Question: As stated in the previous problem, a government issued $8.5 million of special assessment bonds to finance a sewar-extention project. To service the debt, it

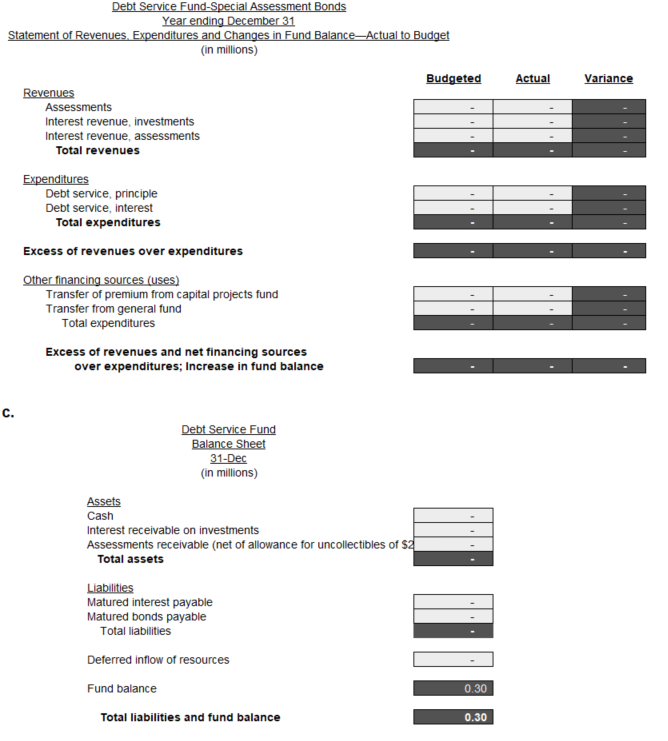

As stated in the previous problem, a government issued $8.5 million of special assessment bonds to finance a sewar-extention project. To service the debt, it assessed property owners $8.5 million. Their obligations are payable over a period of five years, with annual installments due on March 31 of each year. Interest at an annual rate of 8 percent is to be paid on the total balance outstanding as of that date. The bonds require an annual principle payment of $1.57 million each year for five years, due on December 31. In addition, interest on the unpaid balance is payable twice each year, on June 30 and December 31 at an annual rate of 8 percent. The government agreed to make up from its general fund the difference between required debt service payments and revenues. At the start of the year, the government established a debt-service fund. During the year it engaged in the following transactions, all of which would affect that fund. 1 It prepared, and recorded in its accounts, its annual budget. It estimated that it would collect from property owners $1.3 million in special assessments and $0.5 million of interest on the unpaid balance of the assessments. In addition, it expected to earn interest $0.08 million on temporary investments. It would be required to pay interest of $0.68 million and make principal payments of $1.7 million on the outstanding debt. It anticipated transferring $0.5 million from the general fund to cover the revenue shortage. 2. It recorded the $8.5 million of assessments receivable, estimating that $0.2 million would be uncollectible. 3. The special assessments bonds were issued at a premium (net of issue costs) of $0.12 million. ?The government recognized the anticipated transfer of the premium to the debt service fund. 4. During the year the government collected $2.0 million in assessments and $0.4 million in interest (with a few property owners paying their entire assessments in the first year). During the first 60 days of the following year it collected an additional $0.1 million in assessments and $0.01 million in interest, both of which were due the previous year. 5. It transferred $0.12 million (the premium) from the capital projects fund. 6. It purchased $0.8 million of six-month treasury bills as a temporary investment. 7. It made its first interest payment $0.34 million. 8. It sold the investments for $0.85 million, the difference between the selling price and cost representing interest earned. 9. It recognized its year-end obligation for interest of $0.34 million and principal of $1.7 million, but did not actually make the required payments. 10. It prepared year-end closing entries. a. Prepare appropriate journal entries for the debt service fund. b. Prepare a statement of revenues, expenditures, and changes in fund balance in which you compare actual and budgeted amounts for the year ended December 31. c. Prepare a year-end balance sheet.

The options for the drop downs for the journal entries are:

Allowance for uncollectible receivables Appropriations debt service interest Appropriations debt service principal Assessments not yet recognized as revenue Assessments receivable Cash Due from capital projects fund Estimated other financing sources nonreciprocal trans from gen fund a. Journal entries To record the annual budget |(2) To record the assessments receivable (3) To record anticipated transfer of bond premium from the capital projects fund |(4) To record collection of assessments and interest To recognize revenue earned on actual collections during the year plus those anticipated sufficiently soon after the end of the year so as to satisfy the "measurable and available" criteria |(5) To record the cash transfer from the capital projects fund [(6) To record the purchase of temporary investments (7) To record the first semi-annual payment of interest (8) To record the sale of investments (9) To record the obligation for the second semi-annual payment of interest and the first payment of principal (10) To close revenue and estimated revenue accounts To close expeniture and appropriation accounts Debt Service Fund-Special Assessment Bonds Year ending December 31 Statement of Revenues. Expenditures and Changes in Fund Balance Actual to Budget (in millions) Budgeted Actual Variance Revenues Assessments Interest revenue, investments Interest revenue, assessments Total revenues Expenditures Debt service, principle Debt service, interest Total expenditures Excess of revenues over expenditures Other financing sources (uses) Transfer of premium from capital projects fund Transfer from general fund Total expenditures Excess of revenues and net financing sources over expenditures; Increase in fund balance c. Debt Service Fund Balance Sheet 31-Dec (in millions) Assets Cash Interest receivable on investments Assessments receivable (net of allowance for uncollectibles of $2| Total assets Liabilities Matured interest payable Matured bonds payable Total liabilities Deferred inflow of resources Fund balance 0.30 Total liabilities and fund balance 0.30 Allowance for uncollectible receivables Appropriations debt service interest Appropriations debt service principal Assessments not yet recognized as revenue Assessments receivable Cash Due from capital projects fund Estimated other financing sources nonreciprocal trans from gen fund a. Journal entries To record the annual budget |(2) To record the assessments receivable (3) To record anticipated transfer of bond premium from the capital projects fund |(4) To record collection of assessments and interest To recognize revenue earned on actual collections during the year plus those anticipated sufficiently soon after the end of the year so as to satisfy the "measurable and available" criteria |(5) To record the cash transfer from the capital projects fund [(6) To record the purchase of temporary investments (7) To record the first semi-annual payment of interest (8) To record the sale of investments (9) To record the obligation for the second semi-annual payment of interest and the first payment of principal (10) To close revenue and estimated revenue accounts To close expeniture and appropriation accounts Debt Service Fund-Special Assessment Bonds Year ending December 31 Statement of Revenues. Expenditures and Changes in Fund Balance Actual to Budget (in millions) Budgeted Actual Variance Revenues Assessments Interest revenue, investments Interest revenue, assessments Total revenues Expenditures Debt service, principle Debt service, interest Total expenditures Excess of revenues over expenditures Other financing sources (uses) Transfer of premium from capital projects fund Transfer from general fund Total expenditures Excess of revenues and net financing sources over expenditures; Increase in fund balance c. Debt Service Fund Balance Sheet 31-Dec (in millions) Assets Cash Interest receivable on investments Assessments receivable (net of allowance for uncollectibles of $2| Total assets Liabilities Matured interest payable Matured bonds payable Total liabilities Deferred inflow of resources Fund balance 0.30 Total liabilities and fund balance 0.30

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts