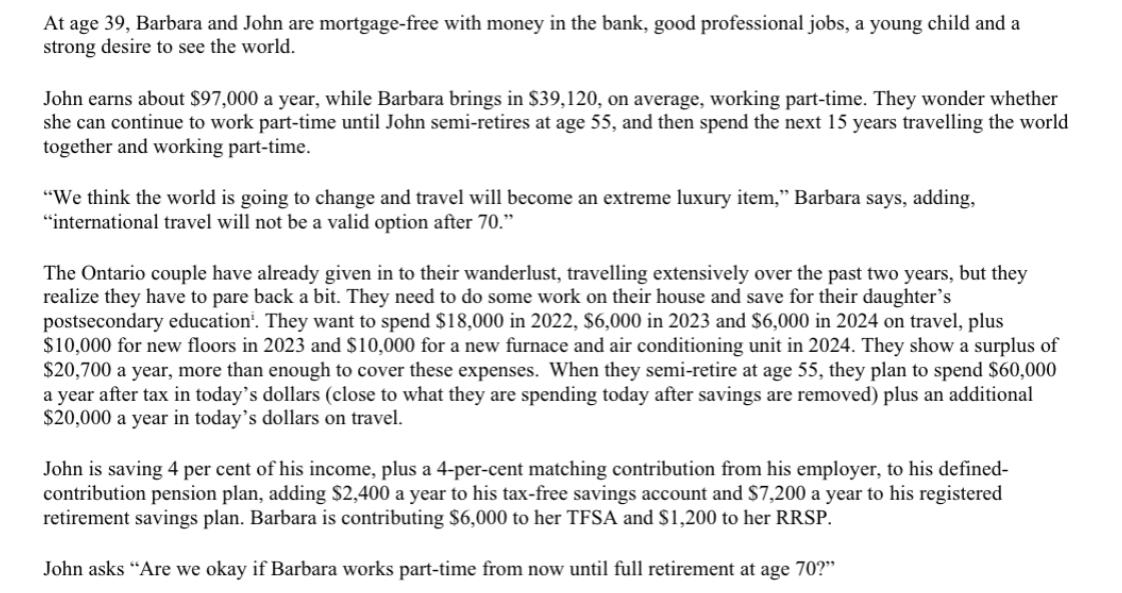

At age 39, Barbara and John are mortgage-free with money in the bank, good professional jobs,...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

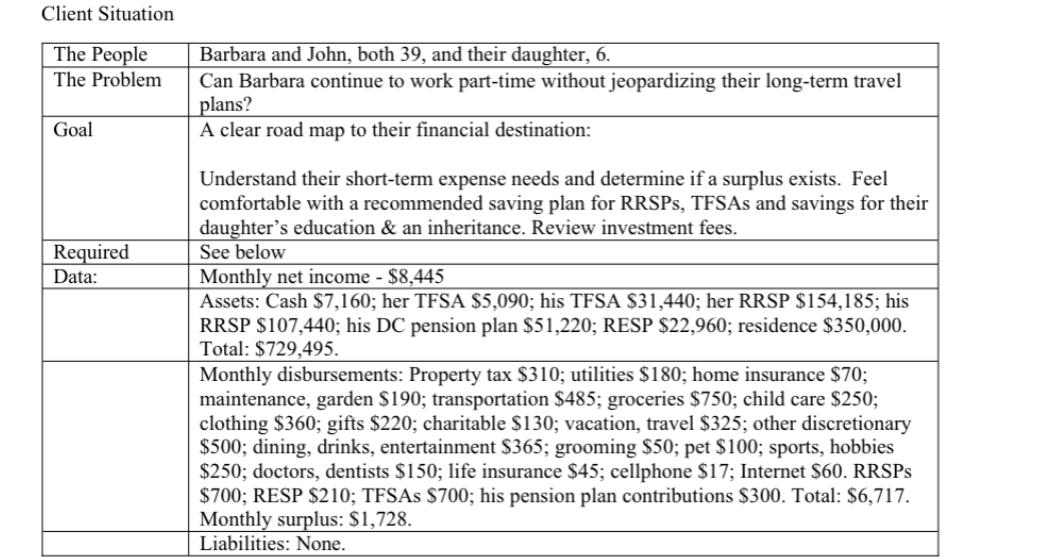

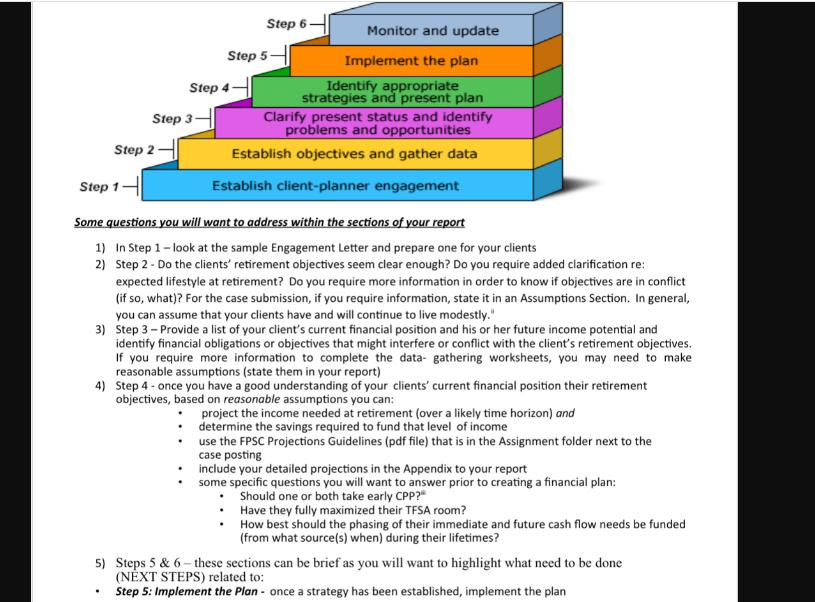

At age 39, Barbara and John are mortgage-free with money in the bank, good professional jobs, a young child and a strong desire to see the world. John earns about $97,000 a year, while Barbara brings in $39,120, on average, working part-time. They wonder whether she can continue to work part-time until John semi-retires at age 55, and then spend the next 15 years travelling the world together and working part-time. "We think the world is going to change and travel will become an extreme luxury item, Barbara says, adding, international travel will not be a valid option after 70." The Ontario couple have already given in to their wanderlust, travelling extensively over the past two years, but they realize they have to pare back a bit. They need to do some work on their house and save for their daughter's postsecondary education. They want to spend $18,000 in 2022, $6,000 in 2023 and $6,000 in 2024 on travel, plus $10,000 for new floors in 2023 and $10,000 for a new furnace and air conditioning unit in 2024. They show a surplus of $20,700 a year, more than enough to cover these expenses. When they semi-retire at age 55, they plan to spend $60,000 a year after tax in today's dollars (close to what they are spending today after savings are removed) plus an additional $20,000 a year in today's dollars on travel. John is saving 4 per cent of his income, plus a 4-per-cent matching contribution from his employer, to his defined- contribution pension plan, adding $2,400 a year to his tax-free savings account and $7,200 a year to his registered retirement savings plan. Barbara is contributing $6,000 to her TFSA and $1,200 to her RRSP. John asks "Are we okay if Barbara works part-time from now until full retirement at age 70?" Client Situation The People The Problem Goal Required Data: Barbara and John, both 39, and their daughter, 6. Can Barbara continue to work part-time without jeopardizing their long-term travel plans? A clear road map to their financial destination: Understand their short-term expense needs and determine if a surplus exists. Feel comfortable with a recommended saving plan for RRSPs, TFSAs and savings for their daughter's education & an inheritance. Review investment fees. See below Monthly net income - $8,445 Assets: Cash $7,160; her TFSA $5,090; his TFSA $31,440; her RRSP $154,185; his RRSP $107,440; his DC pension plan $51,220; RESP $22,960; residence $350,000. Total: $729,495. Monthly disbursements: Property tax $310; utilities $180; home insurance $70; maintenance, garden $190; transportation $485; groceries $750; child care $250; clothing $360; gifts $220; charitable $130; vacation, travel $325; other discretionary $500; dining, drinks, entertainment $365; grooming $50; pet $100; sports, hobbies $250; doctors, dentists $150; life insurance $45; cellphone $17; Internet $60. RRSPs $700; RESP $210; TFSAs $700; his pension plan contributions $300. Total: $6,717. Monthly surplus: $1,728. Liabilities: None. Required: Individually, prepare a professionally typed financial plan following the CIFP 6-steps. Remember that the financial planning process is meant to provide you with an opportunity to take what they have learned in this Retirement Planning course and demonstrate your financial planning skills. Step 6- Monitor and update Step 5 Implement the plan Step 4- Step 3- Identify appropriate strategies and present plan Clarify present status and identify problems and opportunities Step 2 Establish objectives and gather data Step 1- Establish client-planner engagement Some questions you will want to address within the sections of your report 1) In Step 1-look at the sample Engagement Letter and prepare one for your clients 2) Step 2 - Do the clients' retirement objectives seem clear enough? Do you require added clarification re: expected lifestyle at retirement? Do you require more information in order to know if objectives are in conflict (if so, what)? For the case submission, if you require information, state it in an Assumptions Section. In general, you can assume that your clients have and will continue to live modestly." 3) Step 3 - Provide a list of your client's current financial position and his or her future income potential and identify financial obligations or objectives that might interfere or conflict with the client's retirement objectives. If you require more information to complete the data- gathering worksheets, you may need to make reasonable assumptions (state them in your report) 4) Step 4 - once you have a good understanding of your clients' current financial position their retirement objectives, based on reasonable assumptions you can: project the income needed at retirement (over a likely time horizon) and determine the savings required to fund that level of income use the FPSC Projections Guidelines (pdf file) that is in the Assignment folder next to the case posting include your detailed projections in the Appendix to your report some specific questions you will want to answer prior to creating a financial plan: Should one or both take early CPP?" Have they fully maximized their TFSA room? How best should the phasing of their immediate and future cash flow needs be funded (from what source(s) when) during their lifetimes? 5) Steps 5 & 6-these sections can be brief as you will want to highlight what need to be done (NEXT STEPS) related to: . Step 5: Implement the Plan - once a strategy has been established, implement the plan What specialists, if any, would you want to consult at this stage Step 6: Monitor & Update - how often would you want to conduct periodic reviews and updates to evaluate progress towards your clients' retirement objectives At age 39, Barbara and John are mortgage-free with money in the bank, good professional jobs, a young child and a strong desire to see the world. John earns about $97,000 a year, while Barbara brings in $39,120, on average, working part-time. They wonder whether she can continue to work part-time until John semi-retires at age 55, and then spend the next 15 years travelling the world together and working part-time. "We think the world is going to change and travel will become an extreme luxury item, Barbara says, adding, international travel will not be a valid option after 70." The Ontario couple have already given in to their wanderlust, travelling extensively over the past two years, but they realize they have to pare back a bit. They need to do some work on their house and save for their daughter's postsecondary education. They want to spend $18,000 in 2022, $6,000 in 2023 and $6,000 in 2024 on travel, plus $10,000 for new floors in 2023 and $10,000 for a new furnace and air conditioning unit in 2024. They show a surplus of $20,700 a year, more than enough to cover these expenses. When they semi-retire at age 55, they plan to spend $60,000 a year after tax in today's dollars (close to what they are spending today after savings are removed) plus an additional $20,000 a year in today's dollars on travel. John is saving 4 per cent of his income, plus a 4-per-cent matching contribution from his employer, to his defined- contribution pension plan, adding $2,400 a year to his tax-free savings account and $7,200 a year to his registered retirement savings plan. Barbara is contributing $6,000 to her TFSA and $1,200 to her RRSP. John asks "Are we okay if Barbara works part-time from now until full retirement at age 70?" Client Situation The People The Problem Goal Required Data: Barbara and John, both 39, and their daughter, 6. Can Barbara continue to work part-time without jeopardizing their long-term travel plans? A clear road map to their financial destination: Understand their short-term expense needs and determine if a surplus exists. Feel comfortable with a recommended saving plan for RRSPs, TFSAs and savings for their daughter's education & an inheritance. Review investment fees. See below Monthly net income - $8,445 Assets: Cash $7,160; her TFSA $5,090; his TFSA $31,440; her RRSP $154,185; his RRSP $107,440; his DC pension plan $51,220; RESP $22,960; residence $350,000. Total: $729,495. Monthly disbursements: Property tax $310; utilities $180; home insurance $70; maintenance, garden $190; transportation $485; groceries $750; child care $250; clothing $360; gifts $220; charitable $130; vacation, travel $325; other discretionary $500; dining, drinks, entertainment $365; grooming $50; pet $100; sports, hobbies $250; doctors, dentists $150; life insurance $45; cellphone $17; Internet $60. RRSPs $700; RESP $210; TFSAs $700; his pension plan contributions $300. Total: $6,717. Monthly surplus: $1,728. Liabilities: None. Required: Individually, prepare a professionally typed financial plan following the CIFP 6-steps. Remember that the financial planning process is meant to provide you with an opportunity to take what they have learned in this Retirement Planning course and demonstrate your financial planning skills. Step 6- Monitor and update Step 5 Implement the plan Step 4- Step 3- Identify appropriate strategies and present plan Clarify present status and identify problems and opportunities Step 2 Establish objectives and gather data Step 1- Establish client-planner engagement Some questions you will want to address within the sections of your report 1) In Step 1-look at the sample Engagement Letter and prepare one for your clients 2) Step 2 - Do the clients' retirement objectives seem clear enough? Do you require added clarification re: expected lifestyle at retirement? Do you require more information in order to know if objectives are in conflict (if so, what)? For the case submission, if you require information, state it in an Assumptions Section. In general, you can assume that your clients have and will continue to live modestly." 3) Step 3 - Provide a list of your client's current financial position and his or her future income potential and identify financial obligations or objectives that might interfere or conflict with the client's retirement objectives. If you require more information to complete the data- gathering worksheets, you may need to make reasonable assumptions (state them in your report) 4) Step 4 - once you have a good understanding of your clients' current financial position their retirement objectives, based on reasonable assumptions you can: project the income needed at retirement (over a likely time horizon) and determine the savings required to fund that level of income use the FPSC Projections Guidelines (pdf file) that is in the Assignment folder next to the case posting include your detailed projections in the Appendix to your report some specific questions you will want to answer prior to creating a financial plan: Should one or both take early CPP?" Have they fully maximized their TFSA room? How best should the phasing of their immediate and future cash flow needs be funded (from what source(s) when) during their lifetimes? 5) Steps 5 & 6-these sections can be brief as you will want to highlight what need to be done (NEXT STEPS) related to: . Step 5: Implement the Plan - once a strategy has been established, implement the plan What specialists, if any, would you want to consult at this stage Step 6: Monitor & Update - how often would you want to conduct periodic reviews and updates to evaluate progress towards your clients' retirement objectives

Expert Answer:

Related Book For

Posted Date:

Students also viewed these finance questions

-

1. Braun's Brakes manufactures three different product lines, Model X, Model Y, and Model Z. Considerable market demand exists for all models. The following per unit data apply: Which model has the...

-

Planning is one of the most important management functions in any business. A front office managers first step in planning should involve determine the departments goals. Planning also includes...

-

Certain environmental laws prohibit EPA from considering the costs of meeting various standards when the levels of the standards are set. Is this a good example of putting first things first or...

-

By the 1960s, a larger percentage of women were entering the labor force. Because more women were working, their production of services within the home, such as cooking and cleaning, may have fallen....

-

Compare the temperature dependence of the conductivity for metals and intrinsic semiconductors. Briefly explain the difference in behavior.

-

Explain the concept of earned value.

-

Beach Motors Inc. assembles and sells Dune Buggy engines. The company began operations on July 1, 2014, and operated at 100% of capacity during the first month. The following data summarize the...

-

Let f(x) = log(x + 1), g(x) = 10-x, and R be the region bounded by the graphs off and g, as shown above. a) Find the area of the region. b) Region R is the base of a solid. For this solid, each cross...

-

A natural gas trading company wants to develop an optimal trading plan for the next 10 days. The following table summarizes the estimated prices (per thousand cubic feet (cf)) at which the company...

-

A 696 g mass is placed on top of a spring. The other end of the spring is attached to the floor. You also push down on the mass with a force of 3.1 N. The spring moves downward a total of 0.279 m...

-

Considering the various uncontrollable environments that affect organizations, choose an industry and identify how each of the following might generally affect global supply chains: (a) economic; (b)...

-

With what orbital speed will a satellite circle Jupiter if placed at a height of 7.80 x 106 m above the surface of the planet? The mass of Jupiter is 1.90 x 1027 kg and the radius of Jupiter is 7.14...

-

Resistors of 10 and 20 Q are used in two circuits. In circuit 1, the resistors are placed in series with a 30V-battery. In circuit 2, the resistors are placed in parallel with the same battery. What...

-

A ball is thrown toward a cliff of heighth with a speed of 30 m/s and an angle of 60 above horizontal. It lands on the edge of the cliff 3.8 s later.

-

A hoop is rolling without slipping along a horizontal surface with a forward speed of 5 . 5 9 m / s when it starts up a ramp that makes an angle of 2 0 . 4 3 \ deg with the horizontal. What is the...

-

You are a human resource manager for an expanding local welding company and are looking for new welders. 1. Describe the employee search process you would use. 2. Describe the sources of potential...

-

Jax Incorporated reports the following data for its only product. The company had no beginning finished goods inventory and it uses absorption costing. $ 57.30 per unit $ 10.30 per unit $ 7.80 per...

-

What are the key differences between financing entrepreneurial and established companies?

-

What is the purpose of staged financing?

-

What are the main types of investors that fund entrepreneurial ventures?

Study smarter with the SolutionInn App