Question: Assignment Question On 1 July 2018, Mallee Ltd acquired all of the issued shares (cum div.) of Fowl Ltd. At this date, the equity of

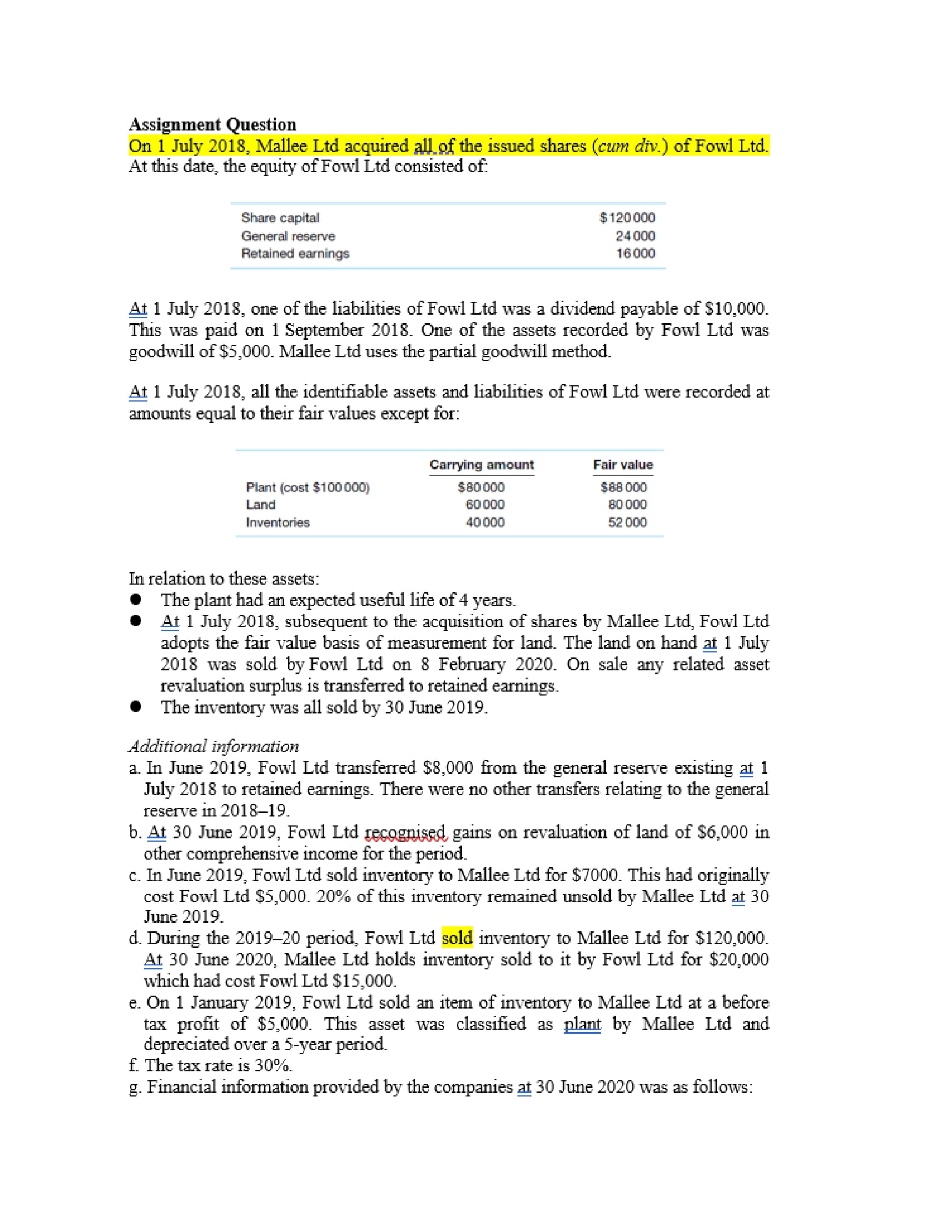

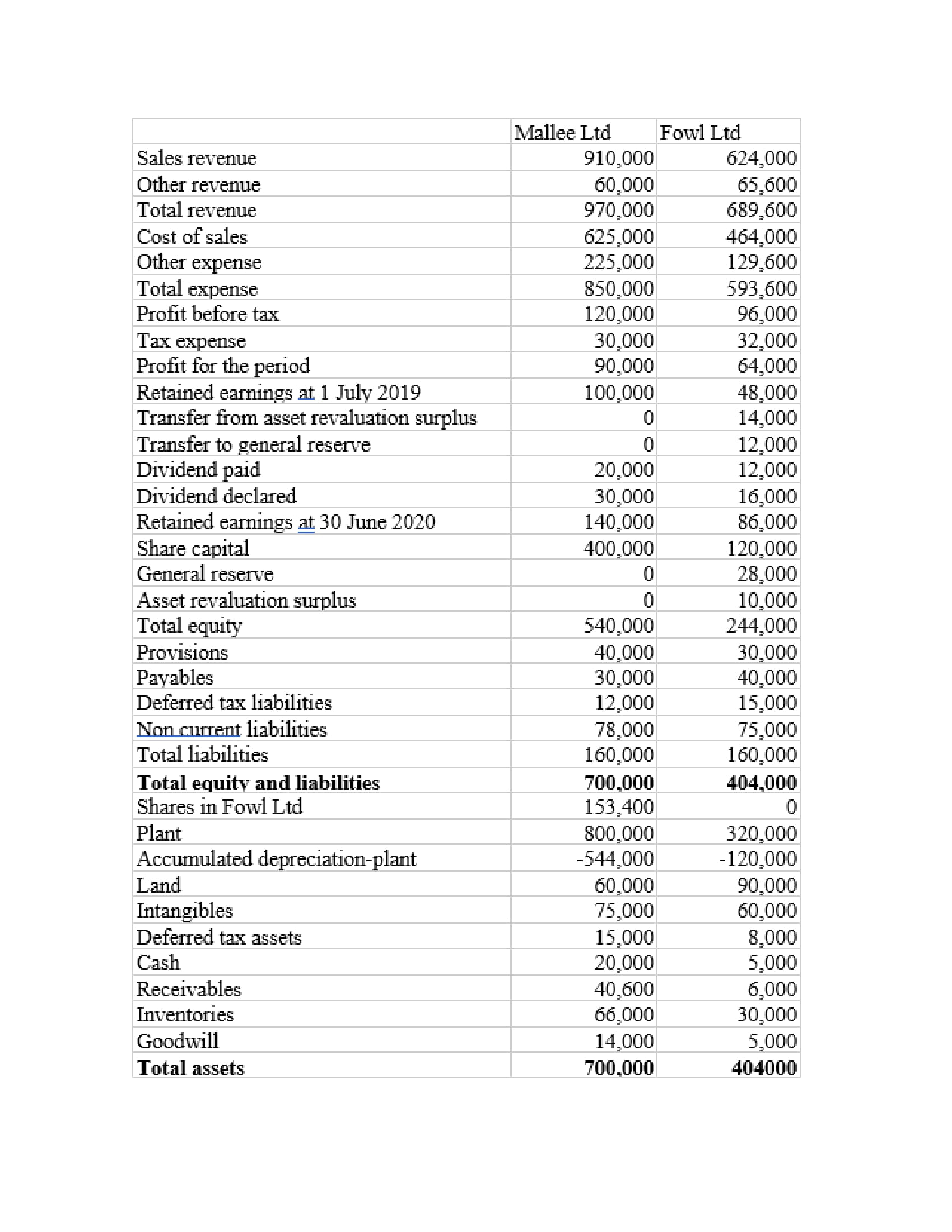

Assignment Question On 1 July 2018, Mallee Ltd acquired all of the issued shares (cum div.) of Fowl Ltd. At this date, the equity of Fowl Ltd consisted of: At 1 July 2018, one of the liabilities of Fowl Ltd was a dividend payable of $10,000. This was paid on 1 September 2018. One of the assets recorded by Fowl Ltd was goodwill of $5,000. Mallee Ltd uses the partial goodwill method. At 1 July 2018, all the identifiable assets and liabilities of Fowl Ltd were recorded at amounts equal to their fair values except for: In relation to these assets: - The plant had an expected useful life of 4 years. - At 1 July 2018, subsequent to the acquisition of shares by Mallee Ltd, Fowl Ltd adopts the fair value basis of measurement for land. The land on hand at 1 July 2018 was sold by Fowl Ltd on 8 February 2020 . On sale any related asset revaluation surplus is transferred to retained earnings. - The inventory was all sold by 30 June 2019. Additional information a. In June 2019 , Fowl Ltd transferred $8,000 from the general reserve existing at 1 July 2018 to retained earnings. There were no other transfers relating to the general reserve in 2018-19. b. At 30 June 2019, Fowl Ltd recognised gains on revaluation of land of $6,000 in other comprehensive income for the period. c. In June 2019, Fowl Ltd sold inventory to Mallee Ltd for $7000. This had originally cost Fowl Ltd $5,000.20% of this inventory remained unsold by Mallee Ltd at 30 June 2019 . d. During the 2019-20 period, Fowl Ltd sold inventory to Mallee Ltd for $120,000. At 30 June 2020, Mallee Ltd holds inventory sold to it by Fowl Ltd for $20,000 which had cost Fowl Ltd $15,000. e. On 1 January 2019, Fowl Ltd sold an item of inventory to Mallee Ltd at a before tax profit of $5,000. This asset was classified as plant by Mallee Ltd and depreciated over a 5 -year period. f. The tax rate is 30%. g. Financial information provided by the companies at 30 June 2020 was as follows: \begin{tabular}{|l|r|r|} \hline & Mallee Ltd & Fowl Ltd \\ \hline Sales revenue & 910,000 & 624,000 \\ \hline Other revenue & 60,000 & 65,600 \\ \hline Total revenue & 970,000 & 689,600 \\ \hline Cost of sales & 625,000 & 464,000 \\ \hline Other expense & 225,000 & 129,600 \\ \hline Total expense & 850,000 & 593,600 \\ \hline Profit before tax & 120,000 & 96,000 \\ \hline Tax expense & 30,000 & 32,000 \\ \hline Profit for the period & 90,000 & 64,000 \\ \hline Retained earnings at 1 July 2019 & 100,000 & 48,000 \\ \hline Transfer from asset revaluation surplus & 0 & 14,000 \\ \hline Transfer to general reserve & 0 & 12,000 \\ \hline Dividend paid & 20,000 & 12,000 \\ \hline Dividend declared & 30,000 & 16,000 \\ \hline Retained earnings at 30 June 2020 & 140,000 & 86,000 \\ \hline Share capital & 400,000 & 120,000 \\ \hline General reserve & 0 & 28,000 \\ \hline Asset revaluation surplus & 0 & 10,000 \\ \hline Total equity & 540,000 & 244,000 \\ \hline Provisions & 40,000 & 30,000 \\ \hline Payables & 30,000 & 40,000 \\ \hline Deferred tax liabilities & 12,000 & 15,000 \\ \hline Non current liabilities & 78,000 & 75,000 \\ \hline Total liabilities & 160,000 & 160,000 \\ \hline Total equity and liabilities & 700,000 & 404,000 \\ \hline Shares in Fowl Ltd & 153,400 & \\ \hline Plant & 800,000 & 320,000 \\ \hline Accumulated depreciation-plant & 544,000 & 120,000 \\ \hline Land & 60,000 & 90,000 \\ \hline Intangibles & 75,000 & 60,000 \\ \hline Deferred tax assets & 15,000 & 8,000 \\ \hline Cash & 20,000 & 5,000 \\ \hline Receivables & 40,600 & 6,000 \\ \hline Inventories & 66,000 & 30,000 \\ \hline Goodwill & 14,000 & 5,000 \\ \hline Total assets & 700,000 & 404000 \\ \hline & & 0 \\ \hline \end{tabular} Required: 1. Prepare the Consolidation Worksheet Journal Entries for the preparation of consolidated financial statements by Mallee Ltd at 30 June 2020. Step 1: Acquisition analysis Step 2: Business combination valuation entries Step 3: Pre-acquisition entries Step 4: Intragroup transactions Note: Students are required to put referenceumber to each journal entry Narrations for entries are required. Abbreviations are not allowed. Show ALL workings. 2. Prepare the Consolidated Worksheet for Mallee Ltd at 30 June 2020. 3. Prepare the Consolidated Statement of Financial Position for Mallee Ltd at 30 June 2020 in accordance with IAS 1/AASB 101 Presentation of Financial Statements. The format of the statement must use total asset approach. 4. Prepare a Consolidated Statement of Comprehensive Income for Mallee Ltd for the year ended 30 June 2020. The format of the statement must be function of expense method (IAS1/AASB101 para 103). Assignment Question On 1 July 2018, Mallee Ltd acquired all of the issued shares (cum div.) of Fowl Ltd. At this date, the equity of Fowl Ltd consisted of: At 1 July 2018, one of the liabilities of Fowl Ltd was a dividend payable of $10,000. This was paid on 1 September 2018. One of the assets recorded by Fowl Ltd was goodwill of $5,000. Mallee Ltd uses the partial goodwill method. At 1 July 2018, all the identifiable assets and liabilities of Fowl Ltd were recorded at amounts equal to their fair values except for: In relation to these assets: - The plant had an expected useful life of 4 years. - At 1 July 2018, subsequent to the acquisition of shares by Mallee Ltd, Fowl Ltd adopts the fair value basis of measurement for land. The land on hand at 1 July 2018 was sold by Fowl Ltd on 8 February 2020 . On sale any related asset revaluation surplus is transferred to retained earnings. - The inventory was all sold by 30 June 2019. Additional information a. In June 2019 , Fowl Ltd transferred $8,000 from the general reserve existing at 1 July 2018 to retained earnings. There were no other transfers relating to the general reserve in 2018-19. b. At 30 June 2019, Fowl Ltd recognised gains on revaluation of land of $6,000 in other comprehensive income for the period. c. In June 2019, Fowl Ltd sold inventory to Mallee Ltd for $7000. This had originally cost Fowl Ltd $5,000.20% of this inventory remained unsold by Mallee Ltd at 30 June 2019 . d. During the 2019-20 period, Fowl Ltd sold inventory to Mallee Ltd for $120,000. At 30 June 2020, Mallee Ltd holds inventory sold to it by Fowl Ltd for $20,000 which had cost Fowl Ltd $15,000. e. On 1 January 2019, Fowl Ltd sold an item of inventory to Mallee Ltd at a before tax profit of $5,000. This asset was classified as plant by Mallee Ltd and depreciated over a 5 -year period. f. The tax rate is 30%. g. Financial information provided by the companies at 30 June 2020 was as follows: \begin{tabular}{|l|r|r|} \hline & Mallee Ltd & Fowl Ltd \\ \hline Sales revenue & 910,000 & 624,000 \\ \hline Other revenue & 60,000 & 65,600 \\ \hline Total revenue & 970,000 & 689,600 \\ \hline Cost of sales & 625,000 & 464,000 \\ \hline Other expense & 225,000 & 129,600 \\ \hline Total expense & 850,000 & 593,600 \\ \hline Profit before tax & 120,000 & 96,000 \\ \hline Tax expense & 30,000 & 32,000 \\ \hline Profit for the period & 90,000 & 64,000 \\ \hline Retained earnings at 1 July 2019 & 100,000 & 48,000 \\ \hline Transfer from asset revaluation surplus & 0 & 14,000 \\ \hline Transfer to general reserve & 0 & 12,000 \\ \hline Dividend paid & 20,000 & 12,000 \\ \hline Dividend declared & 30,000 & 16,000 \\ \hline Retained earnings at 30 June 2020 & 140,000 & 86,000 \\ \hline Share capital & 400,000 & 120,000 \\ \hline General reserve & 0 & 28,000 \\ \hline Asset revaluation surplus & 0 & 10,000 \\ \hline Total equity & 540,000 & 244,000 \\ \hline Provisions & 40,000 & 30,000 \\ \hline Payables & 30,000 & 40,000 \\ \hline Deferred tax liabilities & 12,000 & 15,000 \\ \hline Non current liabilities & 78,000 & 75,000 \\ \hline Total liabilities & 160,000 & 160,000 \\ \hline Total equity and liabilities & 700,000 & 404,000 \\ \hline Shares in Fowl Ltd & 153,400 & \\ \hline Plant & 800,000 & 320,000 \\ \hline Accumulated depreciation-plant & 544,000 & 120,000 \\ \hline Land & 60,000 & 90,000 \\ \hline Intangibles & 75,000 & 60,000 \\ \hline Deferred tax assets & 15,000 & 8,000 \\ \hline Cash & 20,000 & 5,000 \\ \hline Receivables & 40,600 & 6,000 \\ \hline Inventories & 66,000 & 30,000 \\ \hline Goodwill & 14,000 & 5,000 \\ \hline Total assets & 700,000 & 404000 \\ \hline & & 0 \\ \hline \end{tabular} Required: 1. Prepare the Consolidation Worksheet Journal Entries for the preparation of consolidated financial statements by Mallee Ltd at 30 June 2020. Step 1: Acquisition analysis Step 2: Business combination valuation entries Step 3: Pre-acquisition entries Step 4: Intragroup transactions Note: Students are required to put referenceumber to each journal entry Narrations for entries are required. Abbreviations are not allowed. Show ALL workings. 2. Prepare the Consolidated Worksheet for Mallee Ltd at 30 June 2020. 3. Prepare the Consolidated Statement of Financial Position for Mallee Ltd at 30 June 2020 in accordance with IAS 1/AASB 101 Presentation of Financial Statements. The format of the statement must use total asset approach. 4. Prepare a Consolidated Statement of Comprehensive Income for Mallee Ltd for the year ended 30 June 2020. The format of the statement must be function of expense method (IAS1/AASB101 para 103)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts