Question: Auditing: Comprehensive Problem . Please answer what is in the Required. You can put the answer on this excel sheet that I'll be providing or

Auditing: Comprehensive Problem .

Please answer what is in the "Required". You can put the answer on this excel sheet that I'll be providing or provide your own sheet.

a.) Item #16 on letter d. it should be 240,000 not 200,000 (the amount to pay)

b.) Item #20, income tax rate should be 35%

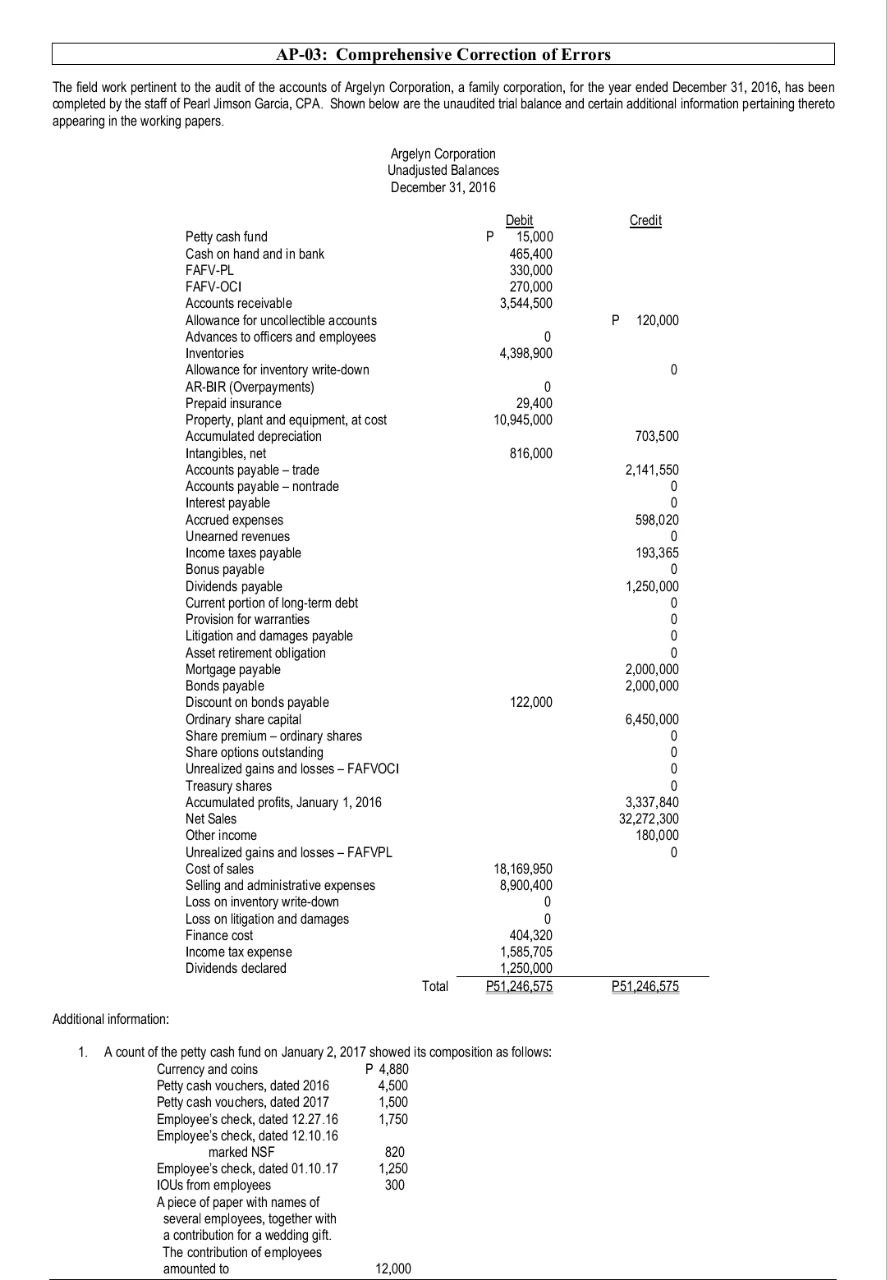

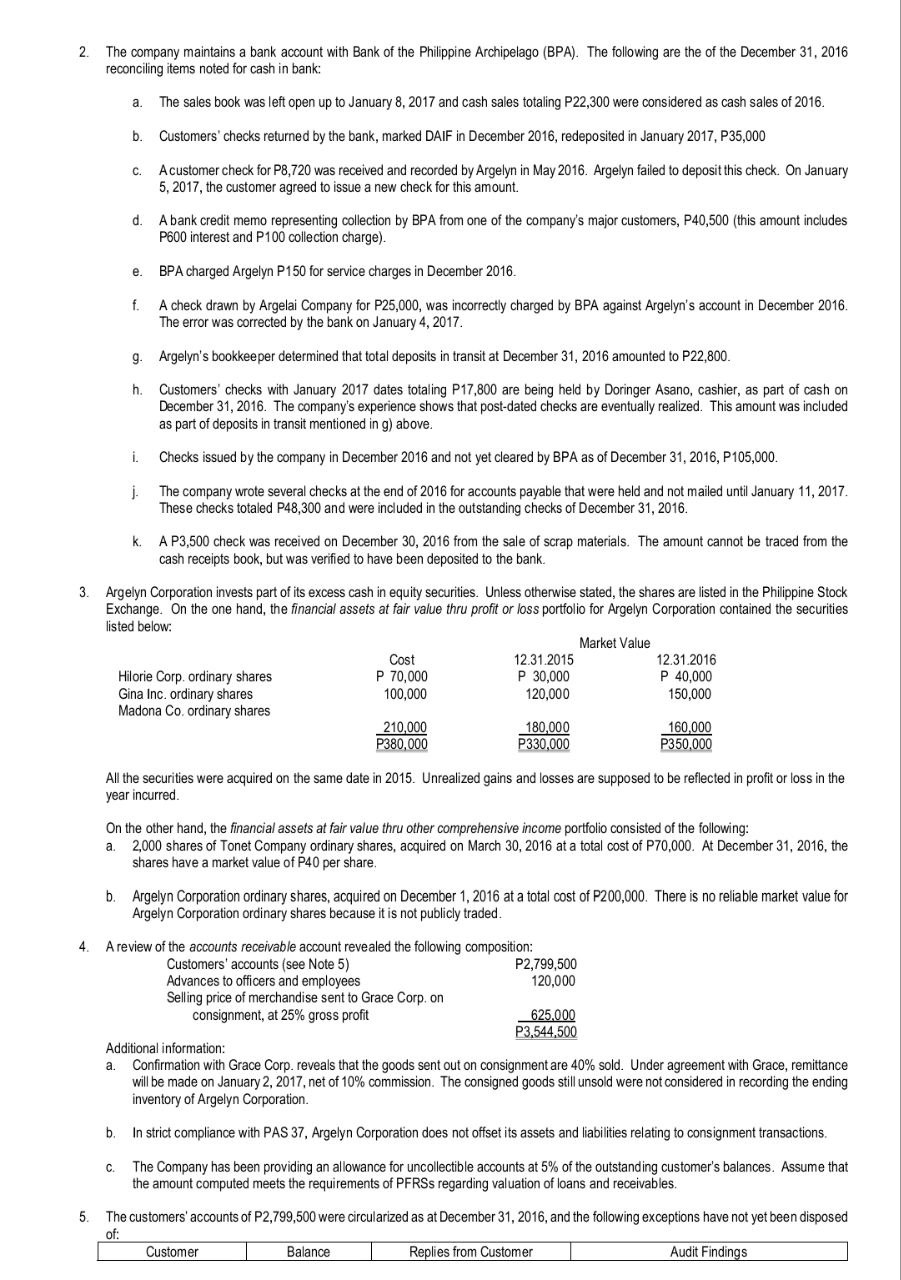

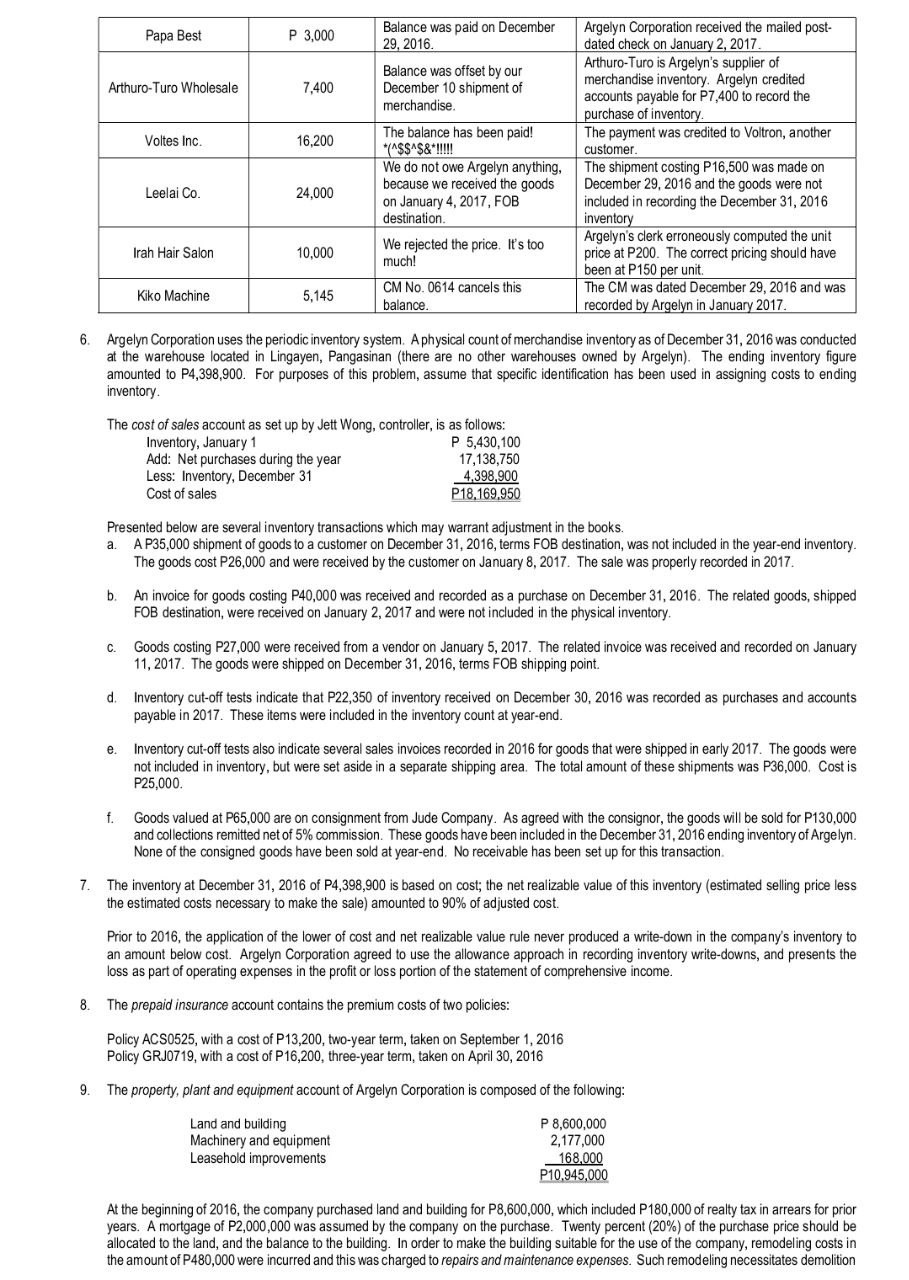

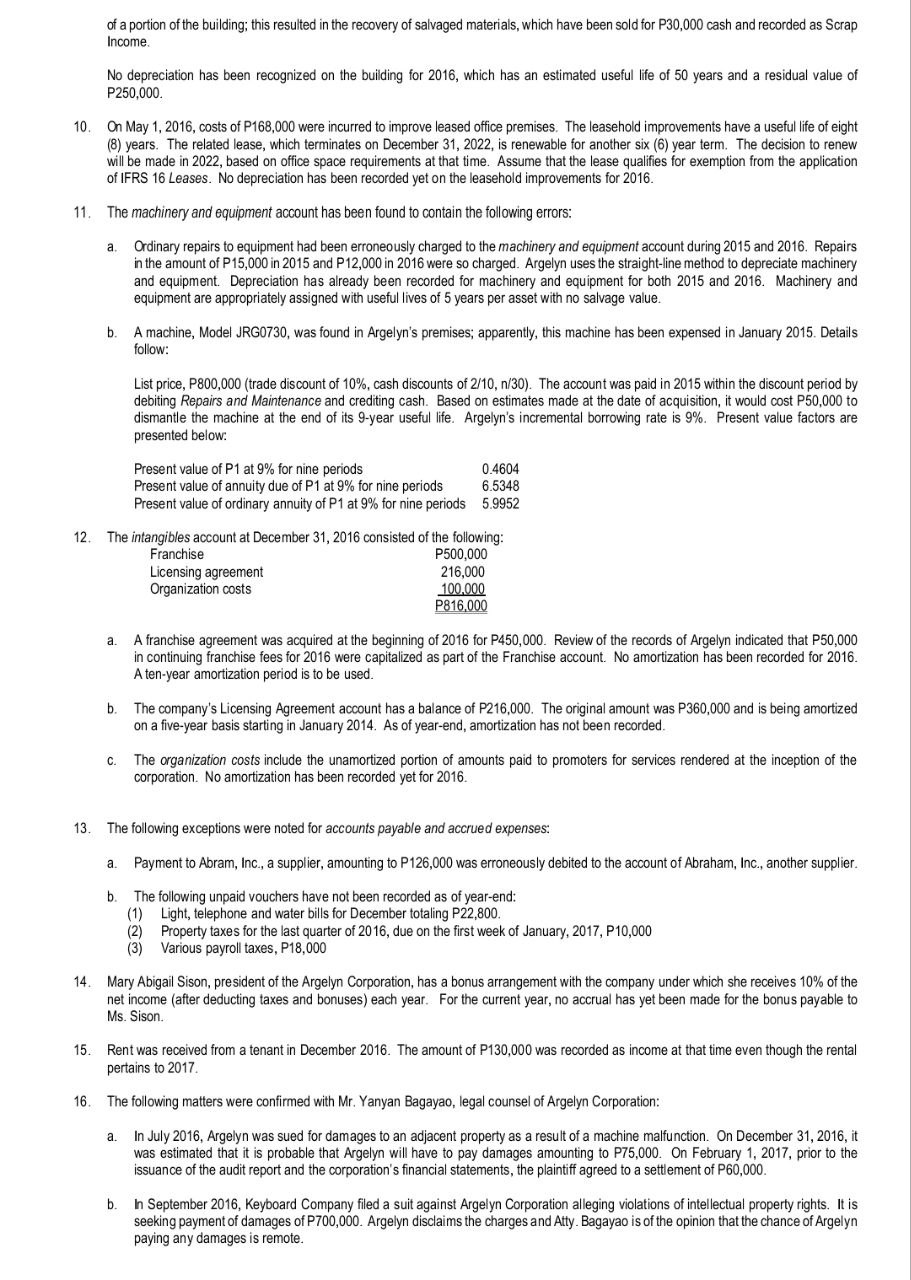

AP-03: Comprehensive Correction of Errors The field work pertinent to the audit of the accounts of Argelyn Corporation, a family corporation, for the year ended December 31, 2016, has been completed by the staff of Pearl Jimson Garcia, CPA. Shown below are the unaudited tral balance and certain additional information pertaining thereto appearing in the working papers. Argelyn Corporation Unadjusted Balances December 31, 2016 Debit Credit Petty cash fund P 15,000 Cash on hand and in bank 465,400 FAFV-PL 330,000 FAFV-OCI 270,000 Accounts receivable 3,544,500 Allowance for uncollectible accounts P 120,000 Advances to officers and employees 0 Inventories 4,398,900 Allowance for inventory write-down 0 AR-BIR (Overpayments) 0 Prepaid insurance 29,400 Property, plant and equipment, at cost 10,945,000 Accumulated depreciation 703,500 Intangibles, net 816,000 Accounts payable trade 2,141,550 Accounts payable - nontrade 0 Interest payable 0 Accrued expenses 598,020 Unearned revenues 0 Income taxes payable 193,365 Bonus payable 0 Dividends payable 1,250,000 Current portion of long-term debt 0 Provision for warranties 0 Litigation and damages payable 0 Asset retirement obligation 0 Mortgage payable 2,000,000 Bonds payable 2,000,000 Discount on bonds payable 122,000 Ordinary share capital 6,450,000 Share premium ordinary shares 0 Share options outstanding 0 Unrealized gains and losses FAFVOC| 0 Treasury shares 0 Accumulated profits, January 1, 2016 3,337,840 Net Sales 32,272,300 Other income 180,000 Unrealized gains and losses - FAFVPL 0 Cost of sales 18,169,950 Selling and administrative expenses 8,900,400 Loss on inventory write-down 0 Loss on litigation and damages 0 Finance cost 404,320 Income tax expense 1,585,705 Dividends declared 1,250,000 Total P51,246,575 P51,246,575 Additional information: 1. Account of the petty cash fund on January 2, 2017 showed its composition as follows: Currency and coins P 4,880 Petty cash vouchers, dated 2016 4.500 Petty cash vouchers, dated 2017 1,500 Employee's check, dated 12.27.16 1,750 Employee's check, dated 12.10.16 marked NSF 820 Employee's check, dated 01.10.17 1,250 |OUs from employees 300 A piece of paper with names of several employees, together with a contribution for a wedding gift. The contribution of employees amounted to 42,000 2. 3. 5. The company maintains a bank account with Bank of the Philippine Archipelago (BPA). The following are the of the December 31, 2016 reconciling items noted for cash in bank: b. The sales book was left open up to January 8, 2017 and cash sales totaling P22,300 were considered as cash sales of 2016. Customers' checks returned by the bank, marked DAIF in December 2016, redeposited in January 2017, P35,000 Acustomer check for P8,720 was received and recorded by Argelyn in May 2016. Argelyn failed to deposit this check. On January 5, 2017, the customer agreed to issue a new check for this amount. Abank credit memo representing collection by BPA from one of the company's major customers, P40,500 (this ammount includes P600 interest and P100 collection charge). BPA charged Argelyn P150 for service charges in December 2016. Acheck drawn by Argelai Company for P25,000, was incorrectly charged by BPA against Argelyn's account in December 2016. The error was corrected by the bank on January 4, 2017. Argelyn's bookkeeper determined that total deposits in transit at December 31, 2016 amounted to P22,800_ Customers' checks with January 2017 dates totaling P17,800 are being held by Doringer Asano, cashier, as part of cash on December 31, 2016. The company's experience shows that past-dated checks are eventually realized. This amount was included as part of deposits in transit mentioned in g) above. Checks issued by the company in December 2016 and not yet cleared by BPA as of December 31, 2016, P105,000. The company wrote several checks at the end of 2016 for accounts payable that were held and not mailed until January 11, 2017. These checks totaled P48,300 and were included in the outstanding checks of December 31, 2016. A P3,500 check was received on December 30, 2016 from the sale of scrap materials. The amount cannot be traced from the cash receipts book, but was verified to have been deposited to the bank. Argelyn Corporation invests part of its excess cash in equity securities. Unless otherwise stated, the shares are listed in the Philippine Stock Exchange. On the one hand, the financial assets af fair value thru profit or loss portfolio for Argelyn Corporation contained the securities listed below: Market Value Cost 12.31.2015 12.31.2016 Hilorie Corp. ordinary shares P 70,000 P 30,000 P 40,000 Gina Inc. ordinary shares 100,000 120,000 150,000 Madona Co, ordinary shares 210,000 180,000 160,000 P380,000 P330,000 P350,000 All the securities were acquired on the same date in 2015. Unrealized gains and losses are supposed to be reflected in profit or loss in the year incurred. On the other hand, the financial assets at fair value thru other comprehensive income portfolio consisted of the following: a. 2,000 shares of Tonet Company ordinary shares, acquired on March 30, 2016 ata total cost of P70,000. At December 31, 2016, the shares have a market value of P40 per share. b. Argelyn Corporation ordinary shares, acquired on December 1, 2016 at a total cost of P200,000. There is no reliable market value for Argelyn Corporation ordinary shares because itis not publicly traded. Areview of the accounts receivable account revealed the following composition: Customers' accounts (see Note 5) P2,799,500 Advances to officers and employees 120,000 Selling price of merchandise sent to Grace Corp. on consignment, at 25% gross profit 625,000 P3,544,500 Additional information: a. Confirmation with Grace Corp. reveals that the goods sent out on consignment are 40% sold. Under agreement with Grace, remittance will be made on January 2, 2017, net of 10% commission. The consigned goods still unsold were not considered in recording the ending inventory of Argelyn Corporation. b. In strict compliance with PAS 37, Argelyn Corporation does not offset its assets and liabilities relating to consignment transactions. c. The Company has been providing an allowance for uncollectible accounts at 5% of the outstanding customer's balances. Assume that the amount computed meets the requirements of PFRSs regarding valuation of loans and receivables. The customers' accounts of P2,799,500 were circularized as at December 31, 2016, and the following exceptions have not yet been disposed of: [ Customer Balance Replies from Customer Audit Findings | Balance was paid on December Argelyn Corporation received the mailed post- Papa Best P 3,000 29, 2016. dated check on January 2, 2017. Arthuro-Turo is Argelyn's supplier of Arthuro-Turo Wholesale 7,400 Docarnbor 10 ahenosrt of Dacsgesieetincal Sea all aban , naachandicn P accounts payable for P7,400 to record the : purchase of inventory. The balance has been paid! The payment was credited to Voltron, another eee Ret *(ASSSSS" MM! customer. We do not owe Argelyn anything, | The shipment costing P16,500 was made on Leelai Co 24.000 because we received the goods December 29, 2016 and the goods were nat : ; on January 4, 2017, FOB included in recording the December 31, 2016 destination. invento ; ; ; Argelyn's clerk erroneously computed the unit irah Hair Salon 10,000 We fejected the price, W's100 | rice at P200. The correct pricing should have : been at P150 per unit. , . CM No. 0614 cancels this The CM was dated December 29, 2016 and was Fn SEE 18 | balance. recorded by Argelyn in January 2017. Argelyn Corporation uses the periodic inventory system. A physical count of merchandise inventory as of December 31, 2016 was conducted at the warehouse located in Lingayen, Pangasinan (there are no other warehouses owned by Argelyn). The ending inventory figure amounted to P4,398,900. For purposes of this problem, assume that specific identification has been used in assigning costs to ending inventory. The cost of sales account as set up by Jett Wong, controller, is as follows: Inventory, January 1 P 5,430,100 Add: Net purchases during the year 17,138,750 Less: Inventory, December 31 4,398,900 Cost of sales P18,169,950 Presented below are several inventory transactions which may warrant adjustment in the books. a. A P35,000 shipment of goods to a customer on December 31, 2016, terms FOB destination, was not included in the year-end inventory. The goods cost P26,000 and were received by the customer on January 8, 2017. The sale was properly recorded in 2017. b. An invoice for goods costing P40,000 was received and recorded as a purchase on December 31, 2016. The related goods, shipped FOB destination, were received on January 2, 2017 and were not included in the physical inventory. c. Goods costing P27,000 were received from a vendor on January 5, 2017. The related invoice was received and recorded on January 11, 2017. The goods were shipped on December 31, 2016, terms FOB shipping point. d. Inventory cut-off tests indicate that P22,350 of inventory received on December 30, 2016 was recorded as purchases and accounts payable in 2017. These items were included in the inventory count at year-end. e. Inventory cut-off tests also indicate several sales invoices recorded in 2016 for goods that were shipped in early 2017. The goods were not included in inventory, but were set aside in a separate shipping area. The total amount of these shipments was P36,000. Costis P25,000. f. Goods valued at P65,000 are on consignment from Jude Company. As agreed with the consignor, the goods will be sold for P130,000 and collections remitted net of 5% commission. These goods have been included in the December 31, 2016 ending inventory of Argelyn. None of the consigned goods have been sold at year-end. No receivable has been set up for this transaction The inventory at December 31, 2016 of P4,398,900 is based on cost; the net realizable value of this inventory (estimated selling price less the estimated costs necessary to make the sale) amounted to 90% of adjusted cost. Prior to 2016, the application of the lower of cost and net realizable value rule never produced a write-down in the company's inventory to an amount below cost. Argelyn Corporation agreed to use the allowance approach in recording inventory write-downs, and presents the loss as part of operating expenses in the profit or loss portion of the statement of comprehensive income. The prepaid insurance account contains the premium costs of two policies: Policy ACS0525, with a cost of P13,200, two-year term, taken on September 1, 2016 Policy GRJO719, with a cost of P16,200, three-year term, taken on April 30, 2016 The property, plant and equipment account of Argelyn Corporation is composed of the following: Land and building P 8,600,000 Machinery and equipment 2,177,000 Leasehold improvements 168,000 P10,945,000 At the beginning of 2016, the company purchased land and building for P8,600,000, which included P180,000 of realty tax in arrears for prior years. A mortgage of P2,000,000 was assumed by the company on the purchase. Twenty percent (20%) of the purchase price should be allocated to the land, and the balance to the building. In order to make the building suitable for the use of the company, remodeling costs in the amount of P480,000 were incurred and this was charged to repairs and maintenance expenses. Such remodeling necessitates demolition of a portion of the building; this resulted in the recovery of salvaged materials, which have been sold for P30,000 cash and recorded as Scrap Income. No depreciation has been recognized on the building for 2016, which has an estimated useful life of 50 years and a residual value of P250,000. On May 1, 2016, costs of P168,000 were incurred to improve leased office premises. The leasehold improvements have a useful life of eight (8) years. The related lease, which terminates on December 31, 2022, is renewable for another six (6) year term. The decision to renew will ba made in 2022, based on office space requirements at that time. Assume that the lease qualifies for exemption from the application of IFRS 16 Leases. No depreciation has been recorded yet on the leasehold improvements for 2016. The machinery and equipment account has been found to contain the following errors: a, Ordinary repairs to equipment had been erroneously charged to the machinery and equipment account during 2015 and 2016. Repairs inthe amount of P15,000 in 2015 and P12,000 in 2016 were so charged. Argelyn uses the straight-line method to depreciate machinery and equipment. Depreciation has already been recorded for machinery and equipment for both 2015 and 2016. Machinery and equipment are appropriately assigned with useful lives of 5 years per asset with no salvage value. b. Amachine, Model JRGO730, was found in Argelyn's premises; apparently, this machine has been expensed in January 2015. Details follow: List price, P800,000 (trade discount of 10%, cash discounts of 2/10, n/30). The account was paid in 2015 within the discount period by debiting Repairs and Maintenance and crediting cash. Based on estimates made at the date of acquisition, it would cost P50,000 to dismantle the machine at the end of its 9-year useful life. Argelyn's incremental borrowing rate is 9%. Present value factors are presented below: Present value of P1 at 9% for nine periods 0.4604 Present value of annuity due of P1 at 9% for nine periods 6.5348 Present value of ordinary annuity of P1 at 9% for nine perinds 5.9952 The intangibles account at December 31, 2016 consisted of the following: Franchise P500,000 Licensing agreement 216,000 Organization costs 100,000 P816,000 a. A franchise agreement was acquired al the beginning of 2016 for P450,000. Review of the records of Argelyn indicated that P50,000 in continuing franchise fees for 2016 were capitalized as part of the Franchise account. No amortization has been recorded for 2016. A ten-year amortization period is to be used. b. The company's Licensing Agreement account has a balance of P216,000. The original amount was P360,000 and is being amortized on a five-year basis starting in January 2014. As of year-end, amortization has not been recorded. c. The organization costs include the unamortized portion of amounts paid to promoters for services rendered at the inception of the corporation. No amortization has been recorded yet for 2016. The following exceptions were nated for accounts payable and accrued expenses: a. Payment to Abram, Inc., a supplier, amounting to P126,000 was erroneously debited to the account of Abraham, Inc., another supplier. b. The following unpaid vouchers have not been recorded as of year-end: (1) Light, telephone and water bills for December totaling P22,800. (2) Property taxes for the last quarter of 2016, due on the first week of January, 2017, P10,000 (3) Various payroll taxes, P18,000 Mary Abigail Sison, president of the Argelyn Corporation, has a bonus arrangement with the company under which she receives 10% of the net income (after deducting taxes and bonuses) each year. For the current year, no accrual has yet been made for the bonus payable to Ms. Sison. Rent was received from a tenant in December 2016. The amount of P130,000 was recorded as income at that time even though the rental pertains to 2017. The following matters were confirmed with Mr, Yanyan Bagayao, legal counsel of Argelyn Corporation: a. In July 2016, Argelyn was sued for damages to an adjacent property as a result of a machine malfunction. On December 31, 2016, it was estimated that it is probable that Argelyn will have to pay damages amounting ta P75,000. On February 1, 2017, prior to the issuance of the audit report and the corporation's financial statements, the plaintiff agreed to a settlement of P60,000. b. In September 2016, Keyboard Company filed a suit against Argelyn Corporation alleging violations of intellectual property rights. It is seeking payment of damages of P700,000. Argelyn disclaims the charges and Atty. Bagayao is of the opinion that the chance of Argelyn paying any damages is remote. 20. 21: 22. c. In October 2016, Mr. Alger Tangdana, an elderly and grumpy shareholder, brought action against the company seeking P100,000 in damages for physical injury sustained as a result of an accident in the company plant. It is reasonably possible that Mr. Tangdana will be successful, but the amount of damages to be paid, if any, cannot be reasonably estimated. d. In November 2016, Argelyn Corporation was sued by the Municipality of Lingayen, alleging violation of environmental laws. It is highly probable that Argelyn will have to pay an amount between P160,000 and P200,000, buta better estimate is P180,000 as a result of this lawsuit. None of these matters have been given accounting recognition. Starting 2016, Argelyn sells dry goods with a warranty under which customers are covered for the cost of repairs for any defect that becomes apparent within one year from the date of purchase. If only minor defects are detected, for all products sold, repair costs of P100,000 would result. If major defects were detected in all products sold, repair costs of P500,000 would result. The company's experience and future expectations indicate that for the coming year, 60% of the goods sold will have no defects, 30% will have minor defects, and 10% will have major defects. The mortgage on land and building assumed by the company is payable in installments of P500,000 every January 1, starting January 1, 2017. Interest of 20% per annum is payable semi-annually every January 1 and July 1. The bonds payable represented a 9%, P2,000,000 face value bond, which was issued on January 1, 2016 to yield 10%. Argelyn uses the interest method of amortizing bond discount. Interest is payable annually on January 1. No interest accrual nor bond discount amortization was recorded during 2016. The income tax rate is 32%. Assume that there are no reconciling items between book income and taxable income. Ignore tax effects. Review of the subscription agreements and share issuance documents reveal that Argelyn Corporation's ordinary share account includes share premium in the amount of P1,450,000. No reclassification entry has been made. On January 1, 2016 Argelyn issued 200 share options to each of its 10 executive officers. The options vest at the end of a three-year period. On the date of the grant, each share option had a fair value of P150. Argelyn expects that all options will vest. The company did not make any entry related to the options, as there was no cash involved in the transaction. REQUIRED: 1: 2. Prepare the necessary audit adjustments at December 31, 2016. Close the Dividends Declared account Compute for the adjusted balances of each account presented in the unadjusted trial balance. You may add more account titles as deemed necessary in order to better reflect the adjusted balances of the company. -end

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Accounting Questions!