Assume that the following market model adequately describes the return-generating behavior of risky assets: Rit a+BiRMt+...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

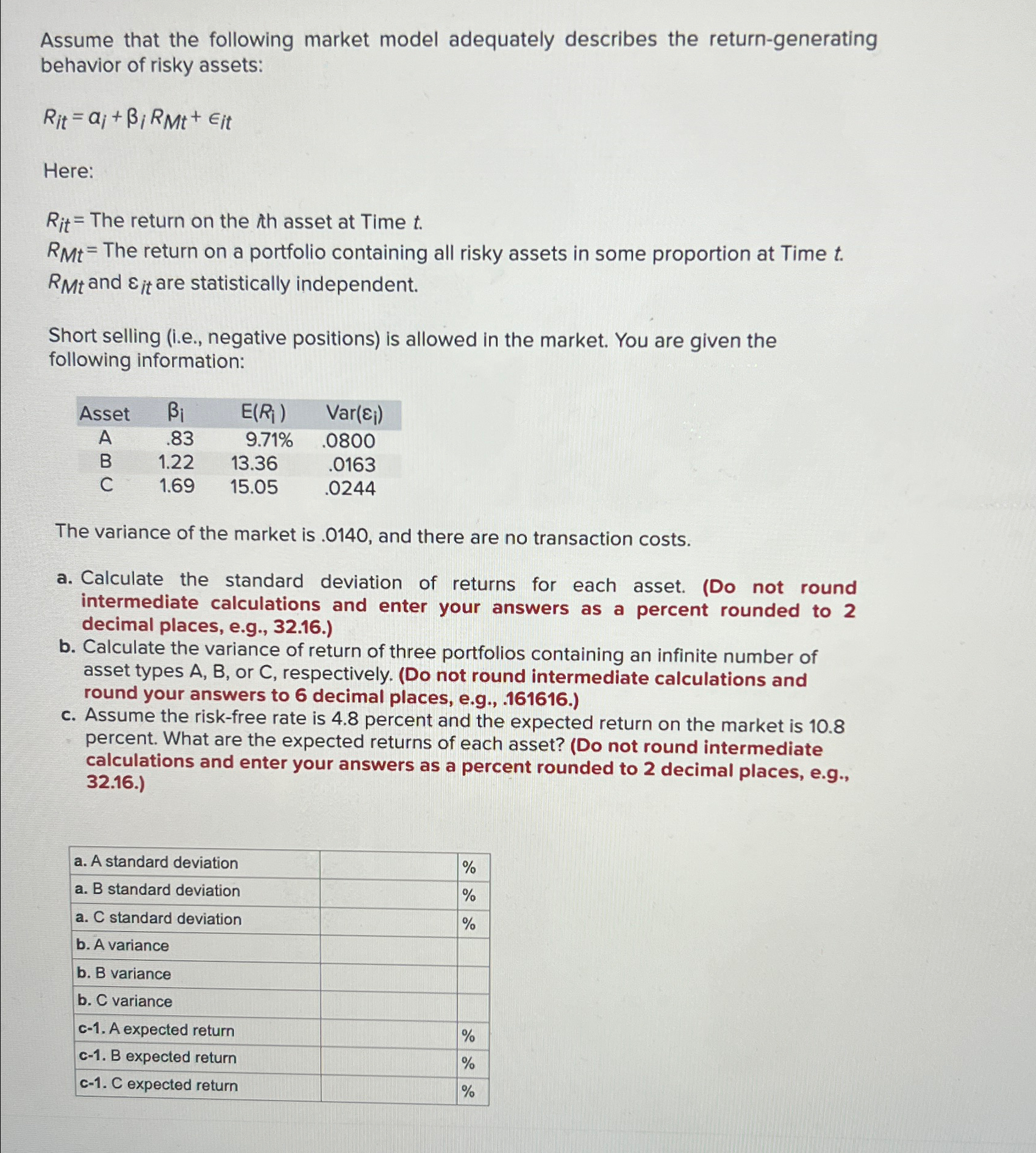

Assume that the following market model adequately describes the return-generating behavior of risky assets: Rit a+BiRMt+ Eit Here: Rit=The return on the ith asset at Time t. RMt=The return on a portfolio containing all risky assets in some proportion at Time t. RMt and & it are statistically independent. Short selling (i.e., negative positions) is allowed in the market. You are given the following information: Asset Bi E(R) Var(i) A .83 9.71% .0800 B 1.22 13.36 .0163 C 1.69 15.05 .0244 The variance of the market is .0140, and there are no transaction costs. a. Calculate the standard deviation of returns for each asset. (Do not round intermediate calculations and enter your answers as a percent rounded to 2 decimal places, e.g., 32.16.) b. Calculate the variance of return of three portfolios containing an infinite number of asset types A, B, or C, respectively. (Do not round intermediate calculations and round your answers to 6 decimal places, e.g., .161616.) c. Assume the risk-free rate is 4.8 percent and the expected return on the market is 10.8 percent. What are the expected returns of each asset? (Do not round intermediate calculations and enter your answers as a percent rounded to 2 decimal places, e.g., 32.16.) a. A standard deviation % a. B standard deviation % a. C standard deviation % b. A variance b. B variance b. C variance c-1. A expected return c-1. B expected return % c-1. C expected return % Assume that the following market model adequately describes the return-generating behavior of risky assets: Rit a+BiRMt+ Eit Here: Rit=The return on the ith asset at Time t. RMt=The return on a portfolio containing all risky assets in some proportion at Time t. RMt and & it are statistically independent. Short selling (i.e., negative positions) is allowed in the market. You are given the following information: Asset Bi E(R) Var(i) A .83 9.71% .0800 B 1.22 13.36 .0163 C 1.69 15.05 .0244 The variance of the market is .0140, and there are no transaction costs. a. Calculate the standard deviation of returns for each asset. (Do not round intermediate calculations and enter your answers as a percent rounded to 2 decimal places, e.g., 32.16.) b. Calculate the variance of return of three portfolios containing an infinite number of asset types A, B, or C, respectively. (Do not round intermediate calculations and round your answers to 6 decimal places, e.g., .161616.) c. Assume the risk-free rate is 4.8 percent and the expected return on the market is 10.8 percent. What are the expected returns of each asset? (Do not round intermediate calculations and enter your answers as a percent rounded to 2 decimal places, e.g., 32.16.) a. A standard deviation % a. B standard deviation % a. C standard deviation % b. A variance b. B variance b. C variance c-1. A expected return c-1. B expected return % c-1. C expected return %

Expert Answer:

Posted Date:

Students also viewed these finance questions

-

Why is an investment portfolio containing a mix of stocks and bonds less risky than one containing a single asset class? Because the markets for stocks and bonds tend to move in the same direction at...

-

A parallel-plate capacitor with circular plates of radius R = 16 mm and gap width d = 5.0 mm has a uniform electric field between the plates. Starting at time t = 0, the potential difference between...

-

How much total interest was paid for the 20 -year loan? The 30 -year loan? Calculate the difference. Below are two amortization tables. They are for loans with the same principal and interest rate,...

-

Vertices \(a\) and \(e\). Recall the three common scenarios in which it is not possible to have a Hamilton between two vertices. Scenario 1: If an edge \(a b\) is a bridge, then there is no Hamilton...

-

Three different companies each purchased a machine on January 1, 2008, for $42,000. Each machine was expected to last five years or 200,000 hours. Salvage value was estimated to be $2,000. All three...

-

Which of the following events would REDUCE the WACC? 1. The market risk premium declines 2. The floataion costs associated with issuing new common stock increases 3. The companys beta increases. 4....

-

1. Explain about Service Detection in Network devices 2. Explain about Network Vulnerability in Network devices 3. Explain about Wireless foot printing 4. Explain about wireless scanning and...

-

Identify two types of reports that may be issued on the internal control structure over the processing of transactions by service organizations and indicate by whom and for what purposes the reports...

-

What is the best way to classify robots? Why?

-

What is the most important business value of robots?

-

a. What conditions must be met for an independent accountant to perform an examination of a management assertion about the effectiveness of an entity's internal control structure? b. Briefly describe...

-

a. What limited procedures are common to both types of reviews? b. What additional procedures are required in SAS 71 reviews?

-

A variable is normally distributed with mean 10 and standard deviation 2. obtain the 85th percentile

-

What types of questions can be answered by analyzing financial statements?

-

Comprehensive Problem: Reviewing the Accounting Cycle} Fodor Freight Service provides delivery of merchandise to retail grocery stores in northern Manitoba. At the beginning of 2018 , the following...

-

Cash-Basis and Accrual-Basis Income} Martin Sharp, who repairs lawn mowers, collects cash from his customers when the repair services are completed. He maintains an inventory of repair parts that are...

-

Preparation of Adjusting Entries} Osaga Beach Resort operates a resort complex that specializes in hosting small business and professional meetings. Osaga Beach closes its fiscal year on January 31,...

Study smarter with the SolutionInn App