Question: ASSIGNMENT FOUR Question 10 Soon after December 31, 2023, the auditor of Marigold Corp. asked the company to prepare a depreciation schedule for semi trucks

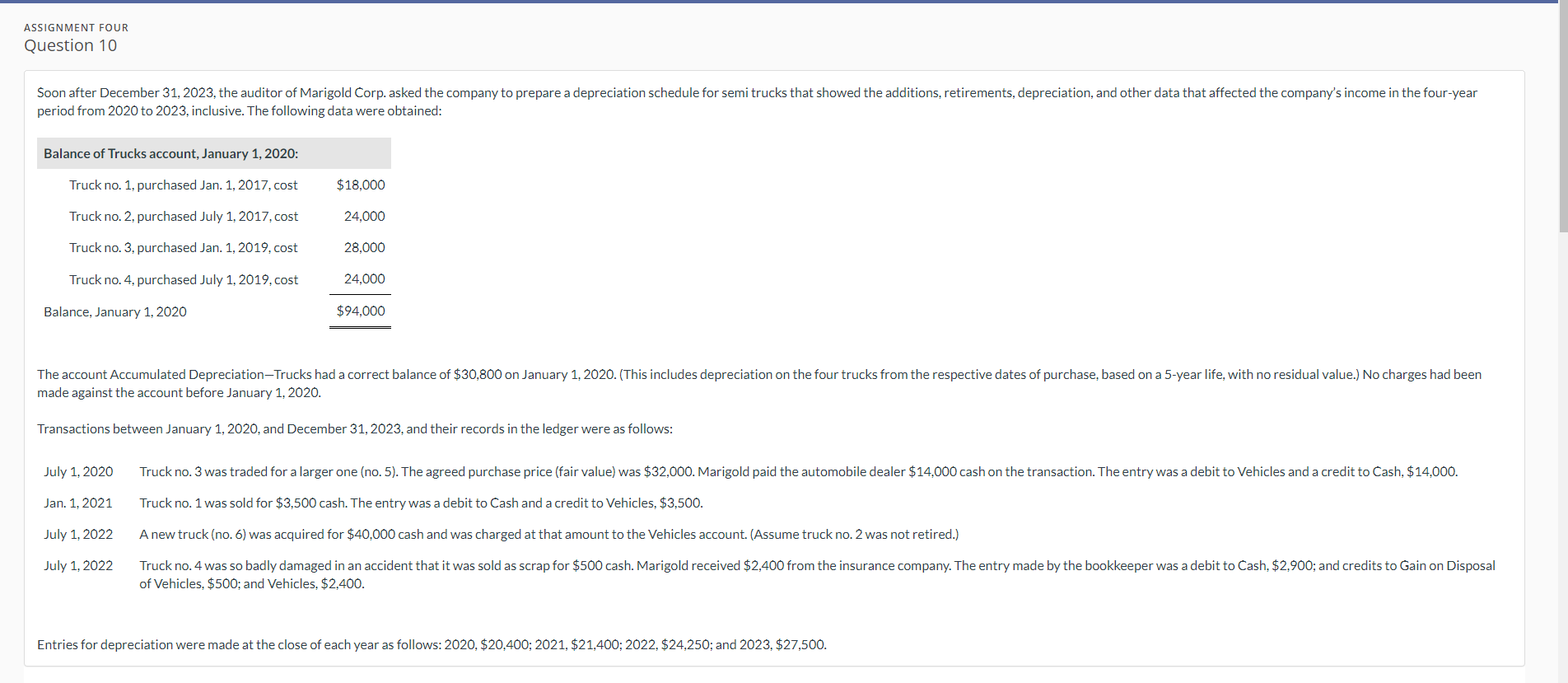

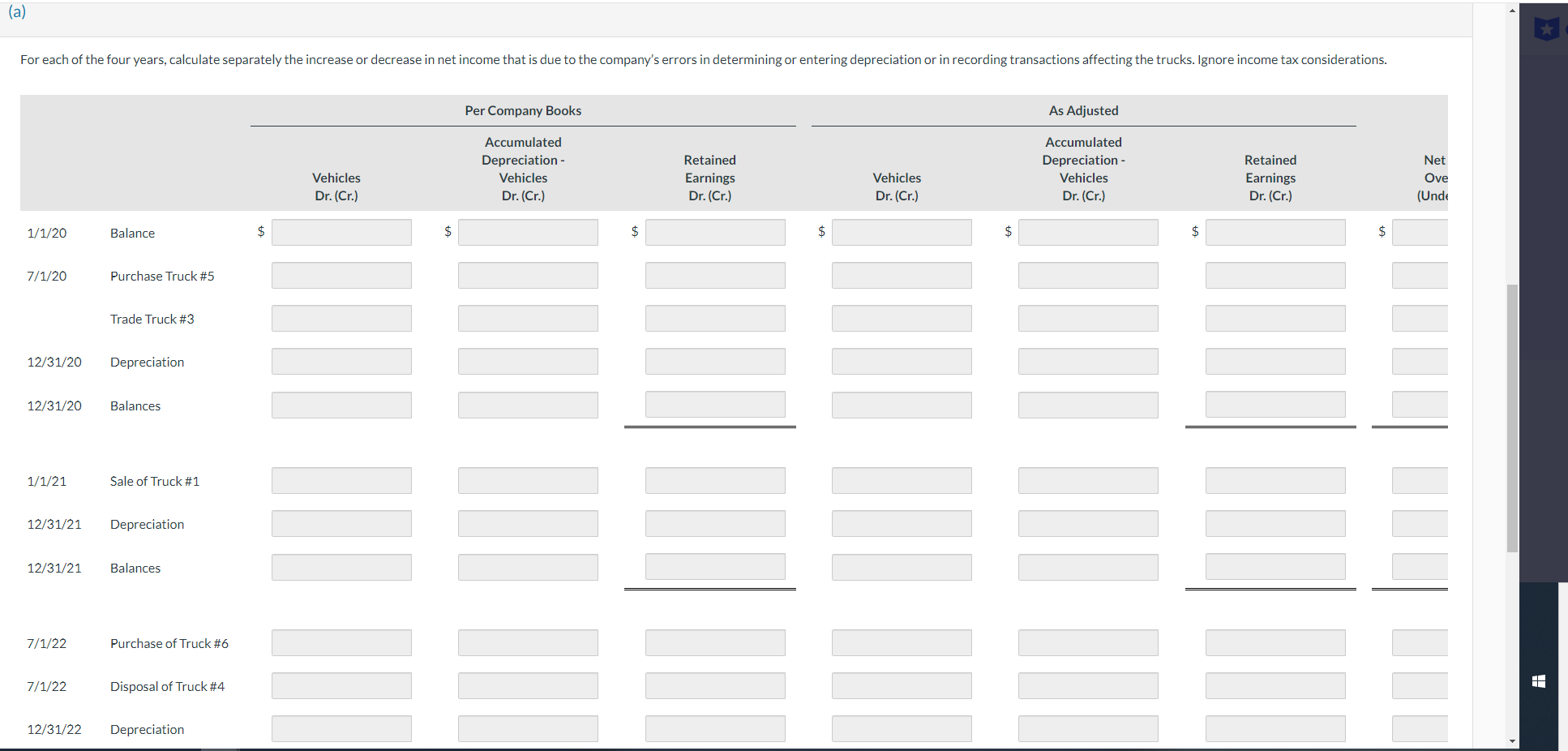

ASSIGNMENT FOUR Question 10 Soon after December 31, 2023, the auditor of Marigold Corp. asked the company to prepare a depreciation schedule for semi trucks that showed the ads period from 2020 to 2023, inclusive. The following data were obtained: ons, retirements, depreciation, and other data that affected the company's income in the four-year Balance of Trucks account, January 1, 2020: Truckno. 1, purchased Jan. 1, 2017, cost $18,000 Truck no. 2, purchased July 1, 2017, cost 24,000 Truck no. 3, purchased Jan. 1, 2019, cost 28.000 Truck no. 4, purchased July 1, 2019, cost 24,000 Balance, January 1, 2020 $94,000 The account Accumulated DepreciationTrucks had a correct balance of $30.800 on January 1, 2020. (This includes depreciation on the four trucks from the respective dates of purchase, based on a 5-year life, with no residual value.) No charges had been made against the account before January 1, 2020. Transactions between January 1, 2020, and December 31, 2023, and their records in the ledger were as follows: July 1,2020 Truck no. 3 was traded for a larger one (no. 5). The agreed purchase price (fair value} was $32,000. Marigold paid the automobile dealer $14,000 cash on the transaction. The entry was a debit to Vehicles and a credit to Cash, $14,000. Jan.1,2021 Truck no. 1 was sold for $3,500 cash. The entry was a debit to Cash and a credit to Vehicles, $3,500. July 1,2022 A new truck (no. 6) was acquired for $40,000 cash and was charged at that amount to the Vehicles account. (Assume truck no. 2 was not retired.) July 1,2022 Truck no. 4 was so badly damaged in an accident that it was sold as scrap for $500 cash. Marigold received $2,400 from the insurance company. The entry made by the bookkeeper was a debit to Cash, $2,900; and credits to Gain on Disposal of Vehicles, $500; and Vehicles, $2,400. Entries for depreciation were made at the close of each year as follows: 2020, $20,400; 2021, $21,400; 2022, $24,250; and 2023, $27,500. (a) For each of the four years, calculate separately the increase or decrease in net income that is due to the company's errors in determining or entering depreciation or in recording transactions affecting the trucks. Ignore income tax considerations. Per Company Books As Adjusted Accumulated Accumulated Depreciation - Retained Depreciation - Retained Net Vehicles Vehicles Earnings Vehicles Vehicles Earnings Ove Dr. (Cr.) Dr. (Cr.) Dr. (Cr.) Dr. (Cr.) Dr. (Cr.) Dr. (Cr.) (Unde 1/1/20 Balance $ $ $ $ $ $ $ 7/1/20 Purchase Truck #5 Trade Truck #3 12/31/20 Depreciation 12/31/20 Balances 1/1/21 Sale of Truck #1 12/31/21 Depreciation 12/31/21 Balances 7/1/22 Purchase of Truck #6 7/1/22 Disposal of Truck #4 12/31/22 Depreciation12/31/21 12/31/21 12/31/22 12/31/22 12/31/23 12/31/23 Depreciation Balances Purchase of Truck #6 Disposal of Truck #4 Depreciation Balances Depreciation Balances Total understatement of income

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts