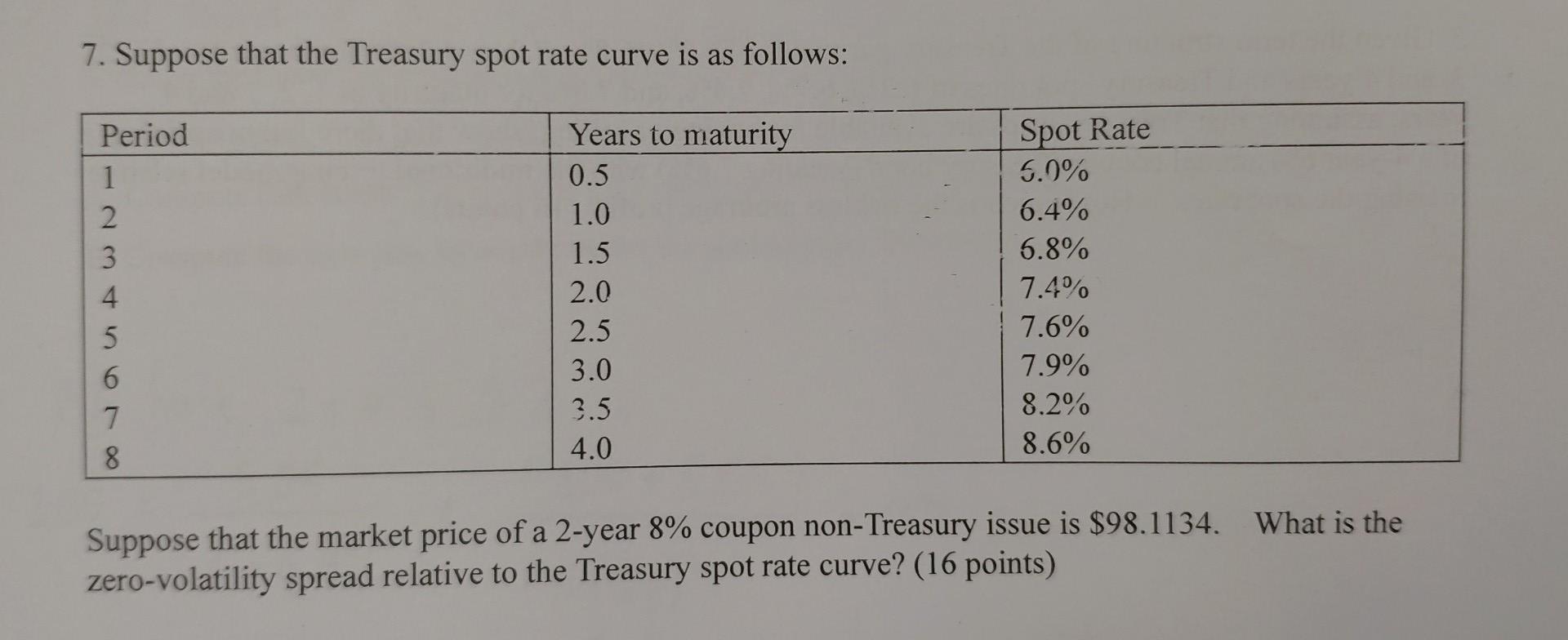

Question: 7. Suppose that the Treasury spot rate curve is as follows: Years to maturity 0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0 Period 1

7. Suppose that the Treasury spot rate curve is as follows: Years to maturity 0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0 Period 1 2 3 4 5 6 7 8 Spot Rate 5.0% 6.4% 5.8% 7.4% 7.6% 7.9% 8.2% 8.6% Suppose that the market price of a 2-year 8% coupon non-Treasury issue is $98.1134. What is the zero-volatility spread relative to the Treasury spot rate curve? (16 points)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Zero volatility spread is added to the treasury spot rate ... View full answer

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock