Question: ITEM #1 LEARNING FROM THE HEADLINES True to the Learning from the Headlines approach of this course, watch the Part Three Intro Video after you

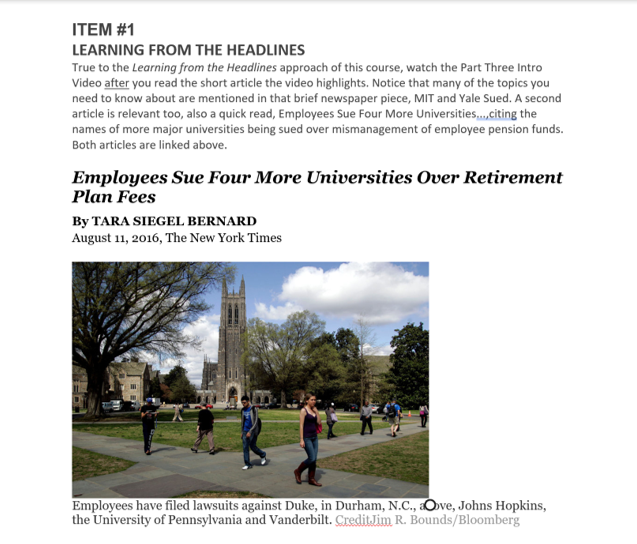

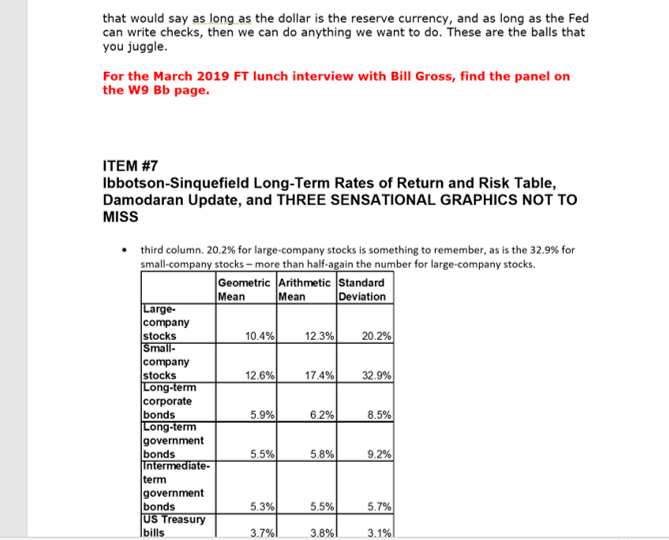

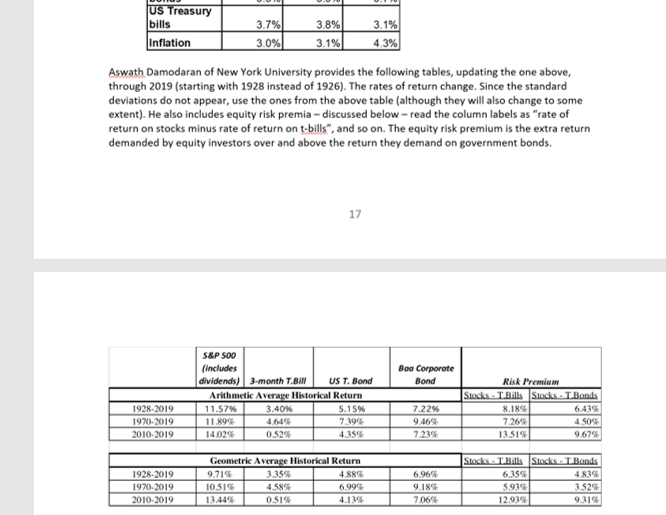

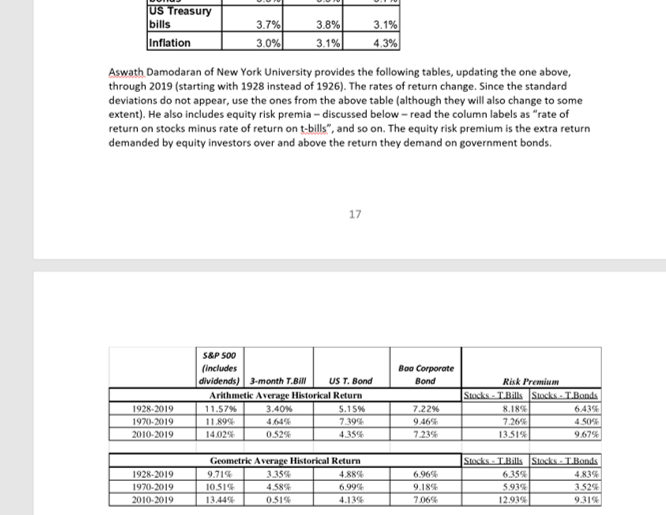

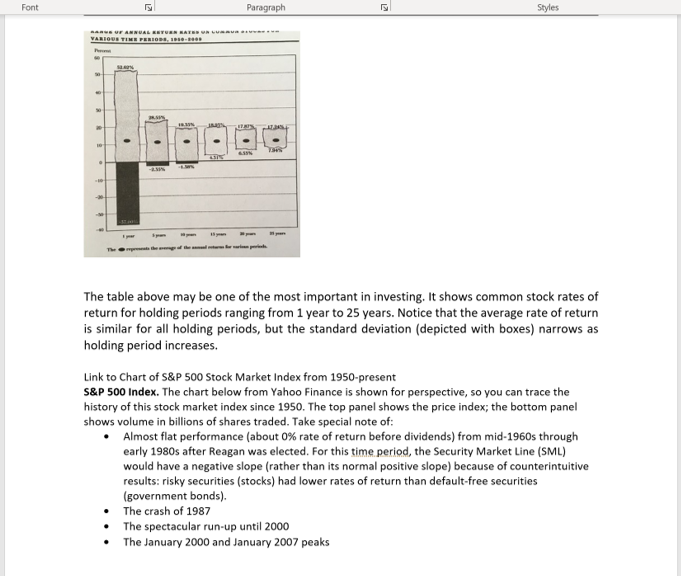

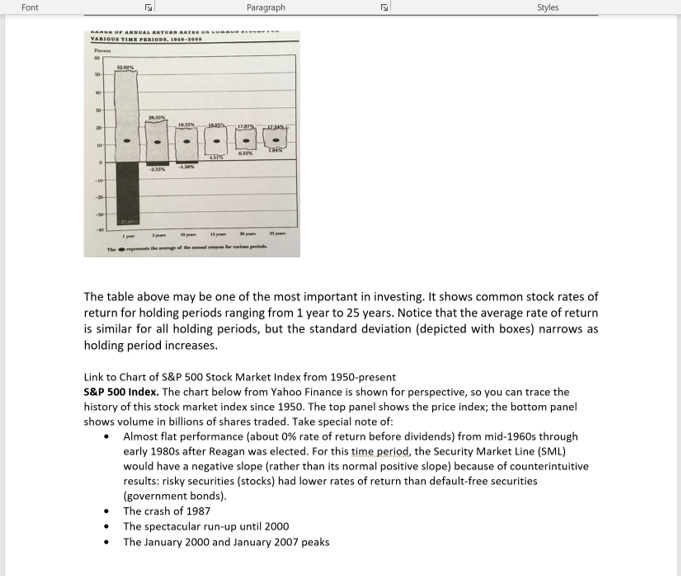

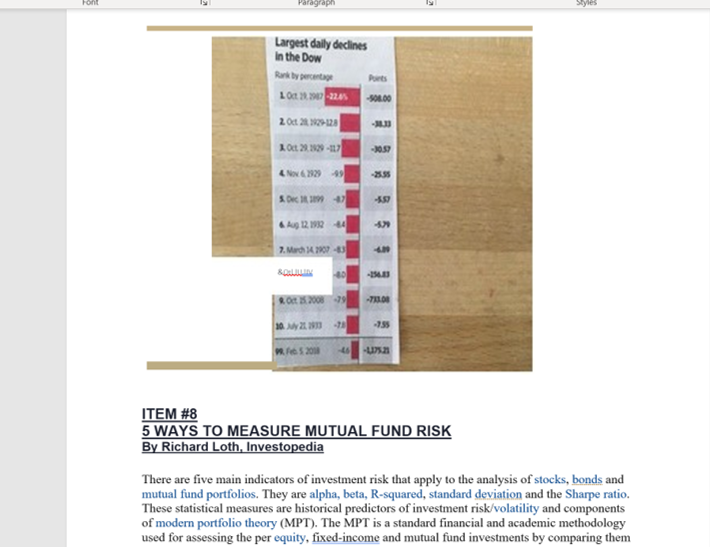

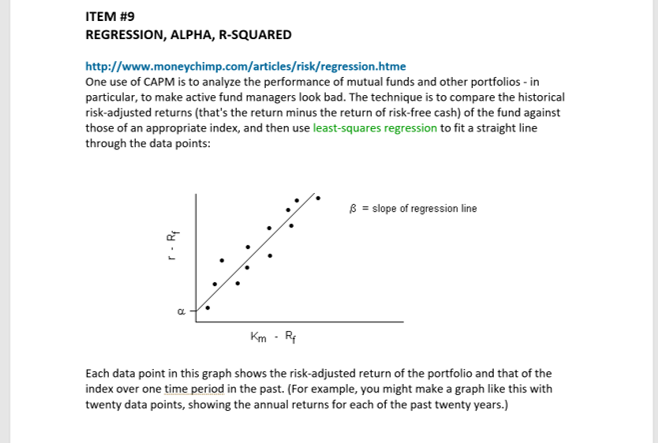

ITEM #1 LEARNING FROM THE HEADLINES True to the Learning from the Headlines approach of this course, watch the Part Three Intro Video after you read the short article the video highlights. Notice that many of the topics you need to know about are mentioned in that brief newspaper piece, MIT and Yale Sued. A second article is relevant too, also a quick read, Employees Sue Four More Universities,.., citing the names of more major universities being sued over mismanagement of employee pension funds. Both articles are linked above. Employees Sue Four More Universities Over Retirement Plan Fees By TARA SIEGEL BERNARD August 11, 2016, The New York Times Employees have filed lawsuits against Duke, in Durham, N.C., Cove, Johns Hopkins, the University of Pennsylvania and Vanderbilt. CreditJim R. Bounds/Bloombergalternatives. Until then, the typical endowment was far more conservative. And through his graduates, his investment style has spread to the nation's prominent schools and foundations. Today, Mr. Swensen and former proteges oversee nearly $100 billion in endowment money for schools including M.I.T., Stanford, the University of Pennsylvania, Bowdoin, Wesleyan and Princeton (which Mr. Golden manages). Other alumni are running the Rockefeller Foundation and the Ewing Marion Kauffman Foundation and working at the YMCA Retirement Fund and the Metropolitan Museum of Art. In an era when it is routine for money managers to elbow their way into the public consciousness - populating the news channels, burnishing their images - Mr. Swensen has largely stayed away from the spotlight, aside from writing a book, "Pioneering Portfolio Management." Yet he is one of the most influential people in a generation that has seen endowments grow tremendously in importance at premier institutions. Yale's endowment now provides 33 percent of the school's budget, compared with 10 percent in 1985. In a series of extended interviews, he and more than a half-dozen of his investment-office veterans discussed his management style - where they agree and disagree. Along the way Mr. Swanson gave his views on things as diverse as the pharmaceutical company Valeant - which "didn't even have the fig leaf of R.&D. expenditures," he said, to justify increasing its drug prices dramatically - to his toughest year, fiscal 2009, when his fund plummeted 24.6 percent during the economic meltdown. In the aftermath, he got hurt in a particularly bad real estate investment. "This is one of my biggest mistakes in the past 30 years," Mr. Swensen said. Over the decades, though, the Yale endowment has built one of the strongest records among the nation's largest endowments. Most recently, in the fiscal year ended June 30 - a dismal one for most schools, with the average endowment declining 2.7 percent, according to Cambridge Associates, which tracks performance - Yale's rose 3.4 percent. Play the Cards and the People Mr. Swensen, a lanky, soft-spoken native of River Falls, Wis., initially planned to become a teacher before going into the world of finance, where he understood it wasn't just about the numbers. "In poker, you can play the cards or you can play the people." said Randy Kim, who worked in the endowment office for a decade and went on to run the Conrad N. Hilton Foundation. "Dave could do both." Mr. Swensen's route to the endowment world was circuitous, though. "My father and my grandfather were both chemistry professors," he said. After earning a doctorate in economics from Yale in 1980, he considered teaching that subject. But while he was researching bond prices at Salomon Brothers for his Ph.D. dissertation, "they offered me a job," he said. Salomon was, of course, a Wall Street bond titan at the time and would eventually help define the go-go 1980s "Barbarians at the Gate" era of leveraged buyouts. All of that was still a few years in the future, though, and anyway, Mr. Swensen said, "I missed Yale so much that I went back to teach one class every semester." In 1985, the Yale provost, William C. Brainard, plucked him from Wall Street and asked him to take over the school's $1 billion endowment. His acceptance meant an 80 percent pay cut. But Mr. Swensen says he never regretted returning to work for anWall Street and asked him to take over the school's $1 billion endowment. His acceptance meant an 80 percent pay cut. But Mr. Swensen says he never regretted returning to work for an academic mission. "I am in the fortunate position of making very good money," he said, for something he loves doing. He made $5.1 million in 2014, the latest numbers available. From the beginning, he brought in analysts and interns to work on the portfolio. Part of that process soon included the weekly meeting to debate investment ideas. "Seeing that there was a debate, even at the most senior level, taught everyone to have their own view," Mr. Golden said. He recalled proposing at the time that Yale place some of its money with several money managers he had identified as promising. "They had good track records," he said. However, the debate centered on something different: "How good they would be going forward." In some cases, Yale selected a manager with little or no track record. That was the case with the Hillhouse Capital Group, an 9 investment fund focused on Chinese stocks that was begun in 2005 by Lei Zhang - himself a former underling of Mr. Swensen. That Hillhouse investment ended up taking Yale on a wild ride during the 2008 financial crisis. The value of the school's investment in Hillhouse fell nearly 44 percent, peak to trough. But instead of taking money out, Yale actually invested more in Hillhouse, convinced that Mr. Zhang's investment approach remained solid. For Mr. Swensen, the decision to stay in was logical. "Who cares about the trailing numbers if the fundamentals of the portfolio are good?" he said. That long term mind-set paid off. Hillhouse has generated more than a 20 percent average annual return since the endowment first invested in 2005. Explaining his investment strategies and other issues is onerous work. Mr. Swensen said his team worked on long quarterly reports that go to the endowment's investment committee. "I edit every single memo," he said. "I think that if you write your argument down, you might recognize flaws in it." Returns are central, of course, but a manager's track record - even if good on the bottom line must be balanced against whether that money manager's goals work in Yale's interest. The university has "close to 100 active relationships" with money-management firms, Mr. Swenseninvestment fund focused on Chinese stocks that was begun in 2005 by Lei Zhang - himself a former underling of Mr. Swensen. That Hillhouse investment ended up taking Yale on a wild ride during the 2008 financial crisis. The value of the school's investment in Hillhouse fell nearly 44 percent, peak to trough. But instead of taking money out. Yale actually invested more in Hillhouse, convinced that Mr. Zhang's investment approach remained solid. For Mr. Swensen, the decision to stay in was logical. "Who cares about the trailing numbers if the fundamentals of the portfolio are good?" he said. That long term mind-set paid off. Hillhouse has generated more than a 20 percent average annual return since the endowment first invested in 2005. Explaining his investment strategies and other issues is onerous work. Mr. Swensen said his team worked on long quarterly reports that go to the endowment's investment committee. "I edit every single memo," he said. "I think that if you write your argument down, you might recognize flaws in it." Returns are central, of course, but a manager's track record - even if good on the bottom line - must be balanced against whether that money manager's goals work in Yale's interest. The university has "close to 100 active relationships" with money-management firms, Mr. Swensen said. "The average length of a relationship is 13 years. That is a long time. It is all about being partners and who you choose." Against the *Asset Gatherers' There are some categories of manager that turn Mr. Swensen off. like the "asset gatherers," as he calls them, often famed for building mammoth investment funds by attracting scores of individual investors. "The Bill Grosses and Peter Lynches are about asset gathering" he said, referring to one of the founders of Pimco and to the former manager of Fidelity Investments' Magellan Fund. "More assets produce more fees, but they force managers to add more positions, not just Grade A ideas," he said. A Fidelity spokesman said Mr. Lynch's record spoke for itself. A representative for Mr. Gross declined to comment. Nor does leverage - the use of borrowed money to try to amplify returns - appeal to the Yale team. "We want managers who are interested in improving operations as a way to create value, as opposed to financial engineering." he said. The team applies a simple test when considering putting money with an investor who specializes in corporate buyouts: Add up the leverage in the investor's portfolio, and compare it with the leverage in the stock market (meaning the borrowing conducted by publicly traded companies). Leverage, after all, can become a millstone if things start to go wrong. "Debt restricts your ability to do things," Mr. Takahashi said. Mr. Swensen also has little patience for some activist investors like William A. Ackman of Pershing Square Capital Management, who has mounted public battles aimed at spurring target companies to revamp. "The drill is that they want return of capital, whether it comes from cash distributions or stock buybacks. That is an extraordinarily short-term orientation," Mr. Swensen said. "By and large, American companies are underinvesting for the future, and a lot of that has to do with either implicit or explicit pressure from activists." Mr. Swensen has been particularly critical of Mr. Ackman's highly publicized investment in Valeant, which in recent years stirred national controversy after it dramatically raised the prices on drugsSwensen has been particularly critical of Mr. Ackman's highly publicized investment in Valeant, which in recent years stirred national controversy after it dramatically raised the prices on drugs that it had bought the right to sell. "The excessive price increases abuse market power and create great profits, while burdening our health care system," he said. "The business model is at odds with sensible public policy. When Congress and the regulatory authorities catch on, the companies suffer," he said. A spokesman for Pershing Square, Francis McGill, said: "Pershing Square is a long-term investor which has improved the operations and performance of more than 30 corporations. It has never advocated short-term financial engineering techniques." Former analysts describe how they learned to be careful observers of personality and engagement when vetting prospective money managers. "We learned to look for managers who know their portfolios well," said Paula J. Volent, senior vice president for investments at Bowdoin College. 10 "If they have to look at a piece of paper in a meeting, then they don't really know." Anne Martin, a former Swensen intern who manages Wesleyan's endowment, described vetting one private equity fund. "We were near the end of the process. I worried that some of the terms were not fair, so I called the manager," she said, who adopted a dismissive tone. "I am not adjusting the terms this time, and I am not going to talk to you about it," she recalled him saying. "So I thought: This is a partnership, and there will be tough times, so how will it be then?" she said. Wesleyan didn't give him the money. Mr. Swensen's analysts have seen his standards prove costly to Yale. For instance, the endowment long had money with Michael Steinhardt, a well-known Wall Street trader, and it had been one of the school's most profitable investments. But in 1991, Mr. Steinhardt's firm was swept up in accusations of cornering the two-year Treasury market. The Steinhardt firm later settled, agreeing to pay $40 million without admitting wrongdoing. But Mr. Swensen had already taken Yale's money out that firm. That decision impressed D. Ellen Shuman, who worked at Yale from 1986 to 1998 and now runs Edgehill Endowment Partners, which manages $650 million for smaller endowments. "David put the reputation of theSteinhardt firm later settled, agreeing to pay $40 million without admitting wrongdoing. But Mr. Swensen had already taken Yale's money out that firm. That decision impressed D. Ellen Shuman, who worked at Yale from 1986 to 1998 and now runs Edgehill Endowment Partners, which manages $650 million for smaller endowments. "David put the reputation of the institution ahead of profits," she said. "It really affected me in my career." 'Not a Steppingstone" Newcomers often arrive at the investment office from the Yale School of Management, as did Peter H. Ammon, now manager of the University of Pennsylvania's endowment. But they take many routes. Seth Alexander, now head of M.I.T.'s endowment, taught at the business school, but did not attend. Robert F. Wallace, who runs the Stanford endowment, was a ballet dancer before going to Yale to study economics. Ms. Volent, who oversees the Bowdoin endowment, planned to be a museum director. And Mr. Golden, head of Princeton's endowment, had an "unsatisfying job at a small money management firm," he recalled. When he met Mr. Takahashi, Mr. Swensen's associate, Mr. Takahashi told him. "If you want to do good, we are looking for an intern." So Mr. Golden joined. Mr. Swensen says he is pleased when his analysts go to the nonprofit world. He never considered leaving Yale and was disappointed when, in 2007, Mohamed ElErian quit as head of the Harvard endowment, after less than two years, to return to Pimco. "Managing an endowment is a position of trust, not a steppingstone," Mr. Swensen said. Mr. El-Erian did not respond to a request for comment. Many Yale office graduates remain close, and they share investment ideas. Mr. Golden of Princeton said that when he finds good money managers, he prefers that they have other investors like Yale and Bowdoin, because they have similarly long time horizons. And when they do invest together. "Yale negotiates for everyone," said Ms. Volent. "We sit back and we let Yale do the hard work if the funds are too expensive." Ms. Shuman said in real estate investments, Mr. Swensen required a fee structure "where managers did not get any of the profits until there was a 6 percent hard return, or whatever number an investor could get from a passive investment at that time." The money managers objected - they wanted 20 percent on the entire profit - but lost. "David's way is fairer," she said. Mr. Swensen likes teaming up to invest with his former analysts. For one thing. it can reduce the risk of panicky withdrawals. "We were talking to a manager who just had capital taken away because the fund had a bad year," Mr. Swensen recalled. "The investor said, "Your five-year numbers are not so good, so we are firing you.' That sounds like the stupidest thing I ever heard," Mr. Swensen said. "When managers have to deal with stupid limited partners, they are not spending their time picking stocks," he said. There have been mistakes. Yale and schools that embraced its model stumbled when the market plummeted in 2008 because they had so much of their portfolios tied up in hard-to-sell assets. Mr. Swensen acknowledges that, going into 2008, "We were too illiquid, and now we are not as illiquid. We want 50 percent of our assets in liquid investments," he said. The real estate meltdown took a toll. Yale, alongwith a host of universities, put money into real estate funds run by Lubert-Adler - the judgment call Mr. Swensen referred to as his "biggest mistake." When one of the funds suffered steep losses as a result of investments in troubled golf resort projects, many schools were hurt. including Yale. Not every Yale-trained manager agrees with Mr. Swensen's investment parameters. Bowdoin has nearly twice as much in absolute return funds (which focus on asset appreciation, as opposed to performance against an index or benchmark) because the hedge fund manager Stanley Druckenmiller is on the Bowdoin investment committee and plays a role in picking managers. Ms. Volent of Bowdoin, whose returns have well outpaced the averages, pointed out that she has "a lot of money in global macroeconomic funds." She added, "They have been great for us, but David hates that area. He thinks no one can anticipate changes in currencies and interest rates." One might wonder about the value of Yale's investment philosophy when looking at the last year's performance. For the year ended June 30, a plain- vanilla portfolio of 60 percent stocks and 40 percent bonds outperformed more diversified portfolios (like those of endowments). However, over a 20-year run, Yale's average annual return has been 12.6 percent compared with 7.4 percent for the 60-40 portfolio. Mr. Swenson has no plans to alter his investment strategy, or to slow down. (He has been fighting cancer for four years, he said, and his condition is stable.) He remains convinced that diversification over the long term is crucial. "This is not a sprint," he said. "I am pretty happy with the numbers." A version of this article appears in print on November 6, 2016, on page BUI of the New York edition with the headline: The Endowment Guru. O 2016 The New York Times Company ITEM #6 ABOUT BILL GROSS - a video and two lunch interviews; Oct 2012 and March 2019 http://bloom.bg/2dPzt51 Janus Capital Fund Manager Bill Gross weighs in on the bond selloff and discusses his investment thoughts. He speaks with Erik Schatzker on "Bloomberg Markets". Watch the video. Star bond investor Bill Gross decamped from money manager Pacific Investment Management Company (PIMCO) in 2014 and now manages about $1.5 billion at Janus Capital, roughly half of which is his money. Gross says he was fired; PIMCO says he resigned. That disagreement is crucial. In OctoberInvestment Management Company (PIMCO) in 2014 and now manages about $1.5 billion at Janus Capital, roughly half of which is his money. Gross says he was fired; PIMCO says he resigned. That disagreement is crucial. In October 2015, Gross sued PIMCO for wrongful dismissal, seeking $200 million in damages that he says he will donate to charity. PIMCO tried to get the suit thrown out, but a California judge ruled it could proceed. Gross, who studied psychology at Duke, cofounded PIMCO in 1971 and led it for more than 4 decades. In January 2016 Gross and his wife pledged $40 million to the University of California at Irvine to create a nursing school. An avid stamp collector, Gross is said to have one of the most impressive collections on the planet. 12 THE LUNCH The obsessive life of bond guru Bill Gross JOANNA SLATER NEWPORT BEACH, CALIF. - The Globe and Mail Published Friday, Oct. 22, 2010 Last updated Thursday, Aug. 23, 2012One Sunday evening last year, Bill Gross was settling down in front of the television to watch some football when his wife's cellphone rang. "I've had a beer and a half - that's as far as I go - but I'm feeling good," he recalled earlier this month. His wife, Sue, picked up the phone and said, "It's for you, sweetheart - somebody by the name of Tim Geithner." One of the world's legendary investors, Mr. Gross doesn't have a cellphone. So when the U.S. Treasury Secretary needed to reach him, the call was routed to his wife. "We chatted for 30 minutes in my inebriated state about what to do about the U.S. economy," he says with an impish smile. The story is Mr. Gross's way of illustrating his political naivety, but it also says something about the role he occupies in finance, and especially the world of bonds. Mr. Gross is responsible for over $1-trillion of other people's money, which they have handed over in large part because of his reputation, stretching back decades, for turning it into more money. He is constantly sought out for his views, which at times represent market-shifting news. His statements might be considered oracular if there weren't so many of them. He believes that investors should face up to a "new normal," a world of feeble economic growth where returns on stocks and bonds are stubbornly low.At 66 years old, Mr. Gross is at a point in his career where most people are easing up on work, but slowing down doesn't appeal to him. Trading is one of the ways he expresses what he cheerfully describes as his "obsessive" personality. We're sitting in a very small conference room at his firm, Pacific Investment Management Co., better known as Pimco. On the table are two sandwiches in clear plastic containers - tuna for him, ham-and-cheese for me - and bottles of water. Out the window is Newport Beach, and beyond it, the Pacific Ocean. His lanky frame folded into a chair, Mr. Gross looks slightly rumpled. A sky-blue tie is draped slackly around his neck. His routine is unvarying: he rises at 4:30 a.m. and is in the office an hour later, before the trading day begins on the East Coast. At 8:30 a.m., he heads across the street to a Marriott hotel to exercise and practice yoga. It was during a yoga session several years ago that Mr. Gross had the idea to dispatch analysts to cities across the country to pose as homebuyers. They brought back street-level intelligence which confirmed Mr. Gross's hunch that the boom was out of hand. Pimco decided to avoid the world of subprime mortgages. "You get endorphins, you get free space, and all of a sudden simple little ideas just pop into your head," Mr. Gross says. "It seemed sort of heretical at the time, especially coming over and saying, 'The 10 of you, go there."" For a titan of finance, Mr. Gross doesn't hew to type. There's the yoga, the lack of a cellphone, the fact that he majored in psychology and once aspired to be a rock star. A man of enormous ambition, he is prone to loud bursts of laughter at his own expense. Mr. Gross is extremely wealthy, with a net worth of $2.1-billion (U.S.), according to Forbes magazine. Yet he eschews what a friend calls the "dog and pony shows" for the socially prominent in Orange County, the prosperous enclave south of Los Angeles where he lives and works. His idea of a good evening usually involves a quiet dinner with his wife. He adores his iPad and devours novels (thumbs up: Philip Roth, thumbs down: Jonathan Franzen).Lately, he has been trying to loosen up a bit in the office, where he prefers to focus, in silence, for hours in front of his trading screens. To break the quiet he helps impose, the morning we meet he starts a new ritual: at 8 a.m., a song that someone recommends is blasted over the sound system. Mr. Gross kicks it off with Short Skirt/Long Jacket by the alt-rock band Cake. He even helps lead a conga line past rows of stunned-looking traders. To hear Mr. Gross tell it, he has spent his life channelling his more compulsive tendencies. He once ran more than 120 miles over six days, from San Francisco to Carmel, not stopping even when his kidney ruptured. He amassed, piece by piece, what may be the world's finest stamp collection. 14 His roots, it turns out, are in Canada. Mr. Gross is a first-generation American, born in Ohio to parents originally from Winnipeg. His mother's family farmed wheat in Manitoba; his father, an executive with a steel company, played hockey. The path toward finance began with a near-death experience. A bad car accident in his final year in college sliced off much of his scalp. As he recuperated, he read a book which became a cult favourite among investors: Beat the Dealer by Edward Thorp, then a math professor. The book detailed how to win at blackjack by using a system for counting cards. After Mr. Gross recovered, he hopped a freight train to Las Vegas. Over the next four months, playing 16 hours a day, he turned $200 into $10,000.More leading universities have been sued on claims that their retirement plans charged employees excessive fees, following a series of similar suits filed earlier this week. In the latest round, complaints were filed in various federal courts on behalf of employees at Duke, Johns Hopkins, the University of Pennsylvania and Vanderbilt. The earlier lawsuits were filed against the Massachusetts Institute of Technology, New York University and Yaleon Tuesday. All of the complaints seek class-action status. 2 Jerome J. Schlichter, a lawyer well known for his pioneering litigation in the world of 401(k) retirement plans, is representing the plaintiffs. But with these suits, the spotlight has shifted to a more obscure corner of the retirement savings market, 403(b) plans, which are similar to 401(k) plans but are typically offered by public schools and nonprofit institutions like universities and hospitals. All of the suits, including the latest four, share similar overarching themes: The universities all used more than one provider, known as a record keeper, to operate their plans and perform the administrative services to keep them running. Had they consolidated to one provider, the plaintiffs claim, they could have used their bargaining power to negotiate much lower fees. Instead, the suits allege, the plans overpaid millions of dollars each year. The complaints also argue that the plans sponsored by the universities offered far too many investment options - many of which were too expensive - whenThe path toward finance began with a near-death experience. A bad car accident in his final year in college sliced off much of his scalp. As he recuperated, he read a book which became a cult favourite among investors: Beat the Dealer by Edward Thorp, then a math professor. The book detailed how to win at blackjack by using a system for counting cards. After Mr. Gross recovered, he hopped a freight train to Las Vegas. Over the next four months, playing 16 hours a day, he turned $200 into $10,000. He began thinking about the future. "I said, well, I obviously enjoy mathematical application of a system of some sort, and hard work, and diligence," he remembers, his sandwich and water still untouched. "What's the adult form of gambling? It's the stock market. Maybe you can't outfox it, but let's see if it can be done. Right then and there I said, 'I'm getting into the money management business."" He couldn't get a job working in stocks, so he started as a credit analyst at an insurance company in Newport Beach. Part of the job involved physically clipping bond coupons to receive the associated interest payments. Needless to say, Mr. Gross had bigger plans. Pimco got its start in 1971 under the insurer's umbrella. Two years later, when Mr. Gross's parents visited, he informed them he was going to be the best bond manager in the world. "Of course, they looked at me and said, 'What's that?" he recalls, laughing. Rather than simply hold bonds, Mr. Gross pioneered ways to trade them, generating fat profits. He employs complex mathematical tools but excels at making big-picture assessments of economies, markets and governments, which then direct his bets. "He seems to be able to make macro judgments about what's going to happen ahead of time, with a better batting average than chance by a significant amount," says Mr. Thorp, now a successful hedge-fund manager. The two men have lunch from time to time. Mr. Gross "has never been complacent," adds one former colleague. He "made sure he was a step ahead of the average investor in identifying potential land mines."Pimco, meanwhile, has become a colossus - indeed, some consider it too big. Its headquarters consists of two unremarkable buildings across from a shopping mall. Inside, it is well-appointed but not opulent (hedge funds a tiny fraction of Pimco's size have offices with more bling). It opened an office in Toronto in 2004 and plans to bring its mutual funds directly to Canadian investors. 15 Do obsessive 66-year-olds ever retire? If they're asked to, Mr. Gross says, naming other investing legends - Warren Buffett is 80 - who are still hard at work. "I like to think that I could recognize it in myself that I've lost it, but most of the time you don't," he says, laughing heartily. "I hope not to abuse the privilege of being one of the founders and therefore not being tapped on the shoulder when the time is right," he says. "But I think we're doing fine." BIOGRAPHY William Hunt Gross Born in 1944, 66 years old Educated at Duke University; MBA from the University of California, Los AngelesServed in the U.S. Navy during the Vietnam War Married, three children Hobbies: reading, collecting stamps, playing golf In 1971, helped found Pacific Investment Management Co.; as of this June, it managed $1.1-trillion (U.S.) Manages Pimco's Total Return Fund, the largest mutual fund in the world, with $252-billion in assets . Shares the title of chief investment officer at Pimco with Mohamed El-Erian, formerly an official at the International Monetary Fund and head of Harvard's endowment Has contributed millions to stem cell research, local hospitals, and Doctors Without Borders On growing up Even though your parents are dead, you're still looking over your shoulder saying, 'Mom or Dad, are you proud of me?' It's ridiculous when you're 66. For the most part, you grow up. You do make the transition. But all these obsessions along the way are really attempts for love and attention. On whether bonds' best days are over It is disheartening to some extent, but to be fair, I started in the midst of the beginning of one of the worst bear markets [for bonds]all the way until '81... I had a good first eight years in which I was smacked in the face with the reality that bonds can go down in price as well as up, so I don't forget that. On getting out of the crisis Ultimately the question becomes how many checks do you have to write, and how many checks can you write. A lot of people say you can't solve a debt crisis with more debt. You have a big contingent there. Then you have the other contingent...that would say as long as the dollar is the reserve currency, and as long as the Fed can write checks, then we can do anything we want to do. These are the balls that you juggle. For the March 2019 FT lunch interview with Bill Gross, find the panel on the W9 Bb page. ITEM #7 Ibbotson-Sinquefield Long-Term Rates of Return and Risk Table, Damodaran Update, and THREE SENSATIONAL GRAPHICS NOT TO MISS . third column. 20.2%% for large-company stocks is something to remember, as is the 32.9% for small-company stocks - more than half-again the number for large-company stocks. Geometric Arithmetic Standard Mean Mean Deviation Large- company stocks 10.4% 12.3% 20.2% Small- company stocks 12.6% 17.4% 32.9% Long-term corporate bonds 5.9% 6.2% 8.5% Long-term government bonds 5.5% 5.8% 9.2% Intermediate- term government bonds 5.3% 5.5% 5.7% US Treasury bills 3.7% 3.8% 3.1%US Treasury bills 3.7% 3.8% 3.1% Inflation 3.0% 3.1% 4.3% Aswath Damodaran of New York University provides the following tables, updating the one above, through 2019 (starting with 1928 instead of 1926). The rates of return change. Since the standard deviations do not appear, use the ones from the above table (although they will also change to some extent). He also includes equity risk premia - discussed below - read the column labels as "rate of return on stocks minus rate of return on t-bills", and so on. The equity risk premium is the extra return demanded by equity investors over and above the return they demand on government bonds. 17 SAP 500 includes Boo Corporate dividends) 3- month T.BIN US T. Bond Bond Risk Premium Arithmetic Average Historical Return Stocks - T.Bills Stocks - T.Bonds 1928-2019 11.57% 3.40% 5.15%% 7.22% 1970-2019 11.89% 4.649 7.39 9 46 7.26% 2010-2019 14.02% 0.524 1.35 7.23 13514 9.674 Geometric Average Historical Return Stocks - T.Bills Stocks - T.Bonds 1928-2019 9.714 3.354 4.884 6.964 6.354 4.834 1970-2019 10514 4.58 5.99 9.184 5.93 3.525 2010-2019 1344% 0.519 4.130 7.064 12.934 9.314US Treasury bills 3.7% 3.8% 3.1% Inflation 3.0% 3.1% 4.3% Aswath Damodaran of New York University provides the following tables, updating the one above, through 2019 (starting with 1928 instead of 1926). The rates of return change. Since the standard deviations do not appear, use the ones from the above table (although they will also change to some extent). He also includes equity risk premia - discussed below - read the column labels as "rate of return on stocks minus rate of return on t-bills", and so on. The equity risk premium is the extra return demanded by equity investors over and above the return they demand on government bonds. 17 SAP 500 includes Boo Corporate dividends) 3- month T.BIN US T. Bond Bond Risk Premium Arithmetic Average Historical Return Stocks - T.Bills Stocks - T.Bonds 1928-2019 11.57% 3.40% 5.15%% 7.22% 1970-2019 11.89% 4.649 7.39 9 46 7.26% 2010-2019 14.02% 0.524 1.35 7.23 13514 9.674 Geometric Average Historical Return Stocks - T.Bills Stocks - T.Bonds 1928-2019 9.714 3.354 4.884 6.964 6.354 4.834 1970-2019 10514 4.58 5.99 9.184 5.93 3.525 2010-2019 1344% 0.519 4.130 7.064 12.934 9.314Font Gil Paragraph Styles The open The table above may be one of the most important in investing. It shows common stock rates of return for holding periods ranging from 1 year to 25 years. Notice that the average rate of return is similar for all holding periods, but the standard deviation (depicted with boxes) narrows as holding period increases. Link to Chart of S&P 500 Stock Market Index from 1950-present 5&P 500 Index. The chart below from Yahoo Finance is shown for perspective, so you can trace the history of this stock market index since 1950. The top panel shows the price index; the bottom panel shows volume in billions of shares traded. Take special note of: Almost flat performance (about 0% rate of return before dividends) from mid-1960s through early 1980s after Reagan was elected. For this time period, the Security Market Line (SML) would have a negative slope (rather than its normal positive slope) because of counterintuitive results: risky securities (stocks) had lower rates of return than default-free securities (government bonds). The crash of 1987 The spectacular run-up until 2000 The January 2000 and January 2007 peaksFont Gil Paragraph Styles The open The table above may be one of the most important in investing. It shows common stock rates of return for holding periods ranging from 1 year to 25 years. Notice that the average rate of return is similar for all holding periods, but the standard deviation (depicted with boxes) narrows as holding period increases. Link to Chart of S&P 500 Stock Market Index from 1950-present 5&P 500 Index. The chart below from Yahoo Finance is shown for perspective, so you can trace the history of this stock market index since 1950. The top panel shows the price index; the bottom panel shows volume in billions of shares traded. Take special note of: Almost flat performance (about 0% rate of return before dividends) from mid-1960s through early 1980s after Reagan was elected. For this time period, the Security Market Line (SML) would have a negative slope (rather than its normal positive slope) because of counterintuitive results: risky securities (stocks) had lower rates of return than default-free securities (government bonds). The crash of 1987 The spectacular run-up until 2000 The January 2000 and January 2007 peaks. The June 2007 meltdown and recovery at January 2013 when the previous peak was exceeded The peak at January 2016 The Spring 2020 dive and the subsequent recovery. http://finance.yahoo.com/echarts?s=%5EGSPC+Interactive#symbol=%SEGSPC;range=my Use the link above to view a current S&P 500 historical chart. Click "Max" to display performance since 1950. Use the interactive feature to move horizontally through the chart. Click the links below to view three extraordinary graphics. "All the World's Stock Exchanges by Size" in one visualization, by Jeff Desjardins - February 17, 2017. Don't miss it; it's fabulous. (The same graphic is an item on the Week 9 Bb page.) https://www.visualcapitalist.com/all-of-the-worlds-stock-exchanges-by-size/ Another Jeff Desjardins graphic is "Stock Market Returns Over Different Time Periods (1872- 2018), dated March 11, 2019. It shows the vitally important fact portfolios help over long time horizons exhibit reduction rate of return volatility. https://www.visualcapitalist.com/stock-market-returns-time-periods-1872-2018/ https://www.visualcapitalist.com/all-of-the-worlds-money-and-markets-in-one-visualization- 2020/ Zoom the graphic below to put the media-hyped daily point drops in the stock market in proper perspective. Always think in ratio terms (ratios, relatives), not absolutes.Largest daily declines In the Dow ITEM #8 5 WAYS TO MEASURE MUTUAL FUND RISK By Richard Loth, Investopedia There are five main indicators of investment risk that apply to the analysis of stocks, bonds and mutual fund portfolios. They are alpha, beta, R-squared, standard deviation and the Sharpe ratio. These statistical measures are historical predictors of investment risk/volatility and components of modern portfolio theory (MPT). The MPT is a standard financial and academic methodology used for assessing the per equity, fixed-income and mutual fund investments by comparing themmutual fund portfolios. They are alpha, beta, R-squared, standard deviation and the Sharpe ratio. These statistical measures are historical predictors of investment risk/volatility and components of modern portfolio theory (MPT). The MPT is a standard financial and academic methodology used for assessing the per equity, fixed-income and mutual fund investments by comparing them to market benchmarks. All of these risk measurements are intended to help investors determine the risk-reward parameters of their investments. In this artic brief explanation of each of these commonly used indicators. Alpha Alpha is a measure of an investment's performance on a risk-adjusted basis. It takes the volatility (price risk) of a security or fund por compares its risk-adjusted performance to a benchmark index. The excess return of the investment relative to the return of the bench its "alpha." Simply stated, alpha is often considered to represent the value that a portfolio manager adds or 20 subtracts from a fund portfolio's return. Alpha of 1.0 means the fund has outperformed its benchmark index by 1%. Correspondingly, a similar negative alpha would indicate a underperformance of 1%. For investors, the more positive an alpha is, the better it is. Beta Beta, also known as the "beta coefficient," is a measure of the volatility, or systematic risk, of a security or a portfolio in comparison to a whole. Beta is calculated using regression analysis, and you can think of it as the tendency of an investment's return to respond to swings in the market. By definition, the market has a beta of 1.0. Individual security and portfolio values are measured according to how they deviate from the market.far too many investment options - many of which were too expensive - when cheaper alternatives were available. It also argued that the long lists of investments served only to confuse investors. For instance, Duke, which had $4-7 billion in assets held by nearly 38,000 participants at the end of 2014, used four providers (TIAA, Vanguard, Fidelity and Valic), offering 400 investment choices. In response to the suit, Michael J. Schoenfeld, Duke's vice president for public affairs and government relations, said the university offered a range of options to give employees more flexibility. Those investments, he added, "are reviewed and carefully managed in accord with federal law to provide low costs and good outcomes." Vanderbilt, which had $3.4 billion in assets and nearly 42,000 participants at the end of 2014, used the same four providers, offering 340 investment options, until April 2015. At that time, it consolidated to Fidelity and shrank its plan menu to a core set of 14 investment options, according to the suit, which argues that the changes should have come many years earlier. In addition, the complaint claims that the university continues to pay too much for record keeping- The suit also notes that Vanderbilt admitted that its older plan structure had caused employees to pay unreasonable record-keeping and investment fees. Beth Fortune, Vanderbilt's vice chancellor for public affairs, said that the university had not yet been served with the complaint and needed more time to respond. Johns Hopkins, with $4-3 billion in assets, offered more than 440 funds from its plan's five record keepers. In January, it reduced the number to three; the complaint argues that the changes did not go far enough.By definition, the market has a beta of 1.0. Individual security and portfolio values are measured according to how they deviate from the market. A beta of 1.0 indicates that the investment's price will move in lock-step with the market. A beta of less than 1.0 indicates that the investment is less volatile than the market, and, correspondingly, a beta of more than 1.0 indicates that the investment's price will be more volatile t market. For example, if a fund portfolio's beta is 1.2, it's theoretically 20% more volatile than the market. Conservative investors looking to preserve capital should focus on securities and fund portfolios with low betas, whereas those invest take on more risk in search of higher returns should look for high beta investments. R-Squared R-Squared is a statistical measure that represents the percentage of a fund portfolio's or security's movements that can be explained b in a benchmark index. For fixed-income securities and their corresponding mutual funds, the benchmark is the U.S. Treasury Bill, and equities and equity funds, the benchmark is the S&P 500 Index. R-squared values range from 0 to 100. According to Morningstar, a mutual fund with an R- squared value between 85 and 100 has a per record that is closely correlated to the index. A fund rated 70 or less would not perform like the index. Mutual fund investors should avoid actively managed funds with high R-squared ratios, which are generally criticized by analysts as b index funds. In these cases, why pay the higher fees for so-called professional management when you can get the same or better result index fund? Standard Deviation Standard deviation measures the dispersion of data from its mean. In plain English, the more that data is spread apart, the higher the d from the norm. In finance, standard deviation is applied to the annual rate of return of an investment to measure its volatility (risk). A would have a high standard deviation. With mutual funds, the standard deviation tells us how much the return on a fund is deviating f expected returns based on its historical performance. Sharpe RatioSharpe Ratio Developed by Nobel laureate economist William Sharpe, this ratio measures risk-adjusted 21 performance. It is calculated by subtracting rate of return (U.S. Treasury Bond) from the rate of return for an investment and dividing the result by the investment's standard dev return. The Sharpe ratio tells investors whether an investment's returns are due to smart investment decisions or the result of excess risk. This is very useful because although one portfolio or security can reap higher returns than its peers, it is only a good investment if those hi not come with too much additional risk. The greater an investment's Sharpe ratio, the better its risk- adjusted performance. The Bottom Line Many investors tend to focus exclusively on investment return, with little concern for investment risk. The five risk measures we have can provide some balance to the risk-return equation. The good news for investors is that these indicators are calculated for them and on several financial websites, as well as being incorporated into many investment research reports. As useful as these measurements a mind that when considering a stock, bond or mutual fund investment, volatility risk is just one of the factors you should be considering that affect the quality of an investment. ITEM #9 REGRESSION, ALPHA, R-SQUAREDITEM #9 REGRESSION, ALPHA, R-SQUARED http://www.moneychimp.com/articles/risk/regression.htme One use of CAPM is to analyze the performance of mutual funds and other portfolios - in particular, to make active fund managers look bad. The technique is to compare the historical risk-adjusted returns (that's the return minus the return of risk-free cash) of the fund against those of an appropriate index, and then use least-squares regression to fit a straight line through the data points: 6 = slope of regression line r - Rf Km - Rf Each data point in this graph shows the risk-adjusted return of the portfolio and that of the index over one time period in the past. (For example, you might make a graph like this with twenty data points, showing the annual returns for each of the past twenty years.)The general equation of this type of line is r - Ry = beta x ( Km - R ) + alpha where r is the fund's return rate, R is the risk-free return rate, and Km is the return of the index. Note that, except for alpha, this is the equation for CAPM - that is, the beta you get from Sharpe's derivation of equilibrium prices is essentially the same beta you get from doing a least- squares regression against the data. (Also note that alpha and beta are standard symbols that statisticians use all the time for this type of regression; Sharpe and his followers weren't trying to be obscure, as some people like to believe.) Beta is the slope of this line. Alpha, the vertical intercept, tells you how much better the fund did than CAPM predicted (or maybe more typically, a negative alpha tells you how much worse it did, probably due to high management fees). The quality of the fit is given by the statistical number r-squared. An r-squared of 1.0 would mean that the model fit the data perfectly, with the line going right through every data point. More realistically, with real data you'd get an r-squared of around .85. From that you would conclude that 85% of the fund's performance is explained by its risk exposure, as measured by beta. (Then you'd punch your fist in the air and say "And the other 15% is due to pure luck!" MPT never believes in investor skill: an investment's behavior equals that of its asset class, minus management fees, plus-or-minus unpredictable luck.)Font Paragraph Styles A spokeswoman said the university offers its employees "a generous and carefully managed benefits program, including for retirement," and is in the process of reviewing the lawsuit. A spokeswoman for the University of Pennsylvania, with $3.8 billion in assets at year-end 2014, said it employed a rigorous process to review all investment options, and ensured they were administered with the highest degree of care and prudence; she said the university planned to defend itself vigorously. ITEM #2 A Random Walk Down Wall Street From Wikipedia, the free encyclopedia https://en.wikipedia.org/wiki/A Random Walk Down Wall Street A Random Walk Down Wall Street, written by Burton Gordon Malkiel, a Princeton economist, is a book on the subject of stock markets which popularized the random walk hypothesis. Malkiel argues that asset prices typically exhibit signs of random walk and that one cannot consistently outperform market averages. The book is frequently cited by those in favor of the efficient-market hypothesis. As of 2019, there have been twelve editions and over 1.5 million copies sold.!' A practical popularization is The Random Walk Guide to Investing: Ten Rules for Financial Success,12 Contents 1 Investing techniques . 2 Alternative view Investing techniquesaragraph Investing techniques Malkiel examines some popular investing techniques, including technical analysis and fundamental analysis, in light of academic research studies of these methods. Through detailed analysis, he notes significant flaws in both techniques, concluding that, for most investors, following these methods will produce inferior results compared to passive strategies. Malkiel has a similar critique for methods of selecting actively managed mutual funds based upon past performance. He cites studies indicating that actively managed mutual funds vary greatly in their success rates over the long term, often underperforming in years following their success, thereby regressing toward the mean. Malkiel suggests that given the distribution of fund performances, it is statistically unlikely that an average investor would happen to select those few mutual funds which will outperform their benchmark index over the long term. Alternative view In 1984 Warren Buffett gave a speech at Columbia University rebutting Malkiel's book and the Efficient Market Hypothesis. See The Superinvestors of Graham-and-Doddsville. As of 2013 Malkiel has not yet responded, and has ignored Buffett's argument. As Seth Klarman has stated: "Buffett's argument has never, to my knowledge, been addressed by the efficient-market theorists; they evidently prefer to continue to prove in theory what was refuted in practice" john naked However in 2014's letter "To the Shareholders of Berkshire Hathaway Inc." (page 20) Buffett revealed his instructions in his will (in addition to his investment strategy, as a professional, while alive) to the trustee for his wife's benefit: It's vital, however, that we recognize the perimeter of our "circle of competence" and stay well inside of it [..] Most investors, of course, have not made the study of business prospects a priority in their lives. If wise, they will conclude that they do not know enough about specific businesses to predict their future earning power. I have good news for these non-professionals: The typical investor doesn't need this skill.The goal of the non-professional should not be to pick winners - neither he nor his "helpers" can do that. Put 10% in short-term government bonds and 90% in a very low-cost S&P 500 index fund. (I suggest Vanguard's.) I believe the trust's long-term results from this policy will be superior to those attained by most investors - whether pension funds, institutions or individuals - who employ high-fee managers. ITEM #3 Charles T. Akre From Wikipedia, the free encyclopedia Charles T. "Chuck" Akre is an American investor, financier and businessman. He serves on the board of directors of Enstar Group, Lid., a Bermuda run-off reinsurance company, he is also the founder, chairman and chief investment officer of Akre Capital Management, FBR Focus, and other funds. Akre Capital Management is based in Middleburg, Virginia. Early life Akre grew up in Washington D.C., graduated from Blair Academy and matriculated to American University, where he obtained a BA in English Literature. After deciding against going to medical school, Akre started in the securities business in 1968. Career Akre held positions as shareholder, Director, CEO of the Asset Management Division and Director of Research at Johnston, Lemon & Co. (a NYSE member firm). Akre established his own firm, Akre Capital Management, in 1989 and operated it as part of Friedman, Billings, Ramsey & Co. until 1999. In 2000, ACM became independent again. Akre established its current location in Middleburg, Virginia in early 2002 while running the FBR Focus Fund, a small- and mid-cap value mutual fund. While Akre was managing the FBR Focus, it performed in the top 1% of small/mid-cap growth funds in 2002, 2004, and 2006, as well as the 2nd percentile in 2001 and the 6th percentile in 2008. In 2008, Akre's FBR Small Cap Value fund consisted of $55 million; in total in 2003 Akre managed about $135 million." After breaking fromFBR, Akre started the Akre Focus Fund in 2009. As of 2009 the fund had about $800 million in assets, while Akre had a seven figure stake in the fund." Akre Capital Management is a long-term, concentrated value investment firm. Akre's and his team of analysts do intense research, and are known for their contrarian investments, most notably in the cell phone tower space during 2001-2003. "I've managed the portfolio the whole time and I've never changed the investment approach," Akre said to CNN Money. "We've been all of them. I don't box myself in." ;) Investment approach Charles Akre uses an investment philosophy that he calls the "three-legged stool" approach, which calls for examining business models, rates of retum, and reinvestment opportunities. The stool is a reference to a three-legged milking stool he keeps in his office - because it is low to the ground, a farmer sitting on it would not fall far if it flipped over. The implication for investing is that if the economy is rattled, fund investors won't be hit with serious damage.( Good investments are businesses that possess four characteristics: 1. Good managers with demonstrated track records 2. Significant and durable competitive advantages 3. Long-term growth/reinvestment opportunities 4. Attractive purchase prices relative to the cash flows generated by the company https://www.youtube.com/watch?v=eEO5G1SjCeU Watch this video of Chuck Akre explaining what he does to outperform the index year-in and year-out.COMMON SENSE INVESTING Your Four Share of Sand Marin Erterms JOHN G. BOGLE Having had cardiac troubles since his 30s, Bogle underwent a heart transplant in 1996. So Bogle could focus on his health issues, John Brennan was named as his replacement. Bogle recovered and remained on the board as senior chairman. He later told the Los Angeles Times that the experience was "almost mystical" and said he was doing well -- playing squash and climbing mountains. Fortune archive 2009 Bogle died on January 16, 2019. A flood of laudatory obits ensued. Here is one by Jason Zweig of the Wall Street Journal. It contains links to more reflections about Jack Bogle. https://www.wsj.com/articles/what-drove-jack-bogle-to-upend-investing- 11547812810?mod article_inlineBUSINESS DAY The Money Management Gospel of Yale's Endowment Guru By GERALDINE FABRIKANT, The New York Times, NOV. 5, 2016 As he has done for decades, once a week David F. Swensen convenes his staff - including his cadre of apprentices - for a morning-long meeting among the Gothic revival flourishes and crenelations of the Yale University campus to debate investment ideas. Mr. Swensen, 62, runs the school's $25.4 billion endowment, one of the largest in the country. Usually he is joined by his intellectual sparring partner, Dean Takahashi, his senior director. It amounts to an internship in the world of managing a university's billions - and the young analysts have a front-row seat. "It was like watching a 70-year-old married couple go at it in full force," recalled Andrew Golden, who was one of those Swensen acolytes in the 1980s. But forget what you think about internships and fetching doughnuts for the bosses. The meetings are supposed to be a crucible of ideas, and the analysts - some of whom stay in the positions for years - recalled bringing their own proposals in the early days. and having to defend them or face the music. "It could be jarring to have your own view shredded by them," Mr. Golden said. As for Mr. Swensen, it's an environment that brings together two things he loves: thinking about investments and teaching other people how to think about them. "They are twin passions of mine," he said during a recent interview in his sun-filled corner office at the endowment's headquarters on Yale's New Haven campus. Certainly no school has incubated as many endowment managers as Yale. Mr. Swensen is legendary in the rarefied world of endowment management. He has pioneered an investment strategy that expanded Yale's portfolio from a plain vanilla mix of stocks and bonds to substantial holdings in real estate, private equity and venture capital, along with other

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Finance Questions!