Question: Based on the primer (Exhibit 1), the idea was to use calls on the S&P 500 Index. The payoff at maturity was based on the

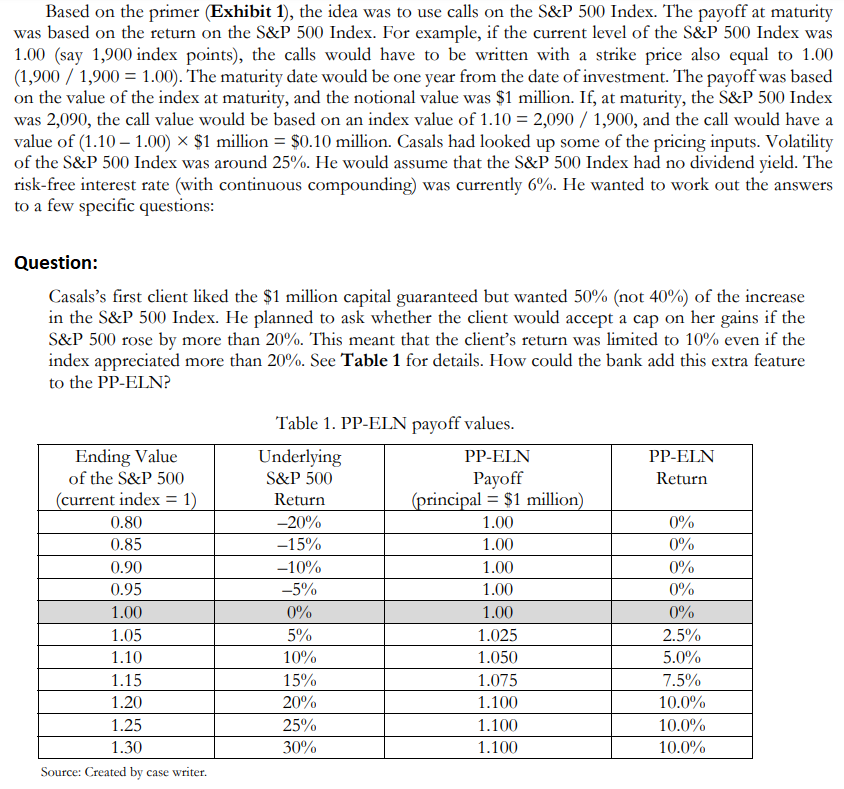

Based on the primer (Exhibit 1), the idea was to use calls on the S&P 500 Index. The payoff at maturity was based on the return on the S&P 500 Index. For example, if the current level of the S&P 500 Index was 1.00 (say 1,900 index points), the calls would have to be written with a strike price also equal to 1.00 (1,900 / 1,900 = 1.00). The maturity date would be one year from the date of investment. The payoff was based on the value of the index at maturity, and the notional value was $1 million. If, at maturity, the S&P 500 Index was 2,090, the call value would be based on an index value of 1.10 = 2,090 / 1,900, and the call would have a value of (1.10 1.00)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts