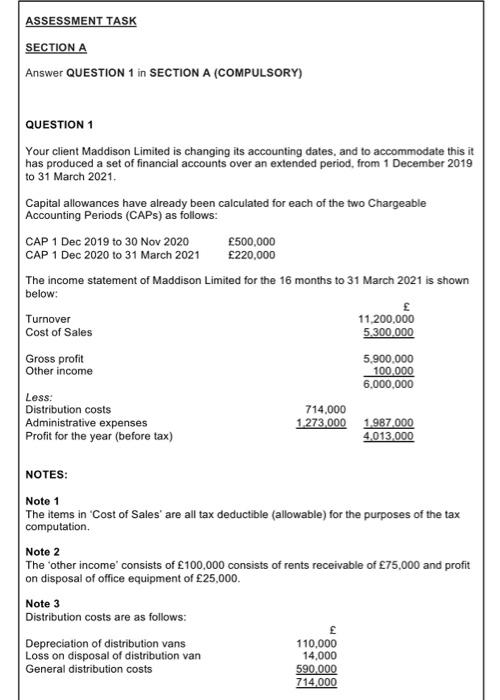

Question: ASSESSMENT TASK SECTION A Answer QUESTION 1 in SECTION A (COMPULSORY) QUESTION 1 Your client Maddison Limited is changing its accounting dates, and to accommodate

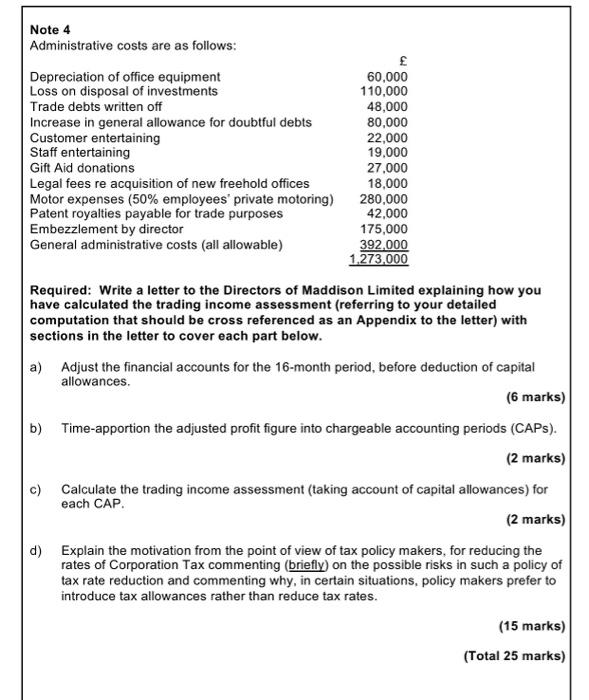

ASSESSMENT TASK SECTION A Answer QUESTION 1 in SECTION A (COMPULSORY) QUESTION 1 Your client Maddison Limited is changing its accounting dates, and to accommodate this it has produced a set of financial accounts over an extended period, from 1 December 2019 to 31 March 2021. Capital allowances have already been calculated for each of the two Chargeable Accounting Periods (CAPs) as follows: CAP 1 Dec 2019 to 30 Nov 2020 500,000 CAP 1 Dec 2020 to 31 March 2021 220,000 The income statement of Maddison Limited for the 16 months to 31 March 2021 is shown below: Turnover 11.200,000 Cost of Sales 5.300.000 Gross profit 5,900.000 Other income 100.000 6,000,000 Less: Distribution costs 714,000 Administrative expenses 1.273.000 1.987.000 Profit for the year (before tax) 4.013,000 NOTES: Note 1 The items in 'Cost of Sales' are all tax deductible (allowable) for the purposes of the tax computation Note 2 The other income' consists of 100,000 consists of rents receivable of 75,000 and profit on disposal of office equipment of 25,000 Note 3 Distribution costs are as follows: Depreciation of distribution vans 110.000 Loss on disposal of distribution van 14,000 General distribution costs 590.000 714,000 Note 4 Administrative costs are as follows: Depreciation of office equipment Loss on disposal of investments Trade debts written off Increase in general allowance for doubtful debts Customer entertaining Staff entertaining Gift Aid donations Legal fees re acquisition of new freehold offices Motor expenses (50% employees' private motoring) Patent royalties payable for trade purposes Embezzlement by director General administrative costs (all allowable) 60,000 110,000 48,000 80,000 22,000 19.000 27,000 18,000 280,000 42,000 175,000 392.000 1.273.000 Required: Write a letter to the Directors of Maddison Limited explaining how you have calculated the trading income assessment (referring to your detailed computation that should be cross referenced as an Appendix to the letter) with sections in the letter to cover each part below. a) Adjust the financial accounts for the 16-month period, before deduction of capital allowances. (6 marks) b) Time-apportion the adjusted profit figure into chargeable accounting periods (CAPs). (2 marks) Calculate the trading income assessment (taking account of capital allowances) for each CAP. (2 marks) d) Explain the motivation from the point of view of tax policy makers, for reducing the rates of Corporation Tax commenting (briefly) on the possible risks in such a policy of tax rate reduction and commenting why, in certain situations, policy makers prefer to introduce tax allowances rather than reduce tax rates. (15 marks) (Total 25 marks) ASSESSMENT TASK SECTION A Answer QUESTION 1 in SECTION A (COMPULSORY) QUESTION 1 Your client Maddison Limited is changing its accounting dates, and to accommodate this it has produced a set of financial accounts over an extended period, from 1 December 2019 to 31 March 2021. Capital allowances have already been calculated for each of the two Chargeable Accounting Periods (CAPs) as follows: CAP 1 Dec 2019 to 30 Nov 2020 500,000 CAP 1 Dec 2020 to 31 March 2021 220,000 The income statement of Maddison Limited for the 16 months to 31 March 2021 is shown below: Turnover 11.200,000 Cost of Sales 5.300.000 Gross profit 5,900.000 Other income 100.000 6,000,000 Less: Distribution costs 714,000 Administrative expenses 1.273.000 1.987.000 Profit for the year (before tax) 4.013,000 NOTES: Note 1 The items in 'Cost of Sales' are all tax deductible (allowable) for the purposes of the tax computation Note 2 The other income' consists of 100,000 consists of rents receivable of 75,000 and profit on disposal of office equipment of 25,000 Note 3 Distribution costs are as follows: Depreciation of distribution vans 110.000 Loss on disposal of distribution van 14,000 General distribution costs 590.000 714,000 Note 4 Administrative costs are as follows: Depreciation of office equipment Loss on disposal of investments Trade debts written off Increase in general allowance for doubtful debts Customer entertaining Staff entertaining Gift Aid donations Legal fees re acquisition of new freehold offices Motor expenses (50% employees' private motoring) Patent royalties payable for trade purposes Embezzlement by director General administrative costs (all allowable) 60,000 110,000 48,000 80,000 22,000 19.000 27,000 18,000 280,000 42,000 175,000 392.000 1.273.000 Required: Write a letter to the Directors of Maddison Limited explaining how you have calculated the trading income assessment (referring to your detailed computation that should be cross referenced as an Appendix to the letter) with sections in the letter to cover each part below. a) Adjust the financial accounts for the 16-month period, before deduction of capital allowances. (6 marks) b) Time-apportion the adjusted profit figure into chargeable accounting periods (CAPs). (2 marks) Calculate the trading income assessment (taking account of capital allowances) for each CAP. (2 marks) d) Explain the motivation from the point of view of tax policy makers, for reducing the rates of Corporation Tax commenting (briefly) on the possible risks in such a policy of tax rate reduction and commenting why, in certain situations, policy makers prefer to introduce tax allowances rather than reduce tax rates. (15 marks) (Total 25 marks)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts