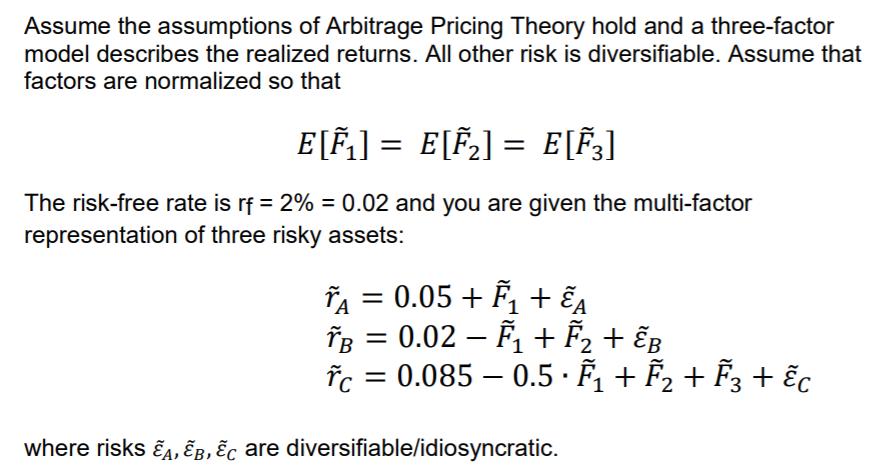

Assume the assumptions of Arbitrage Pricing Theory hold and a three-factor model describes the realized returns....

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

a Ass ume the 3 factor Arbit rage Pricing Theory applies What are the risk prem ia for holding factors 1 2 3 ANS WER The risk prem ia for holding fact... View the full answer

Related Book For

Posted Date: