Question: Assume that the car industry is characterized by monopolistic competition and consequently the equilibrium in the long run is achieved when the average cost

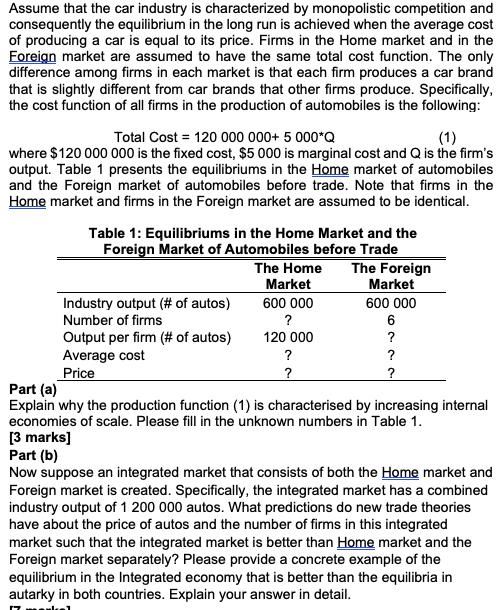

Assume that the car industry is characterized by monopolistic competition and consequently the equilibrium in the long run is achieved when the average cost of producing a car is equal to its price. Firms in the Home market and in the Foreign market are assumed to have the same total cost function. The only difference among firms in each market is that each firm produces a car brand that is slightly different from car brands that other firms produce. Specifically, the cost function of all firms in the production of automobiles is the following: Total Cost = 120 000 000+ 5 000*Q where $120 000 000 is the fixed cost, $5 000 is marginal cost and Q is the firm's output. Table 1 presents the equilibriums in the Home market of automobiles and the Foreign market of automobiles before trade. Note that firms in the Home market and firms in the Foreign market are assumed to be identical. (1) Table 1: Equilibriums in the Home Market and the Foreign Market of Automobiles before Trade The Foreign Market The Home Market Industry output (# of autos) 600 000 600 000 Number of firms ? 6 Output per firm (# of autos) Average cost Price 120 000 ? ? ? Part (a) Explain why the production function (1) is characterised by increasing internal economies of scale. Please fill in the unknown numbers in Table 1. [3 marks] Part (b) Now suppose an integrated market that consists of both the Home market and Foreign market is created. Specifically, the integrated market has a combined industry output of 1 200 000 autos. What predictions do new trade theories have about the price of autos and the number of firms in this integrated market such that the integrated market is better than Home market and the Foreign market separately? Please provide a concrete example of the equilibrium in the Integrated economy that is better than the equilibria in autarky in both countries. Explain your answer in detail.

Step by Step Solution

There are 3 Steps involved in it

a Increasing internal economies of scale occur when a firms cost per unit of output ie its average c... View full answer

Get step-by-step solutions from verified subject matter experts