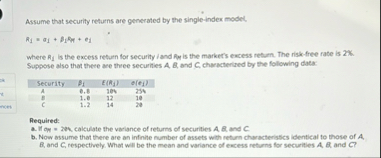

Question: Assume that security returns are generated by the single - index model, 1 = a i t 1 t N i where R i is

Assume that security returns are generated by the singleindex model,

where is the excess retum for security iand is the markets excess return. The riskfree rate is Suppose also that there ace three securities A B and C charnctienised by the following data:

tableSecurity

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock