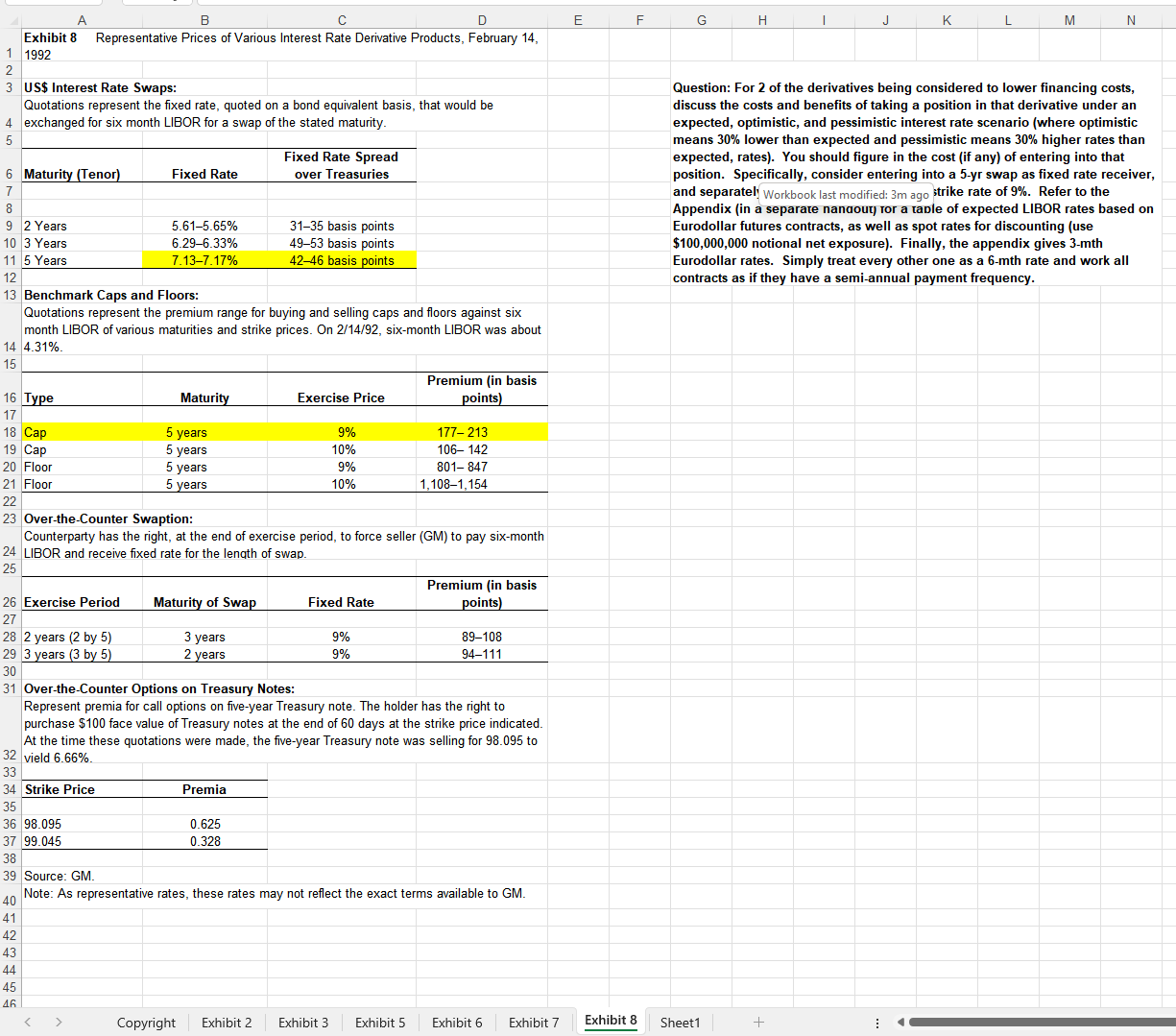

Question: B C D E F G H K M Exhibit 8 Representative Prices of Various Interest Rate Derivative Products, February 14, 1992 3 US$ Interest

B C D E F G H K M Exhibit 8 Representative Prices of Various Interest Rate Derivative Products, February 14, 1992 3 US$ Interest Rate Swaps: Question: For 2 of the derivatives being considered to lower financing costs, Quotations represent the fixed rate, quoted on a bond equivalent basis, that would be discuss the costs and benefits of taking a position in that derivative under an exchanged for six month LIBOR for a swap of the stated maturity expected, optimistic, and pessimistic interest rate scenario (where optimistic means 30% lower than expected and pessimistic means 30% higher rates than Fixed Rate Spread expected, rates). You should figure in the cost (if any) of entering into that 6 Maturity (Tenor) Fixed Rate over Treasuries position. Specifically, consider entering into a 5-yr swap as fixed rate receiver, 7 and separatel: Workbook last modified: 3m ago strike rate of 9%. Refer to the 8 Appendix (in a separate nanaout for a table of expected LIBOR rates based on 9 2 Years 5.61-5.65% 31-35 basis points Eurodollar futures contracts, as well as spot rates for discounting (use 10 3 Years 6.29-6.33% 49-53 basis points $100,000,000 notional net exposure). Finally, the appendix gives 3-mth 11 5 Years 7.13-7 17% 42-46 basis points Eurodollar rates. Simply treat every other one as a 6-mth rate and work all 12 contracts as if they have a semi-annual payment frequency. 13 Benchmark Caps and Floors: Quotations represent the premium range for buying and selling caps and floors against six month LIBOR of various maturities and strike prices. On 2/14/92, six-month LIBOR was about 14 4.31%. 15 Premium (in basis 16 Type Maturity Exercise Price points) 17 18 Cap 5 years 9% 177-213 19 Ca years 10% 106- 142 20 Floor years 9% 801- 847 21 Floor 5 years 0% 1, 108-1,154 23 Over-the-Counter Swaption: Counterparty has the right, at the end of exercise period, to force seller (GM) to pay six-month 24 LIBOR and receive fixed rate for the length of swap 25 Premium (in basis 26 Exercise Period Maturity of Swap Fixed Rate points) 28 2 years (2 by 5) 3 years 9% 89-108 29 3 years (3 by 5) 2 years 9% 94-111 30 31 Over-the-Counter Options on Treasury Notes: Represent premia for call options on five-year Treasury note. The holder has the right to purchase $100 face value of Treasury notes at the end of 60 days at the strike price indicated. At the time these quotations were made, the five-year Treasury note was selling for 98.095 to 32 vield 6.66% Strike Price Premia 36 98.095 0.625 37 99.045 0.328 38 39 Source: GM. Note: As representative rates, these rates may not reflect the exact terms available to GM. 41 42 43 44 45 AG Copyright Exhibit 2 Exhibit 3 Exhibit 5 Exhibit 6 Exhibit 7 Exhibit 8 Sheet1 +

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Finance Questions!