Assume you are the chief financial officer of T-Shirt Pros, a small business that makes custom-printed T-shirts.

Question:

Assume you are the chief financial officer of T-Shirt Pros, a small business that makes custom-printed T-shirts. While reviewing the financial statements that were prepared by company accountants, you discover an error. During this period, the company had purchased a warehouse building, in exchange for a $200,000 note payable. The company’s policy is to report noncash investing and financing activities in a separate statement, after the presentation of the statement of cash flows. This noncash investing and financing transaction was inadvertently included in both the financing section as a source of cash, and the investing section as a use of cash.

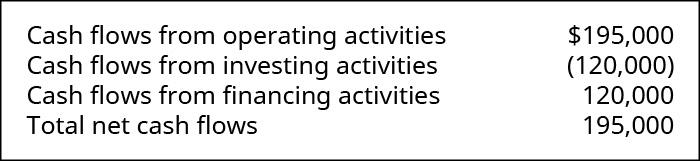

T-Shirt Pros’ statement of cash flows, as it was prepared by the company accountants, reported the following for the period, and had no other capital expenditures.

Because of the misplacement of the transaction, the calculation of free cash flow by outside analysts could be affected significantly. Free cash flow is calculated as cash flow from operating activities, reduced by capital expenditures, the value for which is normally obtained from the investing section of the statement of cash flows. As their manager, would you treat the accountants’ error as a harmless misclassification, or as a major blunder on their part? Explain.

Expert Answer:

Introduction As the Chief Financial Officer CFO of TShirt Pros my role involves overseeing financial reporting and ensuring accuracy in financial stat... View the full answer

Intermediate Accounting

ISBN: 978-0324592375

17th Edition

Authors: James D. Stice, Earl K. Stice, Fred Skousen