Assume that the ABC company provides educational services to a Vietnamese university and expects to receive VND

Question:

Assume that the ABC company provides educational services to a Vietnamese university and expects to receive VND 850 million in three months.

The existing spot rates are USD/TWD of 31.65-31.87 and USD/VND of 24,275.00-25,128.00, respectively.

The three-month interest rates of TWD are 1.25%-2.75% while the three-month interest rates of VND are 3.5%-5.25%.

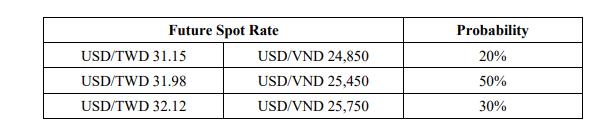

A three-month put option for VND 1,000,000 with a strike price of USD/VND 25,250.00 has an option premium of 5%. The possibilities of exchange rates are summarized in the following table:

(Naïve hedge is used here and it means that the number of hedge contracts are determined using total exposure amount divided by the unit hedge contract size.)

Questions:

(a) What is the TWD cost of using puts to perform the receivable hedge by the naïve option hedge method? (Hint: the interest cost of using puts is the TWD interest rates)

(b) What is the expected TWD cash flow for the hedge portfolio using puts to perform the receivable hedge if the realized USD/VND is 25,200 in three months by the naïve option hedge method?

Expert Answer:

To calculate the TWD cost of using puts to perform the receivable hedge and the expected TWD cash flow for the hedge portfolio we need to follow these ... View the full answer