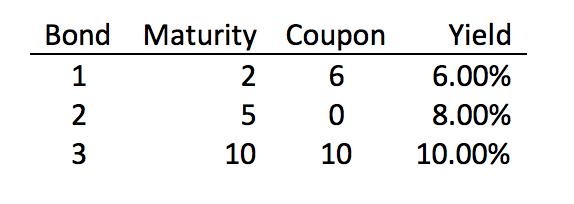

Assume the following three bonds a.) Calculate price, modified duration, and convexity for these three bonds. b.)

Question:

Assume the following three bonds

a.) Calculate price, modified duration, and convexity for these three bonds.

b.) Now, suppose you have $1,000,000 worth of the 5-year bond. You want to carry out a butterfly spread, that is to sell the 5-year bond and buy the 2-year and 10- year bonds such that the value of your final portfolio is the same as the sale proceeds, that is 1,000,000, and the modified duration of the final portfolio is equal to the modified duration of the 5-year bond. Rounding off to the nearest $1000, calculate the dollar value of the 2-year and the 10-year bonds you buy.

c.) Does your portfolio or the initial 5-year bond have greater convexity?

d.) What is the rationale of the butterfly spread?

Expert Answer:

a Bond 1 2Y Price 10001062 94057 Duration 2106 188 years Convexity 21062 375 Bond 2 5Y ... View the full answer

Probability And Statistics For Engineering And The Sciences

ISBN: 9781305251809

9th Edition

Authors: Jay L. Devore