Question: Question one Lafarge is French industrial company specialising in three major products: cement, construction aggregates, and concrete. Lafarge Zambia operates 2 integrated cement plants

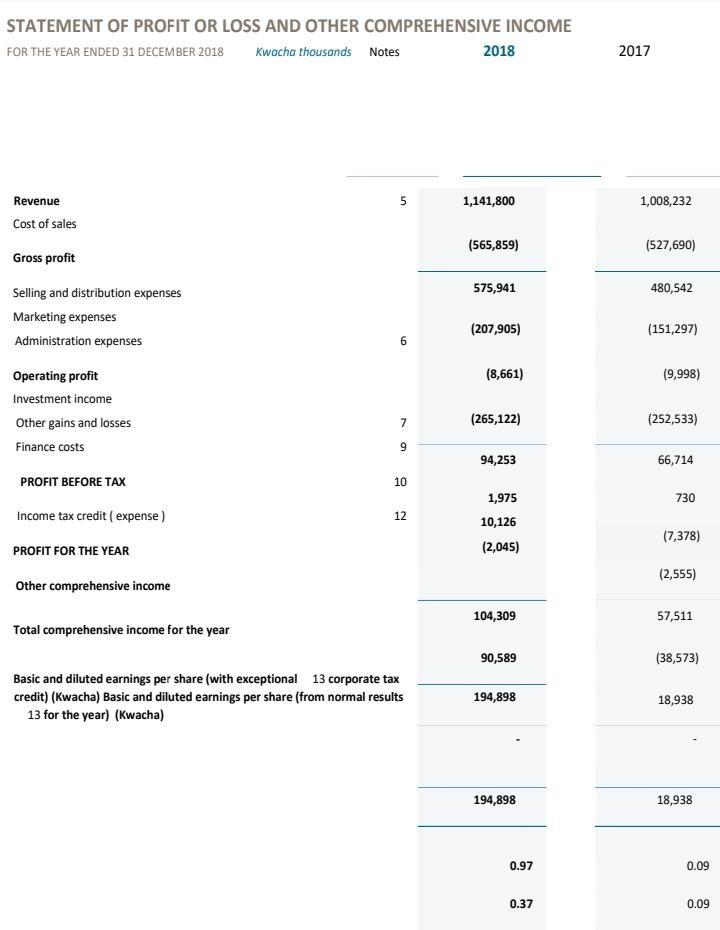

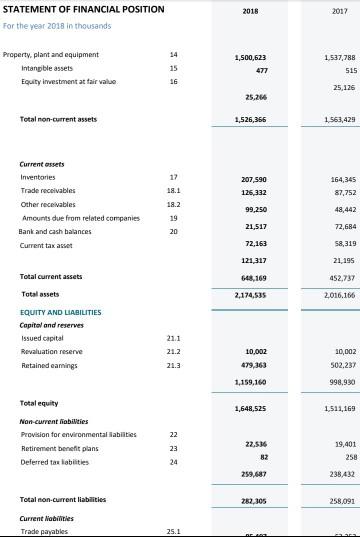

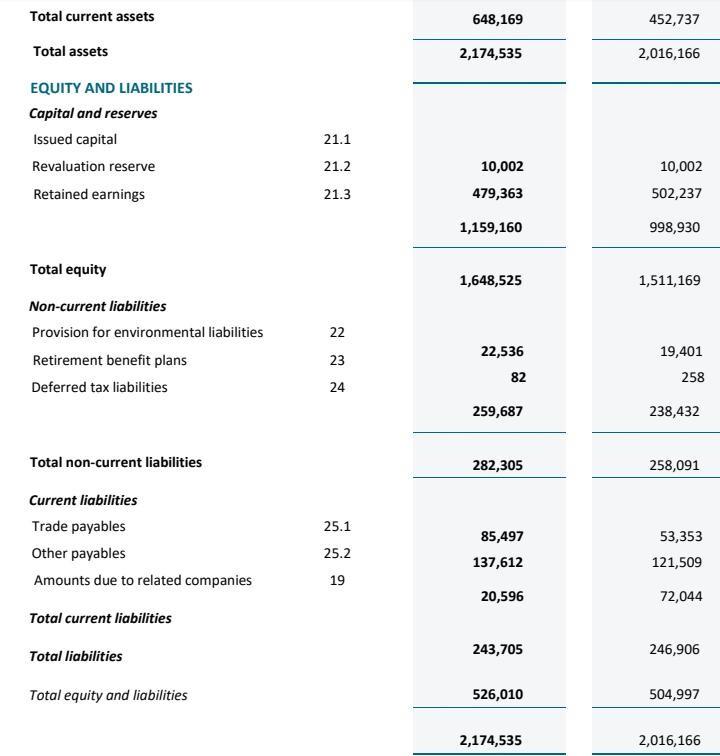

Question one Lafarge is French industrial company specialising in three major products: cement, construction aggregates, and concrete. Lafarge Zambia operates 2 integrated cement plants (situated in Ndola and Lusaka) with a total production capacity of 1.4 million tonnes per annum. The 440 direct employees supported by several hundred more contracted employees continue to add value to the country's raw materials that lead to the production of 6 innovative products including Mphamvu, the flagship product brand, Powerplus for heavy industrial construction, Supaset, the preferred choice for block makers, RoadCem for soil stabilization during road construction, Powercrete, designed for applications in the mining industry, including back filling, rock bolting, stopping and shotcreting, and WallCrete, masonry with superior workability, ideal for bricklaying, plasterwork, floor screed and pointing, whether for large construction projects or individual homebuilders. With a firm focus on innovation and optimising operations, the Company continues to promote value addition and continually create jobs directly and indirectly through forward and backward linkages within and outside the sector. The Company supplies products by road and rail to the entire country, as well as the regional market, primarily to the Tanzania, Burundi Democratic Republic of Congo (DRC), Malawi, Namibia and Zimbabwe. In addition the Aggregates business continues to produce high quality fine, course and dense grade aggregates products, suitable for a wide variety of construction applications, from concrete to road and highway surfaces, railway ballast and fill material. Below are the financial statement for the year 2018 which the chief financial officer is about to submit for audit. STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME FOR THE YEAR ENDED 31 DECEMBER 2018 Kwacha thousands Notes 2018 2017 Revenue 1,141,800 1,008,232 Cost of sales (565,859) (527,690) Gross profit Selling and distribution expenses 575,941 480,542 Marketing expenses (207,905) (151,297) Administration expenses Operating profit (8,661) (9,998) Investment income Other gains and losses 7. (265,122) (252,533) Finance costs 9. 94,253 66,714 PROFIT BEFORE TAx 10 1,975 730 Income tax credit ( expense ) 12 10,126 (7,378) PROFIT FOR THE YEAR (2,045) (2,555) Other comprehensive income 104,309 57,511 Total comprehensive income for the year 90,589 (38,573) Basic and diluted earnings per share (with exceptional 13 corporate tax credit) (Kwacha) Basic and diluted earnings per share (from normal results 13 for the year) (Kwacha) 194,898 18,938 194,898 18,938 0.97 0.09 0.37 0.09 STATEMENT OF FINANCIAL POSITION 2018 2017 For the year 2018 in thousands Property, plant and equipment 14 1,500,623 1,537,788 Intangible assets 15 477 515 Equity investment at fair value 16 25,126 25,26 Total non-current assets 1,526,366 1,561,429 Current essets Inventories 17 207,590 164,345 Trade receivables 18.1 126,332 87,752 Other receivables 18.2 99,250 48,442 Amounts due from releted companies 19 21,517 72,684 Bank and cash balances 20 Current tax asset 72,163 58,319 121,317 21,195 Total current assets 648,169 452,737 Total assets 2,174,535 2,016.166 EQUITY AND LIABILITIES Capital and reserves Issued capital 21.1 Revaluation reserve 21.2 10,002 10,002 Retained eamings 479,363 502,237 21.3 1,159,160 998,930 Total equity 1,648,525 1,511,169 Non-current liabilties Provision for environmental labities 22 22.536 19,401 Retirement benefit plans 23 82 258 Deferred tax labities 24 259,687 238,432 Total non-curent liabilities 282,305 258.091 Current Nabilities Trade payables 25.1 Total current assets 648,169 452,737 Total assets 2,174,535 2,016,166 EQUITY AND LIABILITIES Capital and reserves Issued capital 21.1 Revaluation reserve 21.2 10,002 10,002 Retained earnings 21.3 479,363 502,237 1,159,160 998,930 Total equity 1,648,525 1,511,169 Non-current liabilities Provision for environmental liabilities 22 22,536 19,401 Retirement benefit plans 23 82 258 Deferred tax liabilities 24 259,687 238,432 Total non-current liabilities 282,305 258,091 Current liabilities Trade payables 25.1 85,497 53,353 Other payables 25.2 137,612 121,509 Amounts due to related companies 19 20,596 72,044 Total current liabilities 243,705 246,906 Total liabilities Total equity and liabilities 526,010 504,997 2,174,535 2,016,166 Before submitting the reports for audit the CFO has notice that the following information relating to the construction project of building the bridge which was awarded to Lafarge by the Road Development Agency (RDA) which commenced in 2017 has been omitted in the financial records. The initial price agreed in the contract is K90, 000,000. Lafarge's initial estimate of contract costs is K80, 000,000. It will take 3 years to build the bridge. By the end of year 2017, Lafarge's estimate of contract costs had increased to K80, 500,000.In year 2018, RDA approved a variation resulting in an increase in contract revenue of K2, 000,000 and estimated additional contract costs of K1, 500,000. At the end 2018, costs incurred included K1000, 000 for standard materials stored at the site to be used in the year 2019 to complete the project.Lafarge determines the stage of completion of the contract by using the input method. A summary of the financial data during the construction period is as follows 2017 2018 2019 K,000 Initial amount of revenue agreed 90,000 Contract Cost incured in the year 20,930 000 90,000 .000 90,000 40,750 20,320 The CFO has requested that you deal with this issue so that correct financial statements are submitted for audit. Required a) Citing relevant accounting standard explain what type of error has been made by Lafarge and explain how this error will be accounted for in the books (5 marks) b) Prepare all the required journal entries to update the records of Lafarge (show all your working) 15 marks c) Prepare a new Income statement and the statement of financial position after recording the above omitted transaction.(10 marks) d) Discuss the effect that this omission had on the profit before tax for 2018 and the impact that it would have had to the users of financial statement.(10 marks)

Step by Step Solution

3.40 Rating (153 Votes )

There are 3 Steps involved in it

Small plant mediumsized plant and no plant are the three decision alternatives and good market average market and bad market are the three states of n... View full answer

Get step-by-step solutions from verified subject matter experts