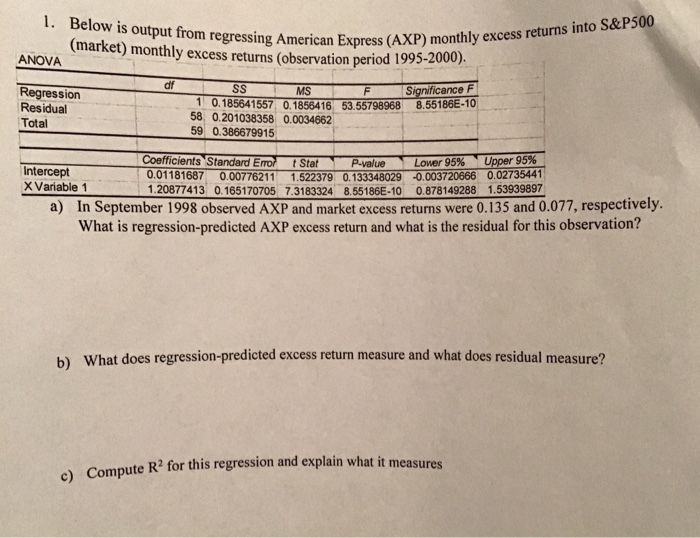

Question: B) and C) only please Below is output from regressing American Express(AXP) monthly excess (market) monthly excess returns (observation period 1995-2000), 1. ANOVA df Regression

Below is output from regressing American Express(AXP) monthly excess (market) monthly excess returns (observation period 1995-2000), 1. ANOVA df Regression Residual Total Significance F MS 10.185641557, 0.1856416 53.55798968 8.55186E-10 58 0.201038358 0.0034662 59 0.386679915 coefficients StandardEm tStat -P-value- Lower95% Upper 95% 0.01181687 0.00776211 1.522379 0.133348029 0.003720666 0.02735441 1.20877413 0.165170705 7.3183324 8,55186E-10 0.878149288 1.53939897 Intercept X Variable1 a) In September 1998 observed AXP and market excess returns were 0.135 and 0.077, respectively. What is regression-predicted AXP excess return and what is the residual for this observation? What does regression-predicted excess return measure and what does residual measure? b) ) Compute R? for this regression and explain what it measures c) pu

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts