Question: What I came up with: What am I doing wrong?? INSTRUCTIONS: (1) Prepare a fair value allocation schedule at the date of acquisition. (2) Prepare

What I came up with:

What am I doing wrong??

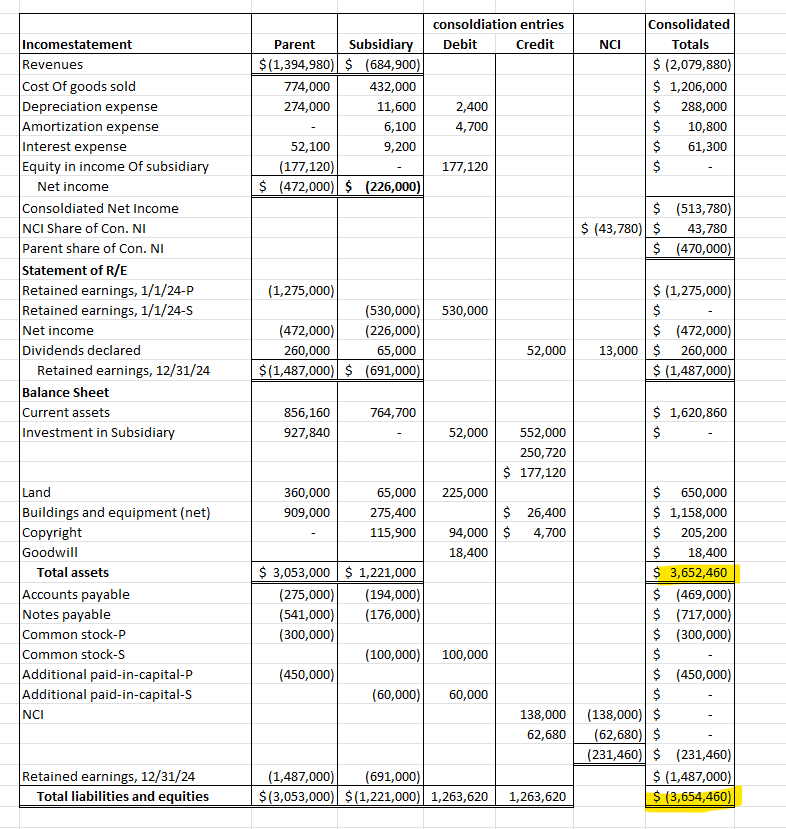

INSTRUCTIONS: (1) Prepare a fair value allocation schedule at the date of acquisition. (2) Prepare all required consolidation entries in general journal form for the December 31, 2024, consolidated worksheet. (3) Prepare a schedule to determine Consolidated Net Income. (4) Prepare a worksheet to consolidate the financial statements of Parent and Subsidiary as of December 31, 2024. \begin{tabular}{|c|c|c|c|c|} \hline \multicolumn{5}{|l|}{ Consolidated Net Income } \\ \hline Parent Net Income without sub & & & $ & 294,880 \\ \hline Sub net income & $ & 226,000 & & \\ \hline \multicolumn{5}{|l|}{ Deduct: } \\ \hline Depreciation on building \& equip & $ & (2,400) & & \\ \hline Amortizaiton copyright & $ & (4,700) & & \\ \hline Sub net income & & & $ & 218,900 \\ \hline Consoldiated net income & & & $ & 513,780 \\ \hline NCl share of consolidated & & & $ & 43,780 \\ \hline Parent share of consoldiated & & & $ & 470,000 \\ \hline \end{tabular} \begin{tabular}{|c|c|c|c|c|c|c|} \hline \multirow[b]{2}{*}{ Incomestatement } & \multirow[b]{2}{*}{ Parent } & \multirow[b]{2}{*}{ Subsidiary } & \multicolumn{2}{|c|}{ consoldiation entries } & \multirow[b]{2}{*}{NCl} & \multirow{2}{*}{ConsolidatedTotals} \\ \hline & & & Debit & Credit & & \\ \hline Revenues & $(1,394,980) & $(684,900) & & & & $(2,079,880) \\ \hline Cost Of goods sold & 774,000 & 432,000 & & & & $1,206,000 \\ \hline Depreciation expense & 274,000 & 11,600 & 2,400 & & & 288,000 \\ \hline Amortization expense & - & 6,100 & 4,700 & & & 10,800 \\ \hline Interest expense & 52,100 & 9,200 & & & & 61,300 \\ \hline Equity in income of subsidiary & (177,120) & - & 177,120 & & & $ \\ \hline Net income & $(472,000) & $(226,000) & & & & \\ \hline Consoldiated Net Income & & & & & & $(513,780) \\ \hline NCl Share of Con. NI & & & & & $(43,780) & 43,780 \\ \hline Parent share of Con. NI & & & & & & $(470,000) \\ \hline \multicolumn{7}{|l|}{ Statement of R/E } \\ \hline Retained earnings, 1/1/24P & (1,275,000) & & & & & $(1,275,000) \\ \hline Retained earnings, 1/1/24S & & (530,000) & 530,000 & & & $ \\ \hline Net income & (472,000) & (226,000) & & & & $(472,000) \\ \hline Dividends declared & 260,000 & 65,000 & & 52,000 & 13,000 & $260,000 \\ \hline Retained earnings, 12/31/24 & $(1,487,000) & $(691,000) & & & & $(1,487,000) \\ \hline \multicolumn{7}{|l|}{ Balance Sheet } \\ \hline Current assets & 856,160 & 764,700 & & & & $1,620,860 \\ \hline \multirow[t]{3}{*}{ Investment in Subsidiary } & 927,840 & - & 52,000 & 552,000 & & $ \\ \hline & & & & 250,720 & & \\ \hline & & & & $177,120 & & \\ \hline Land & 360,000 & 65,000 & 225,000 & & & $650,000 \\ \hline Buildings and equipment (net) & 909,000 & 275,400 & & $26,400 & & $1,158,000 \\ \hline Copyright & - & 115,900 & 94,000 & 4,700 & & $205,200 \\ \hline Goodwill & & & 18,400 & & & 18,400 \\ \hline Total assets & $3,053,000 & $1,221,000 & & & & $3,652,460 \\ \hline Accounts payable & (275,000) & (194,000) & & & & $(469,000) \\ \hline Notes payable & (541,000) & (176,000) & & & & $(717,000) \\ \hline Common stock-P & (300,000) & & & & & $(300,000) \\ \hline Common stock-S & & (100,000) & 100,000 & & & $ \\ \hline Additional paid-in-capital-P & (450,000) & & & & & $(450,000) \\ \hline Additional paid-in-capital-S & & (60,000) & 60,000 & & & $ \\ \hline \multirow[t]{3}{*}{NCl} & & & & 138,000 & (138,000) & $ \\ \hline & & & & 62,680 & (62,680) & $ \\ \hline & & & & & (231,460) & $(231,460) \\ \hline Retained earnings, 12/31/24 & (1,487,000) & (691,000) & & & & $(1,487,000) \\ \hline Total liabilities and equities & $(3,053,000) & $(1,221,000) & 1,263,620 & 1,263,620 & & $(3,654,460) \\ \hline \end{tabular} Parent Company purchased 80% of the outstanding stock of Subsidiary Company on January 1,2024 , for $802,720 cash. At the acquisition date, Subsidiary's total fair value, including the noncontrolling interest, was assessed at $1,003,400, although Subsidiary's book value was only $690,000. At the date of acquisition, several individual items on Subsidiary's financial records had fair values that differed from their book values as follows: For internal reporting purposes, Parent employs the equity method to account for this investment. The account balances for Parent and Subsidiary for the year ending December 31,2024, are given on the next page. At year-end, there were no intra-entity receivables or payables. INSTRUCTIONS: (1) Prepare a fair value allocation schedule at the date of acquisition. (2) Prepare all required consolidation entries in general journal form for the December 31, 2024, consolidated worksheet. (3) Prepare a schedule to determine Consolidated Net Income. (4) Prepare a worksheet to consolidate the financial statements of Parent and Subsidiary as of December 31, 2024. \begin{tabular}{|c|c|c|c|c|} \hline \multicolumn{5}{|l|}{ Consolidated Net Income } \\ \hline Parent Net Income without sub & & & $ & 294,880 \\ \hline Sub net income & $ & 226,000 & & \\ \hline \multicolumn{5}{|l|}{ Deduct: } \\ \hline Depreciation on building \& equip & $ & (2,400) & & \\ \hline Amortizaiton copyright & $ & (4,700) & & \\ \hline Sub net income & & & $ & 218,900 \\ \hline Consoldiated net income & & & $ & 513,780 \\ \hline NCl share of consolidated & & & $ & 43,780 \\ \hline Parent share of consoldiated & & & $ & 470,000 \\ \hline \end{tabular} \begin{tabular}{|c|c|c|c|c|c|c|} \hline \multirow[b]{2}{*}{ Incomestatement } & \multirow[b]{2}{*}{ Parent } & \multirow[b]{2}{*}{ Subsidiary } & \multicolumn{2}{|c|}{ consoldiation entries } & \multirow[b]{2}{*}{NCl} & \multirow{2}{*}{ConsolidatedTotals} \\ \hline & & & Debit & Credit & & \\ \hline Revenues & $(1,394,980) & $(684,900) & & & & $(2,079,880) \\ \hline Cost Of goods sold & 774,000 & 432,000 & & & & $1,206,000 \\ \hline Depreciation expense & 274,000 & 11,600 & 2,400 & & & 288,000 \\ \hline Amortization expense & - & 6,100 & 4,700 & & & 10,800 \\ \hline Interest expense & 52,100 & 9,200 & & & & 61,300 \\ \hline Equity in income of subsidiary & (177,120) & - & 177,120 & & & $ \\ \hline Net income & $(472,000) & $(226,000) & & & & \\ \hline Consoldiated Net Income & & & & & & $(513,780) \\ \hline NCl Share of Con. NI & & & & & $(43,780) & 43,780 \\ \hline Parent share of Con. NI & & & & & & $(470,000) \\ \hline \multicolumn{7}{|l|}{ Statement of R/E } \\ \hline Retained earnings, 1/1/24P & (1,275,000) & & & & & $(1,275,000) \\ \hline Retained earnings, 1/1/24S & & (530,000) & 530,000 & & & $ \\ \hline Net income & (472,000) & (226,000) & & & & $(472,000) \\ \hline Dividends declared & 260,000 & 65,000 & & 52,000 & 13,000 & $260,000 \\ \hline Retained earnings, 12/31/24 & $(1,487,000) & $(691,000) & & & & $(1,487,000) \\ \hline \multicolumn{7}{|l|}{ Balance Sheet } \\ \hline Current assets & 856,160 & 764,700 & & & & $1,620,860 \\ \hline \multirow[t]{3}{*}{ Investment in Subsidiary } & 927,840 & - & 52,000 & 552,000 & & $ \\ \hline & & & & 250,720 & & \\ \hline & & & & $177,120 & & \\ \hline Land & 360,000 & 65,000 & 225,000 & & & $650,000 \\ \hline Buildings and equipment (net) & 909,000 & 275,400 & & $26,400 & & $1,158,000 \\ \hline Copyright & - & 115,900 & 94,000 & 4,700 & & $205,200 \\ \hline Goodwill & & & 18,400 & & & 18,400 \\ \hline Total assets & $3,053,000 & $1,221,000 & & & & $3,652,460 \\ \hline Accounts payable & (275,000) & (194,000) & & & & $(469,000) \\ \hline Notes payable & (541,000) & (176,000) & & & & $(717,000) \\ \hline Common stock-P & (300,000) & & & & & $(300,000) \\ \hline Common stock-S & & (100,000) & 100,000 & & & $ \\ \hline Additional paid-in-capital-P & (450,000) & & & & & $(450,000) \\ \hline Additional paid-in-capital-S & & (60,000) & 60,000 & & & $ \\ \hline \multirow[t]{3}{*}{NCl} & & & & 138,000 & (138,000) & $ \\ \hline & & & & 62,680 & (62,680) & $ \\ \hline & & & & & (231,460) & $(231,460) \\ \hline Retained earnings, 12/31/24 & (1,487,000) & (691,000) & & & & $(1,487,000) \\ \hline Total liabilities and equities & $(3,053,000) & $(1,221,000) & 1,263,620 & 1,263,620 & & $(3,654,460) \\ \hline \end{tabular} Parent Company purchased 80% of the outstanding stock of Subsidiary Company on January 1,2024 , for $802,720 cash. At the acquisition date, Subsidiary's total fair value, including the noncontrolling interest, was assessed at $1,003,400, although Subsidiary's book value was only $690,000. At the date of acquisition, several individual items on Subsidiary's financial records had fair values that differed from their book values as follows: For internal reporting purposes, Parent employs the equity method to account for this investment. The account balances for Parent and Subsidiary for the year ending December 31,2024, are given on the next page. At year-end, there were no intra-entity receivables or payables

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts