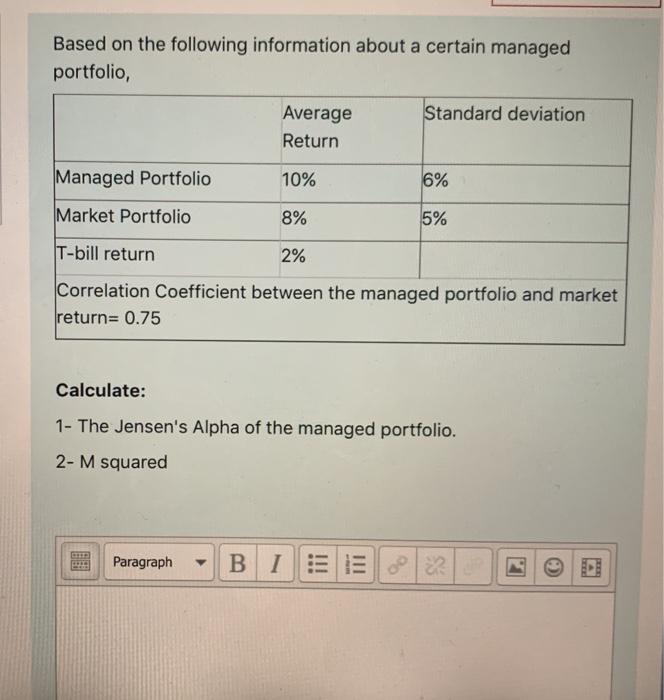

Question: Based on the following information about a certain managed portfolio, Standard deviation Average Return Managed Portfolio 10% 6% Market Portfolio 8% 5% T-bill return 2%

Based on the following information about a certain managed portfolio, Standard deviation Average Return Managed Portfolio 10% 6% Market Portfolio 8% 5% T-bill return 2% Correlation coefficient between the managed portfolio and market return= 0.75 Calculate: 1- The Jensen's Alpha of the managed portfolio. 2- M squared Paragraph

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock