Assume that the CAPM holds. Consider a stock market that consists of only two risky securities, Stock

Question:

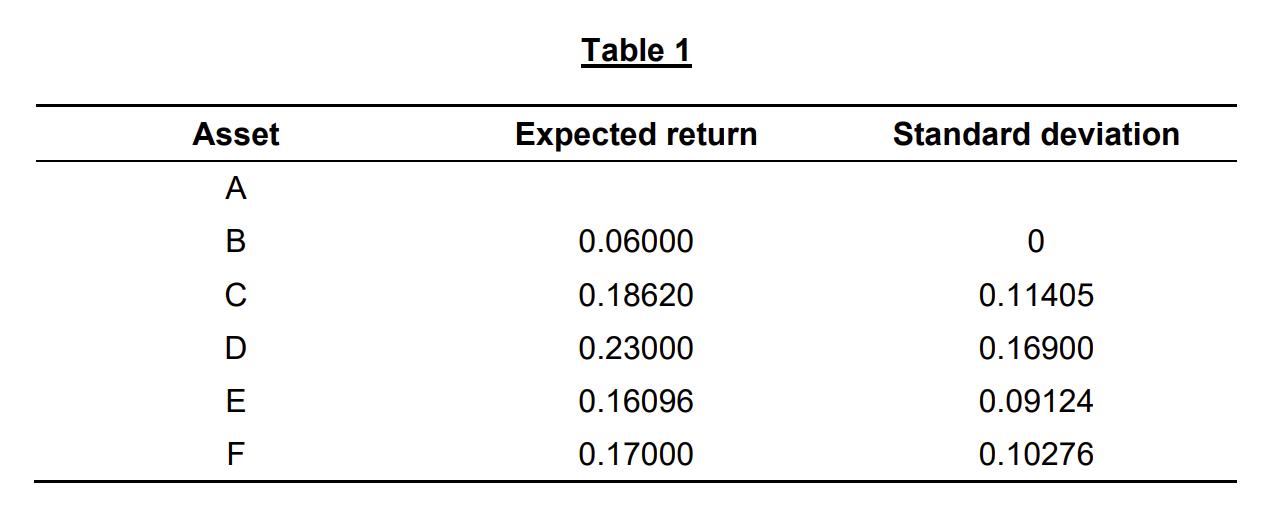

Assume that the CAPM holds. Consider a stock market that consists of only two risky securities, Stock 1 and Stock 2, with the following expected returns (µ) and standard deviations of returns (σ): µ1 = 0.25, σ1 = 0.20; µ2 = 0.15, σ2 = 0.10. Table 1 shows the expected returns and standard deviations for six assets, A to F (the entries for asset A are left intentionally blank). These assets are portfolios consisting of the risk-free asset, Stock 1, and Stock 2 in varying quantities (which may be positive, negative, or zero).

Given that Asset D has a zero investment in the risk-free asset and has a 0.8 weight in stock 1 and 0.2 weight in stock 2.

Given that Asset D has a zero investment in the risk-free asset and has a 0.8 weight in stock 1 and 0.2 weight in stock 2.

Given that the correlation between the returns of Stock 1 and Stock 2 is 0.40016 and the expected returns on asset A is 0.15588 and the standard deviation of asset A is 0.099410.

Answer part (e) as below:

Expert Answer:

Financial Decisions And Markets A Course In Asset Pricing

ISBN: 9780691160801

1st Edition

Authors: John Y. Campbell