Question: apter 3 Homework A Saved Help Save & Exit Submit Check my work 8 An insurance company is analyzing the following three bonds, each with

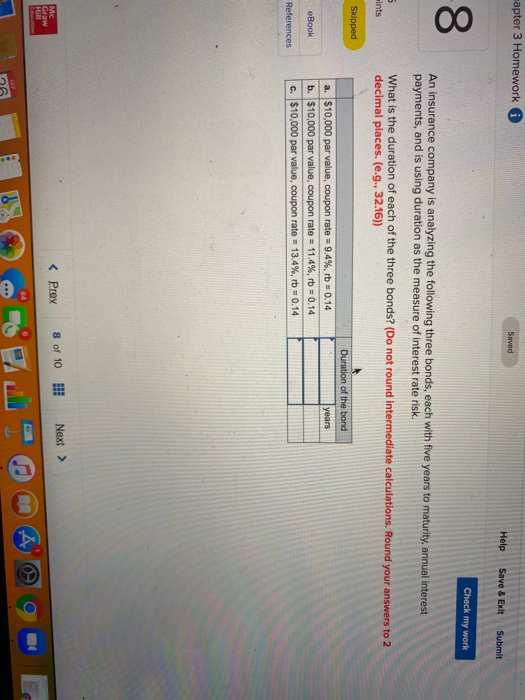

apter 3 Homework A Saved Help Save & Exit Submit Check my work 8 An insurance company is analyzing the following three bonds, each with five years to maturity, annual interest payments, and is using duration as the measure of interest rate risk. What is the duration of each of the three bonds? (Do not round intermediate calculations. Round your answers to 2 decimal places. (e.g., 32.16)) 5 ints Skipped Duration of the bond years eBook a. $10,000 par value, coupon rate = 9.4%, rb = 0.14 b. $10,000 par value, coupon rate = 11.4%, rb = 0.14 c. $10,000 par value, coupon rate = 13.4%, rb 0.14 References Mc Graw Hill con A a

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock