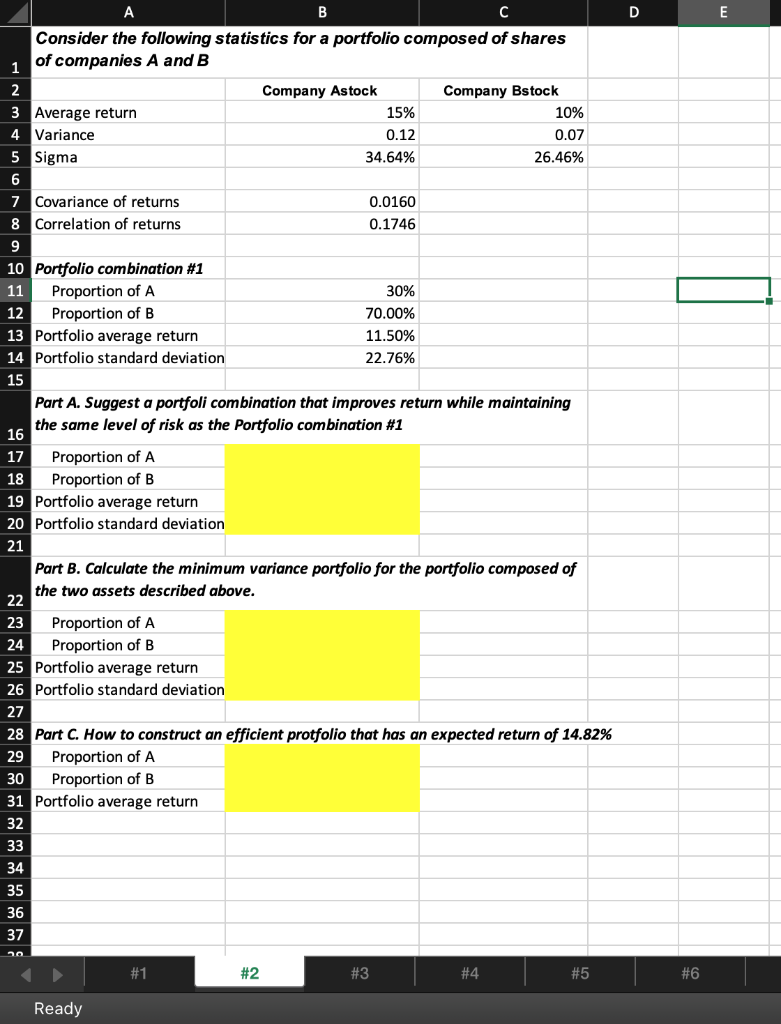

Question: B C Consider the following statistics for a portfolio composed of shares 1 of companies A and B 2 Company Astock Company Bstock 3 Average

B C Consider the following statistics for a portfolio composed of shares 1 of companies A and B 2 Company Astock Company Bstock 3 Average return 15% 10% 4 Variance 0.12 0.07 5 Sigma 34.64% 26.46% 6 7 Covariance of returns 0.0160 8 Correlation of returns 0.1746 9 10 Portfolio combination #1 11 Proportion of A 30% 12 Proportion of B 70.00% 13 Portfolio average return 11.50% 14 Portfolio standard deviation 22.76% 15 Part A. Suggest a portfoli combination that improves return while maintaining the same level of risk as the Portfolio combination #1 16 17 Proportion of A 18 Proportion of B 19 Portfolio average return 20 Portfolio standard deviation 21 Part B. Calculate the minimum variance portfolio for the portfolio composed of the two assets described above. 22 23 Proportion of A 24 Proportion of B 25 Portfolio average return 26 Portfolio standard deviation 27 28 Part C. How to construct an efficient protfolio that has an expected return of 14.82% 29 Proportion of A 30 Proportion of B 31 Portfolio average return 32 33 34 35 36 37 20 #1 #3 #4 #5 Ready #2 D #6 E

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts