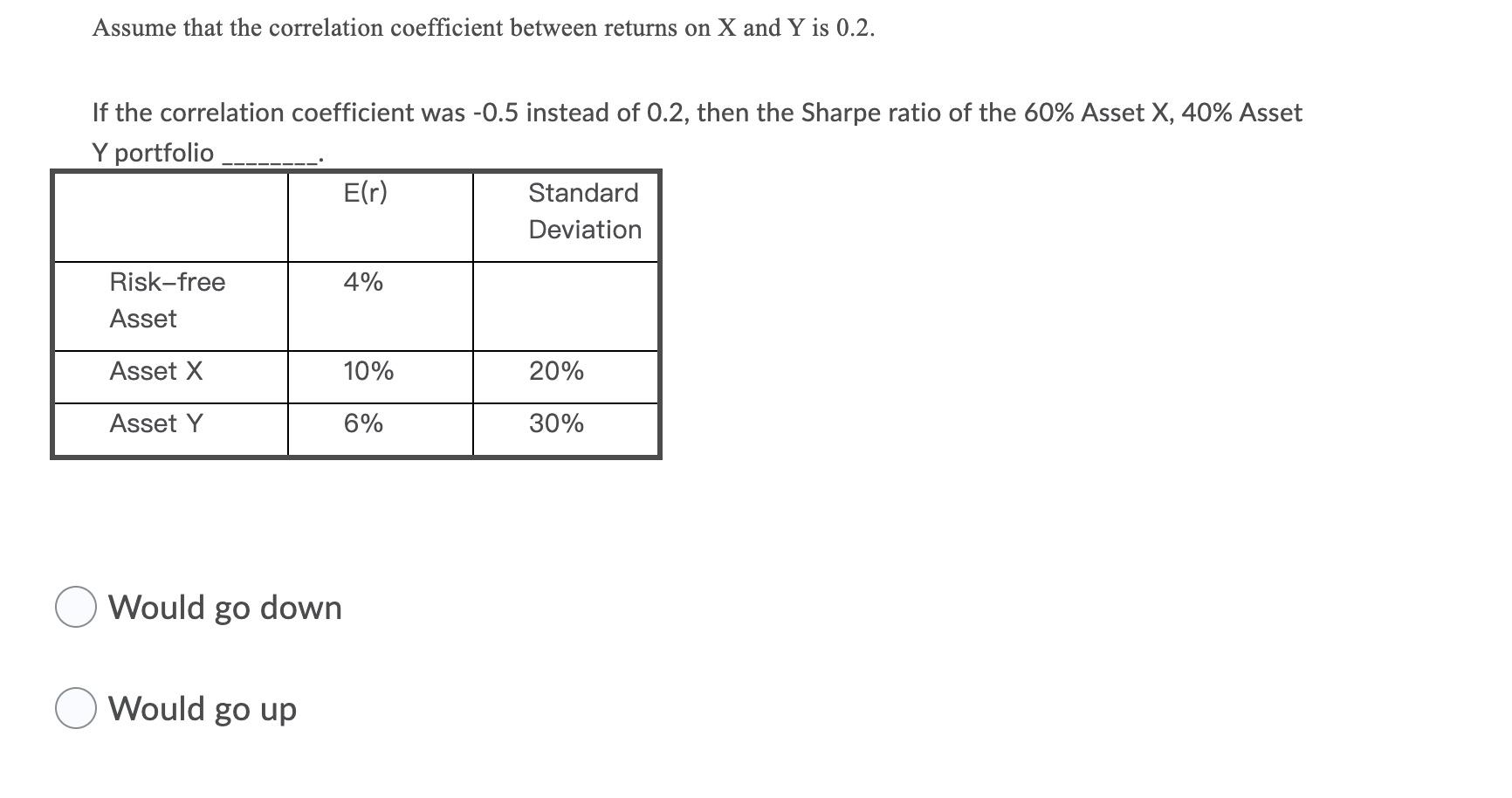

Question: Assume that the correlation coefficient between returns on X and Y is 0.2. If the correlation coefficient was -0.5 instead of 0.2, then the Sharpe

Assume that the correlation coefficient between returns on X and Y is 0.2. If the correlation coefficient was -0.5 instead of 0.2, then the Sharpe ratio of the 60% Asset X, 40% Asset Y portfolio E(r) Standard Deviation 4% Risk-free Asset Asset x 10% 20% Asset Y 6% 30% Would go down Would go up

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock