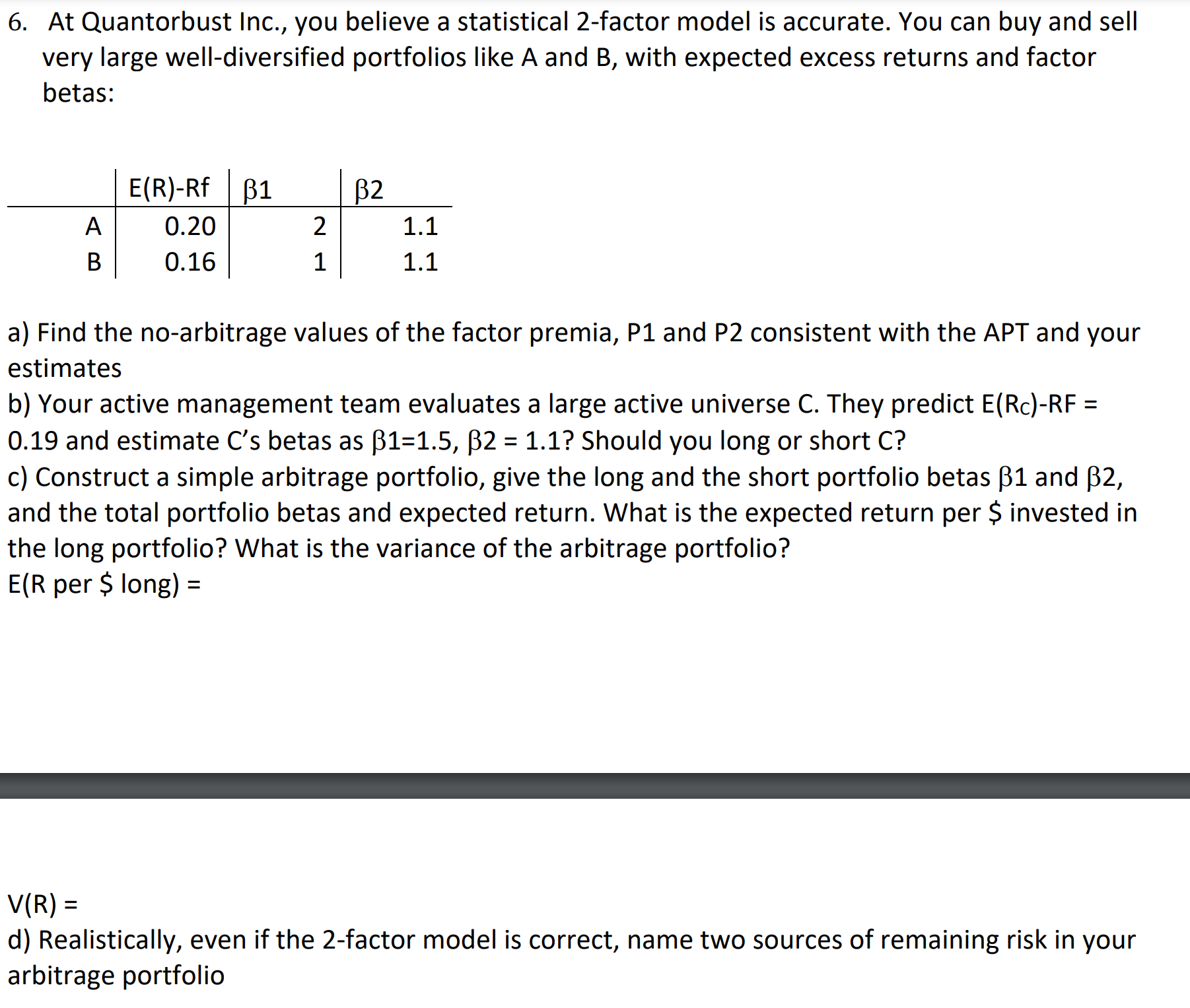

Question: At Quantorbust Inc., you believe a statistical 2 - factor model is accurate. You can buy and sell very large well - diversified portfolios like

At Quantorbust Inc., you believe a statistical factor model is accurate. You can buy and sell

very large welldiversified portfolios like A and B with expected excess returns and factor

betas:

a Find the noarbitrage values of the factor premia, P and P consistent with the APT and your

estimates

b Your active management team evaluates a large active universe They predict

and estimate Cs betas as Should you long or short C

c Construct a simple arbitrage portfolio, give the long and the short portfolio betas and

and the total portfolio betas and expected return. What is the expected return per $ invested in

the long portfolio? What is the variance of the arbitrage portfolio?

per $ long

d Realistically, even if the factor model is correct, name two sources of remaining risk in your

arbitrage portfolio

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock