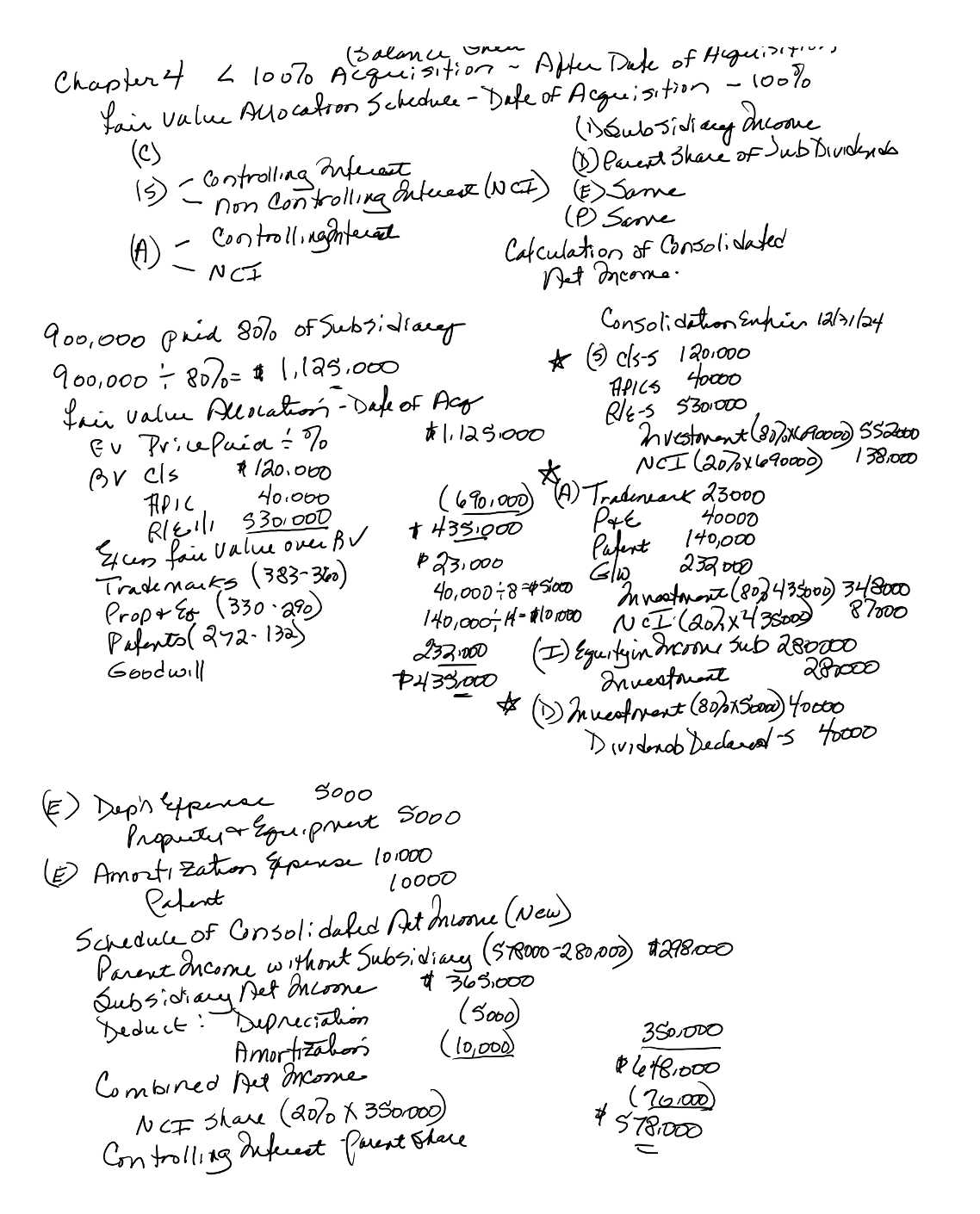

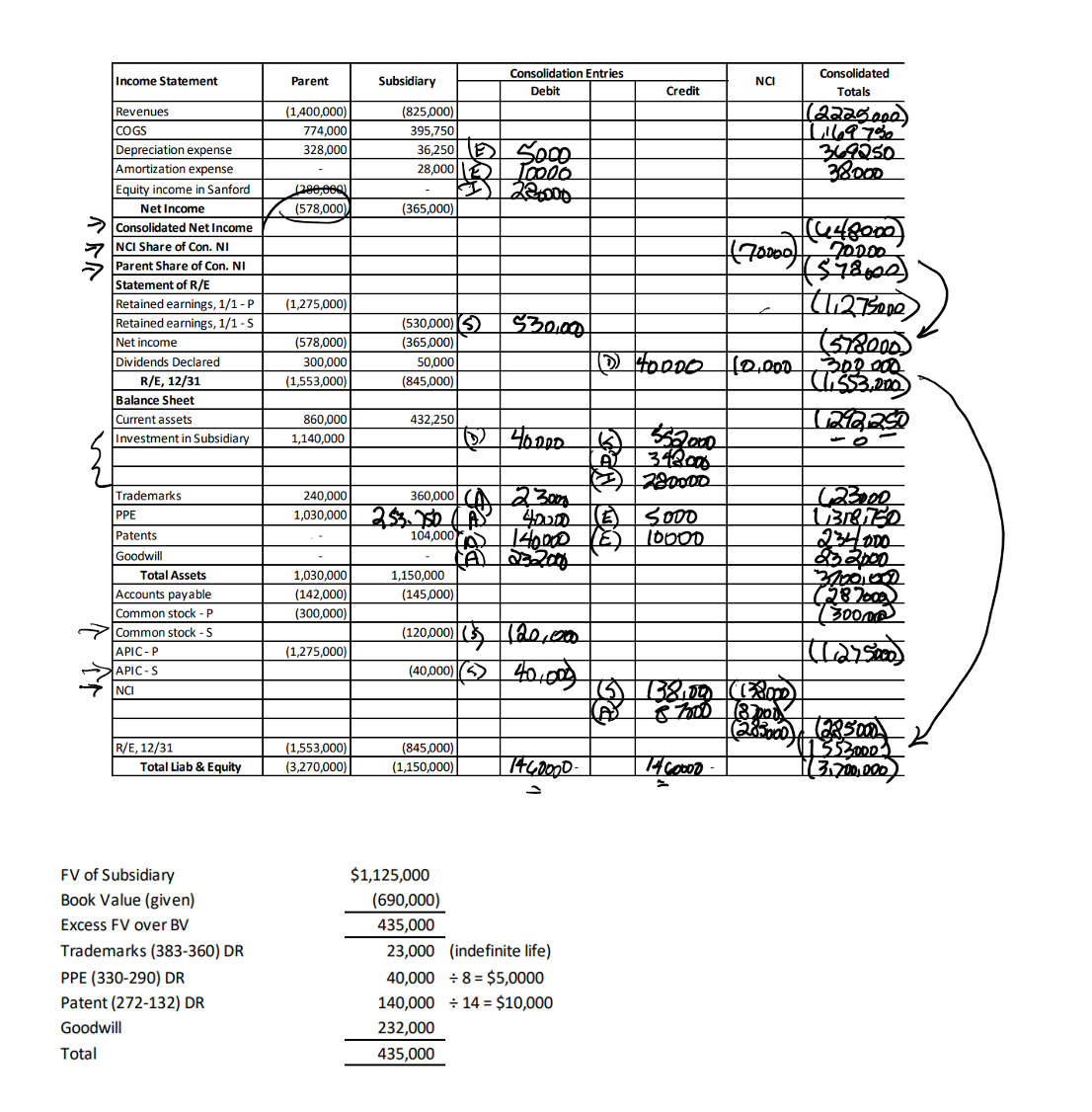

Question: ( Balance onen Chapter 4 6 10070 Acquisition - After Date of Hiquisitive, fair value Allocation Schedule - Date of Acquisition - 100%% (C) (

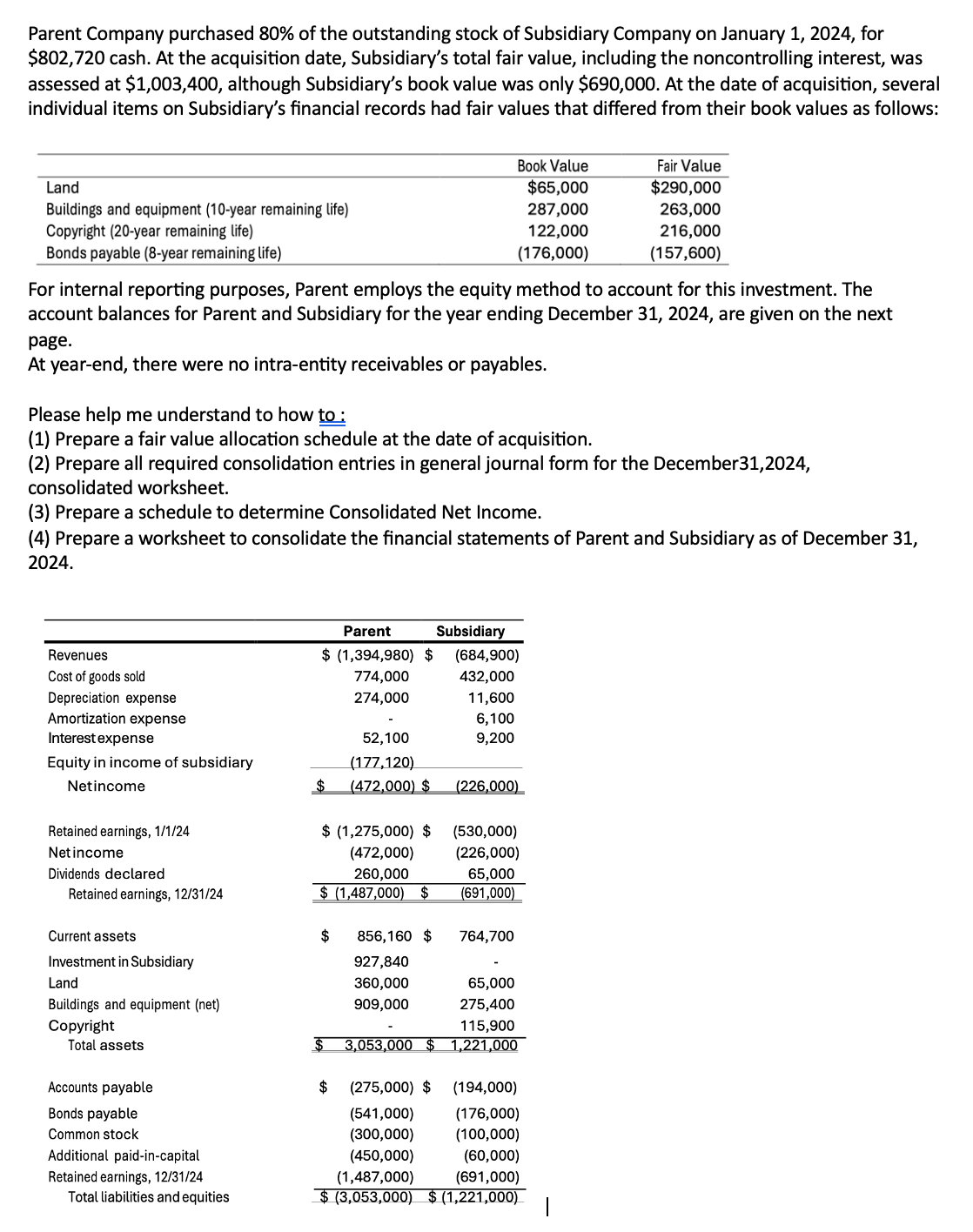

( Balance onen Chapter 4 6 10070 Acquisition - After Date of Hiquisitive, fair value Allocation Schedule - Date of Acquisition - 100%% (C) ( ") Subsidiary Oncoone 15 ) - controlling antecant (>) Parent Share OF Jub Dividend non Controlling interest ( NOT ) ( E ) Same (A ) - Controllingentered ( P) Same NCI Calculation of Consolidated net income . 900,000 paid 80% of Subsidiary Consolidation Entries 12/3,1/24 900,000 - 8070= $ 1,125,000 * (5) c/5- 5 1201000 fair value Allocation - Date of Acy APICS 40000 RE- 5 5301000 EV PricePaid : % * 1, 12 51000 Investorent ( 80)0*( 1900DO) 552060 BV cls $ 120.060 NCI ( 2070 X 690000) 138,000 APIC 401000 RIEL/1 5301000 (690,000) ( A) Trademark 23000 yun fair Value over BV + 435.900 40000 Putent 140,000 Trademarks ( 383 - 340) $ 23,000 232 010 Prop+ Ex (330 . 290) 40,000 - 8 =$ 5iod investment (807 435000) 34/8000 Patents ( 272- 132) 140,000;14- $10,080 NCI ( 202x 4 35000) 87000 Good will 232:060 (I) Equity in Mcrow Sub 280000 1435,000 287000 $ (D) Mucotrent ( 80 /X 5600) 40 060 Dividenob Declared-5 40000 Sooo (E) Amortization Expense 101000 Patent 10000 Schedule of Consolidated Net income ( New) Parent acome without Subsidiary (578000- 280,000) $298000 JSubsidiary Net Oncoone # 365,000 Deduct : Depreciation Amortization ( 10,000) 35010DO Combined Net income 1 4181000 NCF Share (2070 X 350rooo) ( 761000 ) Controlling Anferent Parent Slace $ 5781000Income Statement Parent Subsidiary Consolidation Entries NCI Consolidated Debit Credit Totals Revenues (1,400,000 (825,000) (2220200) COGS 774,000 395,750 1 169 790 Depreciation expense 28,000 36,250 ) 349250 Amortization expense 28,000 E CO20 38000 Equity income in Sanford (280,060) I 23:000 Net Income (578,000 (365,000) Consolidated Net Income NCI Share of Con. NI Parent Share of Con. NI ($ 78600) Statement of R/E Retained earnings, 1/1 - P (1,275,000) Retained earnings, 1/1 - S (530,000) 5 30.0 Net income 578,000) (365,000) (578000) Dividends Declared 300,000 50,000 1D) FORDO 10.000 R/E, 12/31 (1,553,000) 845,000) (553,200 Balance Sheet Current assets 860,000 432,250 14212 250 Investment in Subsidiary ,140,000 562000 - O 280000 Trademark 240,000 360,000 2 3028 PPE 1,030,000 (Soot Patents 104,00040DD ( E) 10000 234/ 200 Goodwill Total Assets ,030,000 ,150,000 Accounts payable (142,000) (145,000) (287003) Common stock - P (300,000) 730010 Common stock - (120,000) (3 20.20 APIC - (1,275,00 APIC - S 40,000) 3> 40+009 R/E, 12/31 (1,553,000) (845,000) 15 53000 Total Liab & Equity (3,270,000) (1,150,000) 7+4DODD- 13 700,200 FV of Subsidiary $1,125,000 Book Value (given) (690,000) Excess FV over BV 435,000 Trademarks (383-360) DR 23,000 (indefinite life) PPE (330-290) DR 40,000 : 8 = $5,0000 Patent (272-132) DR 140,000 : 14 = $10,000 Goodwill 232,000 Total 435,000Parent Company purchased 80% of the outstanding stock of Subsidiary Company on January 1, 2024, for $802,720 cash. At the acquisition date, Subsidiary's total fair value, including the noncontrolling interest, was assessed at $1,003,400, although Subsidiary's book value was only $690,000. At the date of acquisition, several individual items on Subsidiary's financial records had fair values that differed from their book values as follows: Book Value Fair Value Land $65,000 $290,000 Buildings and equipment (10-year remaining life) 287,000 263,000 Copyright (20-year remaining life) 122,000 216,000 Bonds payable (8-year remaining life) (176,000) (157,600) For internal reporting purposes, Parent employs the equity method to account for this investment. The account balances for Parent and Subsidiary for the year ending December 31, 2024, are given on the next page. At year-end, there were no intra-entity receivables or payables. Please help me understand to how to: (1) Prepare a fair value allocation schedule at the date of acquisition. (2) Prepare all required consolidation entries in general journal form for the December31,2024, consolidated worksheet. (3) Prepare a schedule to determine Consolidated Net Income. (4) Prepare a worksheet to consolidate the financial statements of Parent and Subsidiary as of December 31, 2024. Parent Subsidiary Revenues $ (1,394,980) $ (684,900) Cost of goods sold 774,000 432,000 Depreciation expense 274,000 11,600 Amortization expense - 6,100 Interestexpense 52,100 9,200 Equity in income of subsidiary (177,120) Netincome $ (472,000) $ (226,000) Retained earnings, 1/1/24 $ (1,275,000) $ (530,000) Netincome (472,000) (226,000) Dividends declared 260,000 65,000 Retained eamings, 12/31/24 \" (1,487,000) $ (691,000) Current assets $ 856,160 $ 764,700 Investment in Subsidiary 927,840 - Land 360,000 65,000 Buildings and equipment (net) 909,000 275,400 Copyright - 115,900 Total assets Accounts payable $ (275,000) $ (194,000) Bonds payable (541,000) (176,000) Common stock (300,000) (100,000) Additional paid-in-capital (450,000) (60,000) Retained earnings, 12/31/24 (1,487,000) (691,000) Total liabilities and equities $ (3,053,000) _$ (1,221,000) |

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Accounting Questions!