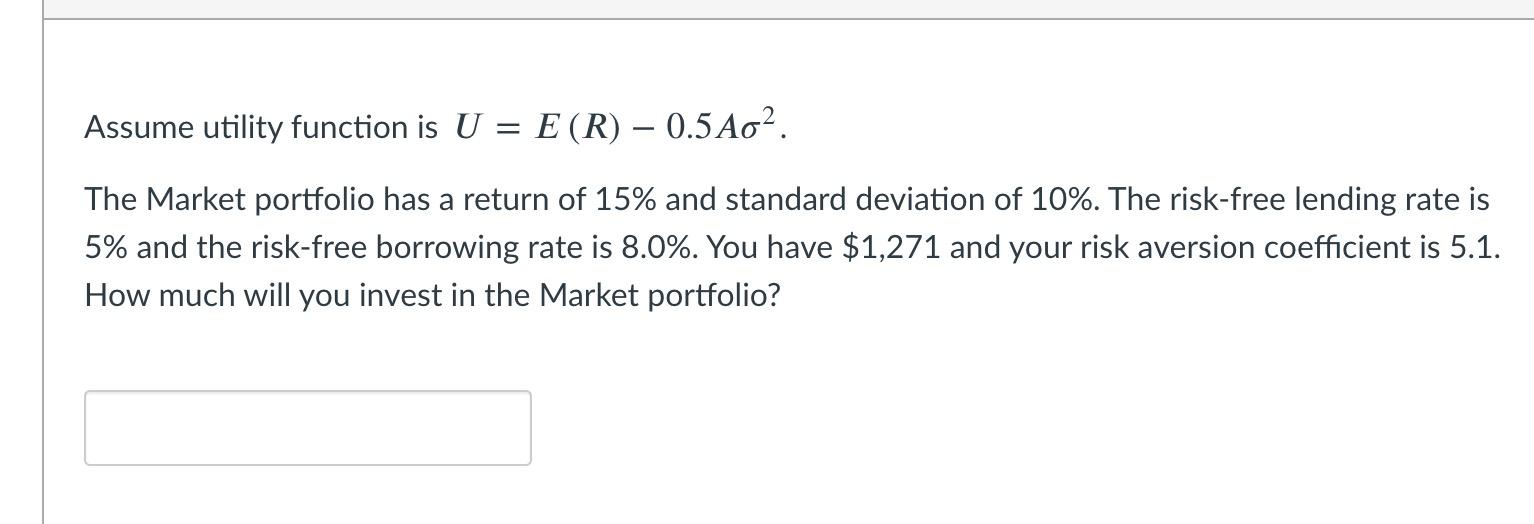

Question: Assume utility function is U = E(R) 0.5 Ag2. The Market portfolio has a return of 15% and standard deviation of 10%. The risk-free lending

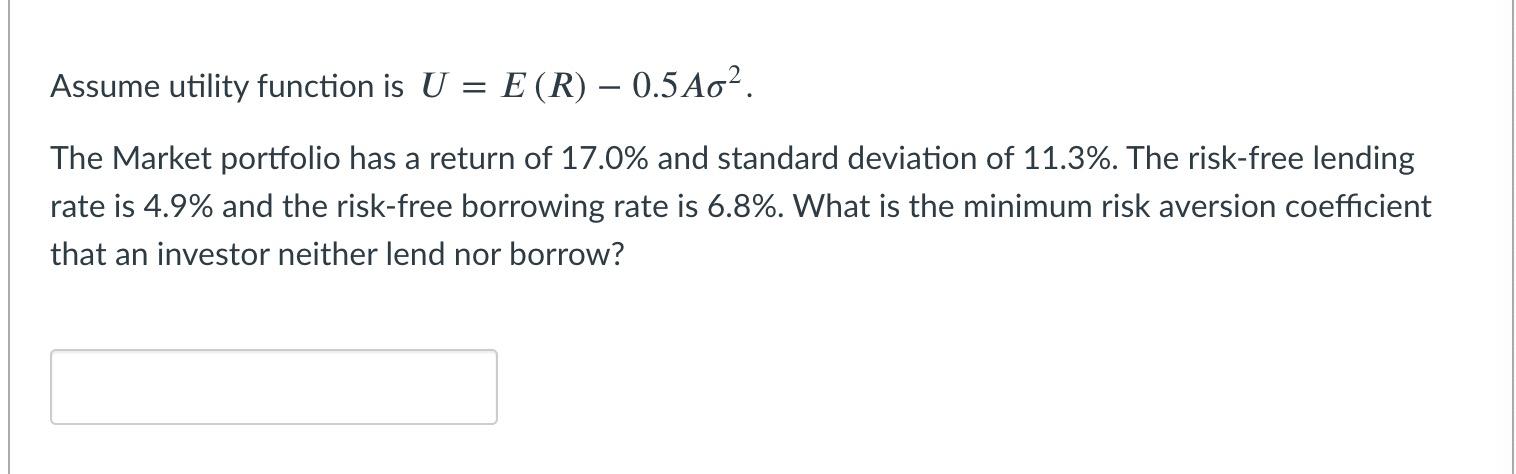

Assume utility function is U = E(R) 0.5 Ag2. The Market portfolio has a return of 15% and standard deviation of 10%. The risk-free lending rate is 5% and the risk-free borrowing rate is 8.0%. You have $1,271 and your risk aversion coefficient is 5.1. How much will you invest in the Market portfolio? Assume utility function is U = E(R) 0.5 A02. The Market portfolio has a return of 17.0% and standard deviation of 11.3%. The risk-free lending rate is 4.9% and the risk-free borrowing rate is 6.8%. What is the minimum risk aversion coefficient that an investor neither lend nor borrow

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock