Question: Applied Probability Consider the Black-Scholes model for the price Sn of a risky asset after n trading days: Sn = YlY2 . . . Yn,

Applied Probability

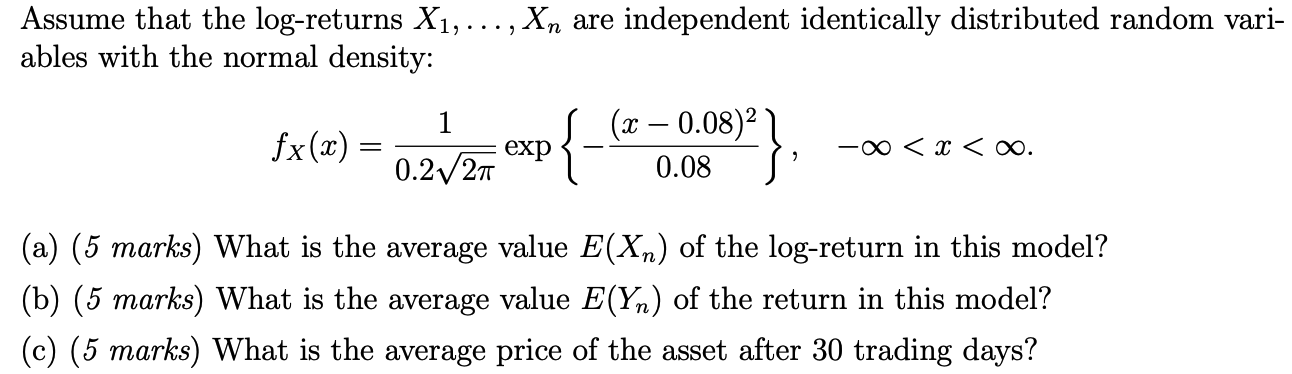

Consider the Black-Scholes model for the price Sn of a risky asset after n trading days: Sn = YlY2 . . . Yn, where Yi = exiAssume that the log-returns X1, ..., An are independent identically distributed random vari- ables with the normal density: H (a - 0.08)2 fx (20) = 0.2V2TT exp -00

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock