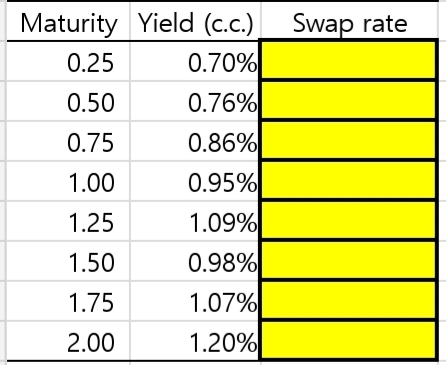

Question: Assume that the continuously compounded yield curve is given below. Calculate the quarterly swap rate for all maturities between 3 months and 2 years (every

Assume that the continuously compounded yield curve is given below.

Calculate the quarterly swap rate for all maturities between 3 months and 2 years (every three months).

Maturity Yield (c.c.) Swap rate 0.25 0.70% 0.50 0.76% 0.75 0.86% 1.00 0.95% 1.25 1.09% 1.50 0.98% 1.75 1.07% 2.00 1.20%

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock