been appointed to the board of directors of HBI. The remaining HBI shares are held by the founder and president of HBI. The journal entry recorded related to this acquisition was: Dr. Investment in HBI Cr. Cash $400,000 $400,000 HBI has a December 31 year end and reported net income of $1,400,000 for 2023, which is its typical profit level. Bruce is not sure if this investment is being accounted for appropriately. He would like to account for the investment in a way that makes his financial statements "look good." Sales Cost of sales Appendix II Quality Cabinets Inc. Statement of income and retained earnings For the period ended December 31 (Draft) 2023 (Draft) $ 8,959,800 5,939,648 3,020,152 2022 (Audited) $ 8,834,000 6,129,709 2,704,291 Gross profit Expenses: Advertising and promotion 357,900 266,500 Amortization 219,163 166,584 Automobile 140,800 102,600 Bad debts 17,250 19,110 Donations 1,200 1,000 Dues and fees 7,500 Insurance 69,600 57,200 Interest and bank charges 119,203 46,600 Office 101,200 108,700 Professional fees 67,700 34,800 Property taxes 44,700 40,900 Repairs and maintenance 207,100 155,100 Rent expense 84,654 Salaries and wages 1,160,460 1,175,600 Travel 117,666 103,900 Utilities 67,600 70,200 Warranty 72,059 69,482 Income before taxes Income taxes Net income Retained earnings, opening Dividends Retained earnings, closing $ 2,606,861 164,397 286,015 70,000 76,754 94,397 209,261 2,561,214 2,360,953 48,750 9,000 $2,561,214 Appendix III (continued) Tax information Prepared by Bruce MacDonald 4. Other meals and entertainment, which are included in advertising and promotion, included the following: business lunches and dinners: $9,010 tickets to sporting events: $2,870 Christmas dinner (for all of the company's employees): $3,790 5. Insurance includes premiums for Bruce's key person life insurance policy of $12,000. 6. Warranty expense is equal to the cash paid. 7. The company was late in filing its corporate tax return last year and deficient in its instalment payments during the year. Interest and penalties of $690 were charged to the company. These have been expensed on the current-year income statement. 8. The company has a net capital loss carried forward from five years ago in the amount of $4,100 ($8,200 capital loss). 9. During the year, Quality sold its portfolio investments for $35,000. Bruce was happy that a profit was made on the original cost of $29,850. The gain of $5,150 was recognized on the financial statements and included as a credit in interest and bank charges. One of the investments paid a capital dividend of $2,000 in the current year. The dividend was also included as a credit to interest and bank charges. 10. All donations made in the year were to registered charitable organizations. 11. Quality incurred $10,000 as a refinancing fee for the term loan. 12. The balances in the eligible refundable dividend tax on hand, non-eligible refundable tax on hand, and capital dividend accounts at the beginning of the year were nil. 13. Quality uses the taxes payable method for recording income tax. 14. Quality is a Canadian-controlled private corporation that is eligible for the small business deduction. The marginal rate for business income below the business limit is 14%. Quality is not associated with any other companies. 15. The marginal rate for income in excess of the business limit is 30%. The rate for aggregate investment income is 50%. 16. The $70,000 recorded as income tax expense represents instalment payments made for this tax year. Appendix III Tax information Prepared by Bruce MacDonald 1. Information regarding property, plant, and equipment at December 31: Additions to property, plant, and equipment: Manufacturing equipment Delivery trucks Office equipment Computer hardware Computer software Leased asset $ 313,888 169,370 14,230 12,110 13,670 1,068,067 $1,591,335 The manufacturing equipment and delivery trucks were acquired in February of the current year; the office equipment, computer hardware and software were acquired in November of the current year. All software additions this year were application software. Quality's building was purchased five years ago. At that time, Quality did not make an election to place the building in a separate Class 1. $325,625 of amortization is included in current-year cost of sales in the income statement. Lease payments related to the capitalized lease asset for the year amounted to $98,000 and interest on the lease liability (included in interest and bank charges) was $48,503. Lease payments under the provincial land agreement totalled $36,000 and were included in rent expense. 2. Undepreciated capital cost balances at the beginning of the year were as follows: Class 1 Class 8 Class 10 Class 12 $ 416,400 131,800 76,300 Class 50 4,360 $ 628,860 3. Bruce is a member of the Blue Ridge Golf and Country Club (BRGCC), where he entertains many of the company's customers and suppliers. Payments to BRGCC during the year are included in advertising and promotion and consisted of the following: monthly dues: $8,280 (total for the year) green fees: $4,360 restaurant and beverage costs: $10,290

Expert Answer:

Related Book For

Modern Advanced Accounting In Canada

ISBN: 9781259066481

7th Edition

Authors: Hilton Murray, Herauf Darrell

Posted Date:

Students also viewed these accounting questions

-

Quality Cabinets Inc. (Quality) manufactures custom kitchen cabinets from its location in Squamish, British Columbia. The cabinets are then sold to contractors who install them in kitchens. Bruce...

-

Solve parts b and d of Problem 2.67 assuming that the free end of the rope is attached to the crate. Problem 2.67: A 280-kg crate is supported by several rope-and-pulley arrangements as shown....

-

The balance sheets of Cheever and Ham Companies as of December 31, 20xx, are as follows. Liabilities and Stockholders' Equity Assume that Cheever Company purchased 100 percent of Ham's common stock...

-

The elements of an array are stored in consecutive storage locations in the computers internal memory. True or False

-

In 2014, Barker contacted Price about a van Price had advertised for sale. The advertisement described the van as a 1994 Ford E350. Barker and Price agreed to meet, and, on April 9, Barker inspected...

-

The standard cost data for Madison Machinery Company show the following costs for producing one of its machines: Direct materials. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ....

-

Consider the region R on Earth including points whose coordinates, when rounded to a whole number of seconds, round to 1233'8" N, 8843'11" W. Determine with justification the perimeter of region R.

-

Classical conditioning is an inevitable theory in psychology. Do you agree with this statement or not? Support you answer with suitable REAL LIFE examples and reasons. Instructions: - Introduction of...

-

Assume that we know that for the period 19262010 the yield component for common stocks was 3.99 percent and that the cumulative wealth index was $2,420.46. The cumulative wealth index value for the...

-

A questionnaire was sent to 500 of a dry cleaners customers to solicit their opinions about service received. Twenty-three customers were found to be unhappy with the service. On this evidence, can...

-

You are working for a VCR manufacturer. There are three shifts in the plant: morning shift, evening shift, and midnight shift. The manager suspects that the midnight shifts productivity is lower than...

-

The dean of the school of business wants the proportion of A grades given out by his faculty members to be around 10 %. He randomly surveys 2,000 students in 50 classes and finds that of the 2,000...

-

A food company claims that its new product, low-fat yogurt, is 99 % fat-free. The management wants to keep the proportion of bad (not 99 % fat-free) products below 2 %. Inspectors check 500 cups of...

-

An employee earned $37,000 during the year working for an employer when the maximum limit for Social Security was $117,000. The FICA tax rate for Social Security is 6.2% and the FICA tax rate for...

-

Research corporate acquisitions using Web resources and then answer the following questions: Why do firms purchase other corporations? Do firms pay too much for the acquired corporation? Why do so...

-

PART A On January 1, Year 5, Anderson Corporation paid $650,000 for 20,000 (20%) of the outstanding shares of Carter Inc. The investment was considered to be one of significant influence. In Year 5,...

-

In what manner does the balance-sheet format used by companies in other countries differ from the format used by Canadian companies?

-

You have just completed an interview with the newly formed audit committee of the Andrews Street Youth Centre (ASYC). This organization was created to keep neighborhood youth off the streets by...

-

The microfinance concept has been a blessing for many people in developing countries. Its success there causes some to wonder if it can spur growth in areas of developed nations that need...

-

An institution that many people know little about and some governments find worrisome is offshore financial centers. They operate with little oversight, few regulations, and often little taxation....

-

What is the appeal of the eurocurrency market?

Study smarter with the SolutionInn App