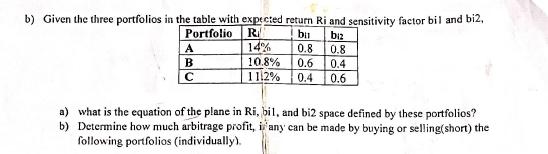

Question: b) Given the three portfolios in the table with expected return Ri and sensitivity factor bil and bi2, Portfolio A B Ri bil biz

b) Given the three portfolios in the table with expected return Ri and sensitivity factor bil and bi2, Portfolio A B Ri bil biz 14% 0.8 0.8 10.8% 0.6 0.4 C 1112% 0.4 0.6 a) what is the equation of the plane in Ri, bil, and bi2 space defined by these portfolios? b) Determine how much arbitrage profit, i'any can be made by buying or selling(short) the following portfolios (individually).

Step by Step Solution

There are 3 Steps involved in it

a The equation of the plane in Ri bil and bi2 space can be represented as R a b1b2 c1b1 c2b2 where a ... View full answer

Get step-by-step solutions from verified subject matter experts