Question: Below is an extract from Amazon's 2017 annual report. What is the firm's GAAP effective tax rate? Why does the rate differ from the top

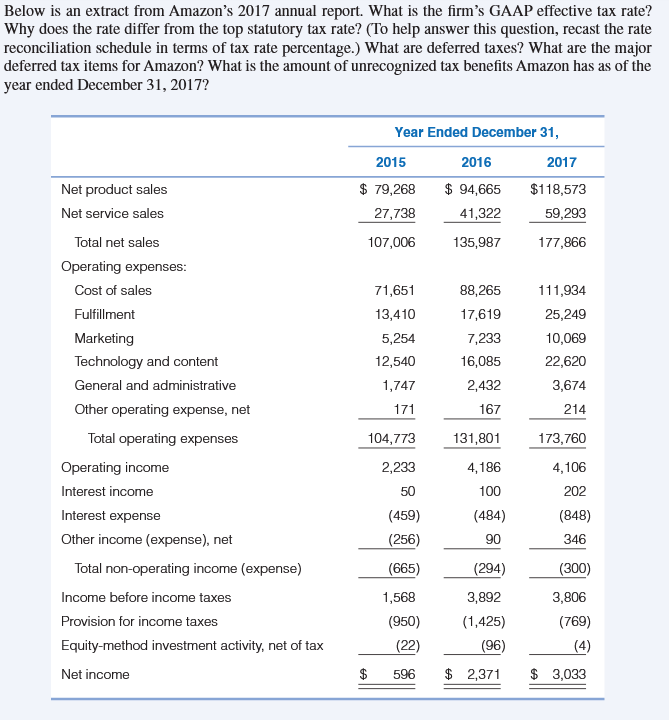

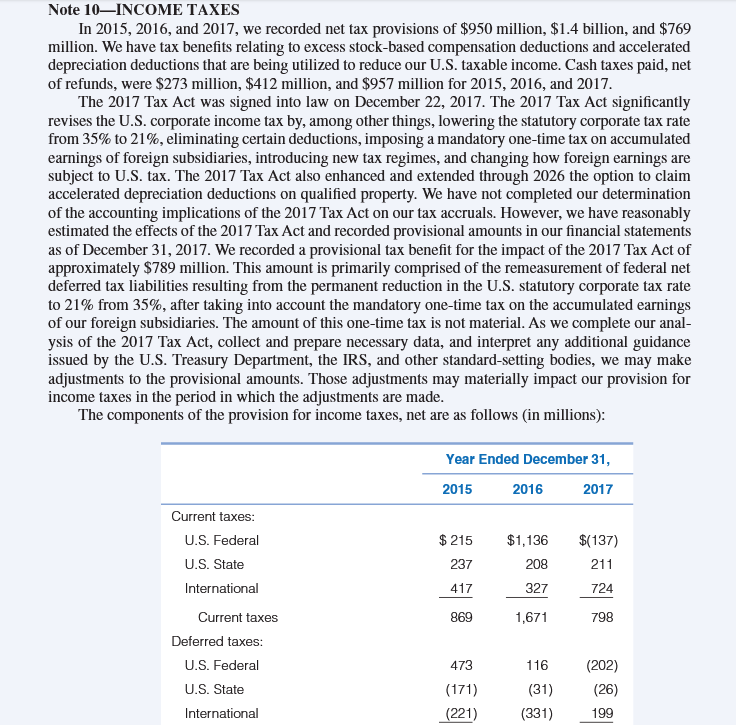

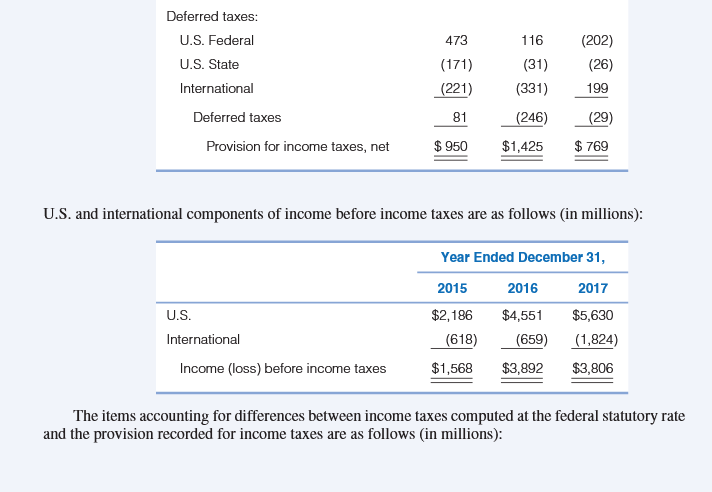

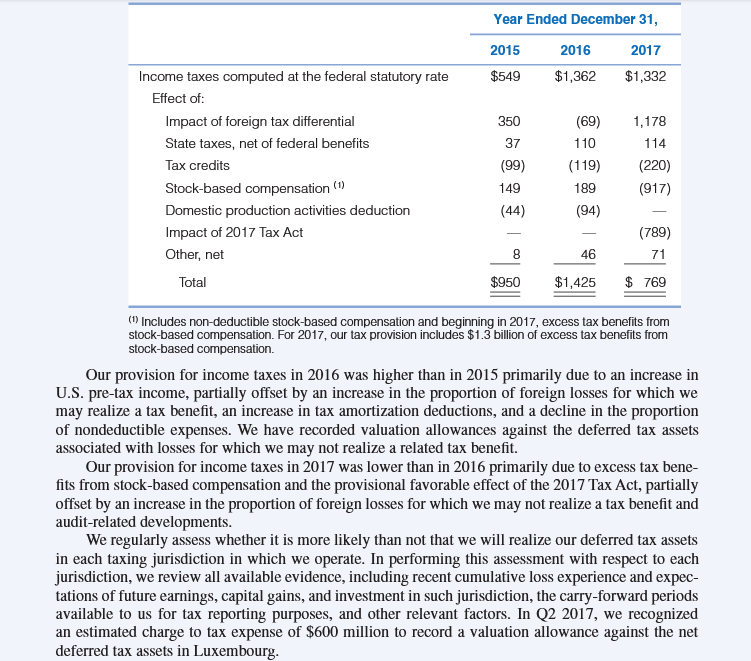

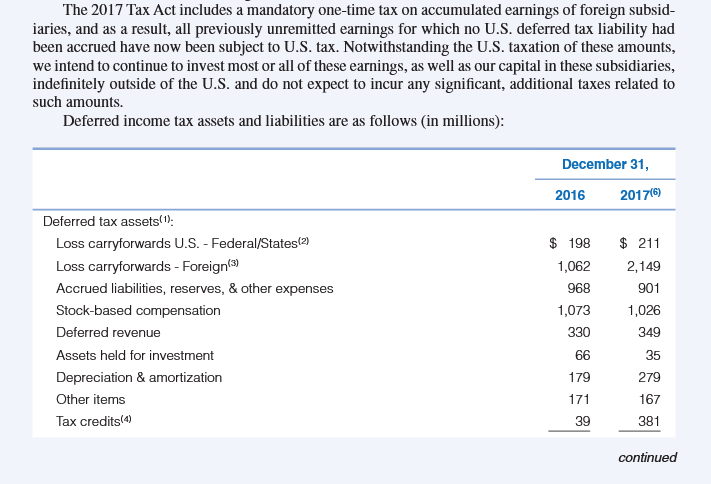

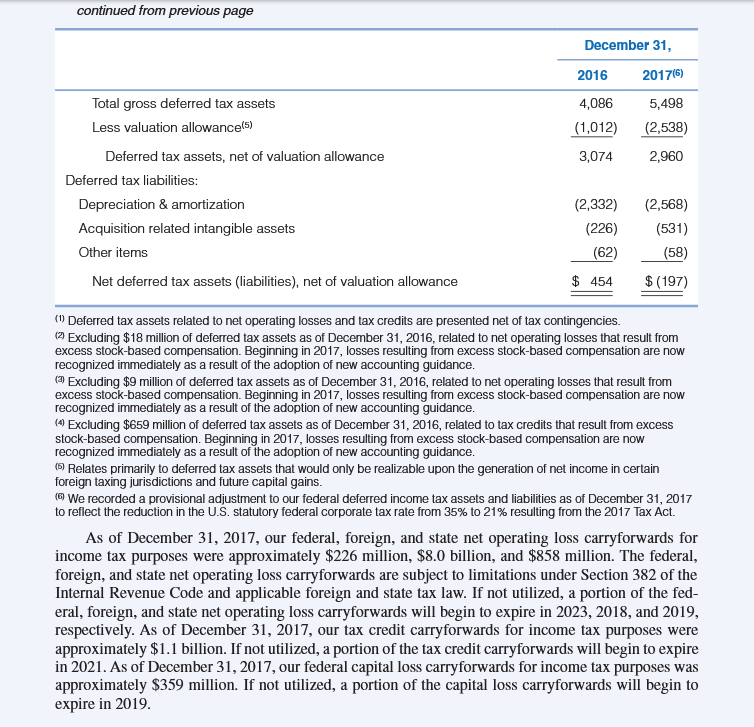

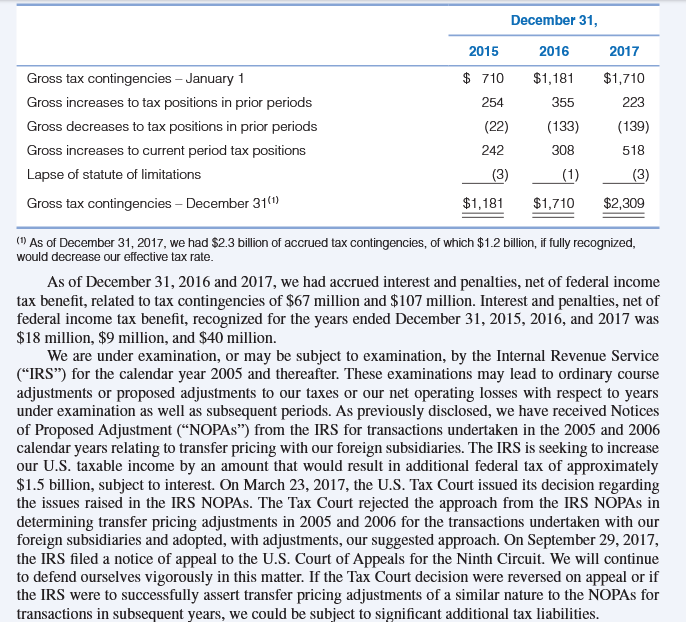

Below is an extract from Amazon's 2017 annual report. What is the firm's GAAP effective tax rate? Why does the rate differ from the top statutory tax rate? (To help answer this question, recast the rate reconciliation schedule in terms of tax rate percentage.) What are deferred taxes? What are the major deferred tax items for Amazon? What is the amount of unrecognized tax benefits Amazon has as of the year ended December 31, 2017? Year Ended December 31, 2016 Net product sales $ 94,665 Net service sales 41,322 Total net sales 135,987 Operating expenses: Cost of sales 88,265 Fulfillment 17,619 Marketing 7,233 Technology and content 16,085 General and administrative 2,432 Other operating expense, net 167 Total operating expenses 131,801 Operating income 4,186 Interest income 100 Interest expense (484) Other income (expense), net 90 Total non-operating income (expense) (294) Income before income taxes Provision for income taxes Equity-method investment activity, net of tax Net income 2015 $ 79,268 27,738 107,006 71,651 13,410 5,254 12,540 1,747 171 104,773 2,233 50 (459) (256) (665) 1,568 (950) (22) 596 3,892 (1,425) (96) $2,371 2017 $118,573 59,293 177,866 111,934 25,249 10,069 22,620 3,674 214 173,760 4,106 202 (848) 346 (300) 3,806 (769) (4) $ 3,033 Note 10-INCOME TAXES In 2015, 2016, and 2017, we recorded net tax provisions of $950 million, $1.4 billion, and $769 million. We have tax benefits relating to excess stock-based compensation deductions and accelerated depreciation deductions that are being utilized to reduce our U.S. taxable income. Cash taxes paid, net of refunds, were $273 million, $412 million, and $957 million for 2015, 2016, and 2017. The 2017 Tax Act was signed into law on December 22, 2017. The 2017 Tax Act significantly revises the U.S. corporate income tax by, among other things, lowering the statutory corporate tax rate from 35% to 21%, eliminating certain deductions, imposing a mandatory one-time tax on accumulated earnings of foreign subsidiaries, introducing new tax regimes, and changing how foreign earnings are subject to U.S. tax. The 2017 Tax Act also enhanced and extended through 2026 the option to claim accelerated depreciation deductions on qualified property. We have not completed our determination of the accounting implications of the 2017 Tax Act on our tax accruals. However, we have reasonably estimated the effects of the 2017 Tax Act and recorded provisional amounts in our financial statements as of December 31, 2017. We recorded a provisional tax benefit for the impact of the 2017 Tax Act of approximately $789 million. This amount is primarily comprised of the remeasurement of federal net deferred tax liabilities resulting from the permanent reduction in the U.S. statutory corporate tax rate to 21% from 35%, after taking into account the mandatory one-time tax on the accumulated earnings of our foreign subsidiaries. The amount of this one-time tax is not material. As we complete our anal- ysis of the 2017 Tax Act, collect and prepare necessary data, and interpret any additional guidance issued by the U.S. Treasury Department, the IRS, and other standard-setting bodies, we may make adjustments to the provisional amounts. Those adjustments may materially impact our provision for income taxes in the period in which the adjustments are made. The components of the provision for income taxes, net are as follows (in millions): Year Ended December 31, 2015 2016 2017 Current taxes: U.S. Federal $ 215 $1,136 $(137) U.S. State 237 208 211 International 417 327 724 869 1,671 798 473 116 (202) (171) (31) (26) (221) (331) 199 Current taxes Deferred taxes: U.S. Federal U.S. State International Deferred taxes: U.S. Federal U.S. State International 473 116 (202) (171) (31) (26) (221) (331) 199 Deferred taxes 81 (246) (29) Provision for income taxes, net $ 950 $1,425 $ 769 U.S. and international components of income before income taxes are as follows (in millions): Year Ended December 31, 2015 2016 2017 U.S. $2,186 $4,551 $5,630 International (618) (1,824) Income (loss) before income taxes $1,568 $3,892 $3,806 The items accounting for differences between income taxes computed at the federal statutory rate and the provision recorded for income taxes are as follows (in millions): (659) Year Ended December 31, 2015 2016 2017 Income taxes computed at the federal statutory rate $549 $1,362 $1,332 Effect of: Impact of foreign tax differential 350 (69) 1,178 37 110 114 State taxes, net of federal benefits Tax credits (99) (119) (220) Stock-based compensation (1) 149 189 (917) (44) (94) Domestic production activities deduction Impact of 2017 Tax Act (789) Other, net 8 46 71 Total $950 $1,425 $ 769 (1) Includes non-deductible stock-based compensation and beginning in 2017, excess tax benefits from stock-based compensation. For 2017, our tax provision includes $1.3 billion of excess tax benefits from stock-based compensation. Our provision for income taxes in 2016 was higher than in 2015 primarily due to an increase in U.S. pre-tax income, partially offset by an increase in the proportion of foreign losses for which we may realize a tax benefit, an increase in tax amortization deductions, and a decline in the proportion of nondeductible expenses. We have recorded valuation allowances against the deferred tax assets associated with losses for which we may not realize a related tax benefit. Our provision for income taxes in 2017 was lower than in 2016 primarily due to excess tax bene- fits from stock-based compensation and the provisional favorable effect of the 2017 Tax Act, partially offset by an increase in the proportion of foreign losses for which we may not realize a tax benefit and audit-related developments. We regularly assess whether it is more likely than not that we will realize our deferred tax assets in each taxing jurisdiction in which we operate. In performing this assessment with respect to each jurisdiction, we review all available evidence, including recent cumulative loss experience and expec- tations of future earnings, capital gains, and investment in such jurisdiction, the carry-forward periods available to us for tax reporting purposes, and other relevant factors. In Q2 2017, we recognized an estimated charge to tax expense of $600 million to record a valuation allowance against the net deferred tax assets in Luxembourg. The 2017 Tax Act includes a mandatory one-time tax on accumulated earnings of foreign subsid- iaries, and as a result, all previously unremitted earnings for which no U.S. deferred tax liability had been accrued have now been subject to U.S. tax. Notwithstanding the U.S. taxation of these amounts, we intend to continue to invest most or all of these earnings, as well as our capital in these subsidiaries, indefinitely outside of the U.S. and do not expect to incur any significant, additional taxes related to such amounts. Deferred income tax assets and liabilities are as follows (in millions): December 31, 2016 Deferred tax assets(1); Loss carryforwards U.S. - Federal/States(2) $ 198 Loss carryforwards - Foreign (3) 1,062 Accrued liabilities, reserves, & other expenses 968 Stock-based compensation 1,073 Deferred revenue 330 Assets held for investment 66 179 Depreciation & amortization Other items 171 Tax credits(4) 39 2017 (6) $211 2,149 901 1,026 349 35 279 167 381 continued continued from previous page December 31, 2016 2017 (6) Total gross deferred tax assets 4,086 5,498 Less valuation allowance(5) (1,012) (2,538) Deferred tax assets, net of valuation allowance 3,074 2,960 Deferred tax liabilities: Depreciation & amortization (2,332) (2,568) Acquisition related intangible assets (226) (531) Other items (62) (58) Net deferred tax assets (liabilities), net of valuation allowance $ 454 $ (197) (1) Deferred tax assets related to net operating losses and tax credits are presented net of tax contingencies. (2) Excluding $18 million of deferred tax assets as of December 31, 2016, related to net operating losses that result from excess stock-based compensation. Beginning in 2017, losses resulting from excess stock-based compensation are now recognized immediately as a result of the adoption of new accounting guidance. (3) Excluding $9 million of deferred tax assets as of December 31, 2016, related to net operating losses that result from excess stock-based compensation. Beginning in 2017, losses resulting from excess stock-based compensation are now recognized immediately as a result of the adoption of new accounting guidance. (4) Excluding $659 million of deferred tax assets as of December 31, 2016, related to tax credits that result from excess stock-based compensation. Beginning in 2017, losses resulting from excess stock-based compensation are now recognized immediately as a result of the adoption of new accounting guidance. (5) Relates primarily to deferred tax assets that would only be realizable upon the generation of net income in certain foreign taxing jurisdictions and future capital gains. (6) We recorded a provisional adjustment to our federal deferred income tax assets and liabilities as of December 31, 2017 to reflect the reduction in the U.S. statutory federal corporate tax rate from 35% to 21% resulting from the 2017 Tax Act. As of December 31, 2017, our federal, foreign, and state net operating loss carryforwards for income tax purposes were approximately $226 million, $8.0 billion, and $858 million. The federal, foreign, and state net operating loss carryforwards are subject to limitations under Section 382 of the Internal Revenue Code and applicable foreign and state tax law. If not utilized, a portion of the fed- eral, foreign, and state net operating loss carryforwards will begin to expire in 2023, 2018, and 2019, respectively. As of December 31, 2017, our tax credit carryforwards for income tax purposes were approximately $1.1 billion. If not utilized, a portion of the tax credit carryforwards will begin to expire in 2021. As of December 31, 2017, our federal capital loss carryforwards for income tax purposes was approximately $359 million. If not utilized, a portion of the capital loss carryforwards will begin to expire in 2019. Tax Contingencies We are subject to income taxes in the U.S. (federal and state) and numerous foreign jurisdictions. Significant judgment is required in evaluating our tax positions and determining our provision for income taxes. During the ordinary course of business, there are many transactions and calculations for which the ultimate tax determination is uncertain. We establish reserves for tax-related uncertainties based on estimates of whether, and the extent to which, additional taxes will be due. These reserves are established when we believe that certain positions might be challenged despite our belief that our tax return positions are fully supportable. We adjust these reserves in light of changing facts and cir- cumstances, such as the outcome of tax audits. The provision for income taxes includes the impact of reserve provisions and changes to reserves that are considered appropriate. The reconciliation of our tax contingencies is as follows (in millions): 2015 $ 710 254 (22) 242 December 31, 2016 $1,181 355 (133) 308 2017 $1,710 223 (139) 518 Gross tax contingencies - January 1 Gross increases to tax positions in prior periods Gross decreases to tax positions in prior periods Gross increases to current period tax positions Lapse of statute of limitations (3) (1) Gross tax contingencies - December 31(1) $1,181 $1,710 $2,309 (1) As of December 31, 2017, we had $2.3 billion of accrued tax contingencies, of which $1.2 billion, if fully recognized, would decrease our effective tax rate. As of December 31, 2016 and 2017, we had accrued interest and penalties, net of federal income tax benefit, related to tax contingencies of $67 million and $107 million. Interest and penalties, net of federal income tax benefit, recognized for the years ended December 31, 2015, 2016, and 2017 was $18 million, $9 million, and $40 million. We are under examination, or may be subject to examination, by the Internal Revenue Service ("IRS") for the calendar year 2005 and thereafter. These examinations may lead to ordinary course adjustments or proposed adjustments to our taxes or our net operating losses with respect to years under examination as well as subsequent periods. As previously disclosed, we have received Notices of Proposed Adjustment ("NOPAs") from the IRS for transactions undertaken in the 2005 and 2006 calendar years relating to transfer pricing with our foreign subsidiaries. The IRS is seeking to increase our U.S. taxable income by an amount that would result in additional federal tax of approximately $1.5 billion, subject to interest. On March 23, 2017, the U.S. Tax Court issued its decision regarding the issues raised in the IRS NOPAS. The Tax Court rejected the approach from the IRS NOPAS in determining transfer pricing adjustments in 2005 and 2006 for the transactions undertaken with our foreign subsidiaries and adopted, with adjustments, our suggested approach. On September 29, 2017, the IRS filed a notice of appeal to the U.S. Court of Appeals for the Ninth Circuit. We will continue to defend ourselves vigorously in this matter. If the Tax Court decision were reversed on appeal or if the IRS were to successfully assert transfer pricing adjustments of a similar nature to the NOPAS for transactions in subsequent years, we could be subject to significant additional tax liabilities. (3) Certain of our subsidiaries were under examination or investigation by the French Tax Adminis- tration ("FTA") for calendar year 2006 and thereafter. In September 2012, we received proposed tax assessment notices for calendar years 2006 through 2010 relating to the allocation of income between foreign jurisdictions. In June 2015, we received final tax collection notices for these years assessing additional French taxes, interest, and penalties through September 2012. In December 2017, we set- tled this dispute with the FTA and included the impact thereof within our financial statements. In addi- tion, in October 2014, the European Commission opened a formal investigation to examine whether decisions by the tax authorities in Luxembourg with regard to the corporate income tax paid by certain of our subsidiaries comply with European Union rules on state aid. On October 4, 2017, the European Commission announced its decision that determinations by the tax authorities in Luxembourg did not comply with European Union rules on state aid. This decision orders Luxembourg to calculate and recover additional taxes from us for the period May 2006 through June 2014. We believe this decision to be without merit and will consider our legal options, including an appeal. In December 2017, Lux- embourg appealed the European Commission's decision. While the European Commission announced an estimated recovery amount of approximately 250 million, plus interest, the actual amount of addi- tional taxes subject to recovery is to be calculated by the Luxembourg tax authorities in accordance with the European Commission's guidance. Once the recovery amount is computed by Luxembourg, we anticipate funding it, including interest, into escrow, where it will remain pending conclusion of all appeals. We may be required to fund into escrow an amount in excess of the estimated recovery amount announced by the European Commission. We are also subject to taxation in various states and other foreign jurisdictions including Canada, China, Germany, India, Japan, Luxembourg, and the United Kingdom. We are under, or may be subject to, audit or examination and additional assessments by the relevant authorities in respect of these particular jurisdictions primarily for 2008 and thereafter. We expect the total amount of tax contingencies will grow in 2018. In addition, changes in state, federal, and foreign tax laws may increase our tax contingencies. The timing of the resolution of income tax examinations is highly uncertain, and the amounts ultimately paid, if any, upon resolution of the issues raised by the taxing authorities may differ from the amounts accrued. It is reasonably possible that within the next 12 months we will receive additional assessments by various tax author- ities or possibly reach resolution of income tax examinations in one or more jurisdictions. These assessments or settlements could result in changes to our contingencies related to positions on tax filings in years through 2017. The actual amount of any change could vary significantly depending on the ultimate timing and nature of any settlements. We cannot currently provide an estimate of the range of possible outcomes. Below is an extract from Amazon's 2017 annual report. What is the firm's GAAP effective tax rate? Why does the rate differ from the top statutory tax rate? (To help answer this question, recast the rate reconciliation schedule in terms of tax rate percentage.) What are deferred taxes? What are the major deferred tax items for Amazon? What is the amount of unrecognized tax benefits Amazon has as of the year ended December 31, 2017? Year Ended December 31, 2016 Net product sales $ 94,665 Net service sales 41,322 Total net sales 135,987 Operating expenses: Cost of sales 88,265 Fulfillment 17,619 Marketing 7,233 Technology and content 16,085 General and administrative 2,432 Other operating expense, net 167 Total operating expenses 131,801 Operating income 4,186 Interest income 100 Interest expense (484) Other income (expense), net 90 Total non-operating income (expense) (294) Income before income taxes Provision for income taxes Equity-method investment activity, net of tax Net income 2015 $ 79,268 27,738 107,006 71,651 13,410 5,254 12,540 1,747 171 104,773 2,233 50 (459) (256) (665) 1,568 (950) (22) 596 3,892 (1,425) (96) $2,371 2017 $118,573 59,293 177,866 111,934 25,249 10,069 22,620 3,674 214 173,760 4,106 202 (848) 346 (300) 3,806 (769) (4) $ 3,033 Note 10-INCOME TAXES In 2015, 2016, and 2017, we recorded net tax provisions of $950 million, $1.4 billion, and $769 million. We have tax benefits relating to excess stock-based compensation deductions and accelerated depreciation deductions that are being utilized to reduce our U.S. taxable income. Cash taxes paid, net of refunds, were $273 million, $412 million, and $957 million for 2015, 2016, and 2017. The 2017 Tax Act was signed into law on December 22, 2017. The 2017 Tax Act significantly revises the U.S. corporate income tax by, among other things, lowering the statutory corporate tax rate from 35% to 21%, eliminating certain deductions, imposing a mandatory one-time tax on accumulated earnings of foreign subsidiaries, introducing new tax regimes, and changing how foreign earnings are subject to U.S. tax. The 2017 Tax Act also enhanced and extended through 2026 the option to claim accelerated depreciation deductions on qualified property. We have not completed our determination of the accounting implications of the 2017 Tax Act on our tax accruals. However, we have reasonably estimated the effects of the 2017 Tax Act and recorded provisional amounts in our financial statements as of December 31, 2017. We recorded a provisional tax benefit for the impact of the 2017 Tax Act of approximately $789 million. This amount is primarily comprised of the remeasurement of federal net deferred tax liabilities resulting from the permanent reduction in the U.S. statutory corporate tax rate to 21% from 35%, after taking into account the mandatory one-time tax on the accumulated earnings of our foreign subsidiaries. The amount of this one-time tax is not material. As we complete our anal- ysis of the 2017 Tax Act, collect and prepare necessary data, and interpret any additional guidance issued by the U.S. Treasury Department, the IRS, and other standard-setting bodies, we may make adjustments to the provisional amounts. Those adjustments may materially impact our provision for income taxes in the period in which the adjustments are made. The components of the provision for income taxes, net are as follows (in millions): Year Ended December 31, 2015 2016 2017 Current taxes: U.S. Federal $ 215 $1,136 $(137) U.S. State 237 208 211 International 417 327 724 869 1,671 798 473 116 (202) (171) (31) (26) (221) (331) 199 Current taxes Deferred taxes: U.S. Federal U.S. State International Deferred taxes: U.S. Federal U.S. State International 473 116 (202) (171) (31) (26) (221) (331) 199 Deferred taxes 81 (246) (29) Provision for income taxes, net $ 950 $1,425 $ 769 U.S. and international components of income before income taxes are as follows (in millions): Year Ended December 31, 2015 2016 2017 U.S. $2,186 $4,551 $5,630 International (618) (1,824) Income (loss) before income taxes $1,568 $3,892 $3,806 The items accounting for differences between income taxes computed at the federal statutory rate and the provision recorded for income taxes are as follows (in millions): (659) Year Ended December 31, 2015 2016 2017 Income taxes computed at the federal statutory rate $549 $1,362 $1,332 Effect of: Impact of foreign tax differential 350 (69) 1,178 37 110 114 State taxes, net of federal benefits Tax credits (99) (119) (220) Stock-based compensation (1) 149 189 (917) (44) (94) Domestic production activities deduction Impact of 2017 Tax Act (789) Other, net 8 46 71 Total $950 $1,425 $ 769 (1) Includes non-deductible stock-based compensation and beginning in 2017, excess tax benefits from stock-based compensation. For 2017, our tax provision includes $1.3 billion of excess tax benefits from stock-based compensation. Our provision for income taxes in 2016 was higher than in 2015 primarily due to an increase in U.S. pre-tax income, partially offset by an increase in the proportion of foreign losses for which we may realize a tax benefit, an increase in tax amortization deductions, and a decline in the proportion of nondeductible expenses. We have recorded valuation allowances against the deferred tax assets associated with losses for which we may not realize a related tax benefit. Our provision for income taxes in 2017 was lower than in 2016 primarily due to excess tax bene- fits from stock-based compensation and the provisional favorable effect of the 2017 Tax Act, partially offset by an increase in the proportion of foreign losses for which we may not realize a tax benefit and audit-related developments. We regularly assess whether it is more likely than not that we will realize our deferred tax assets in each taxing jurisdiction in which we operate. In performing this assessment with respect to each jurisdiction, we review all available evidence, including recent cumulative loss experience and expec- tations of future earnings, capital gains, and investment in such jurisdiction, the carry-forward periods available to us for tax reporting purposes, and other relevant factors. In Q2 2017, we recognized an estimated charge to tax expense of $600 million to record a valuation allowance against the net deferred tax assets in Luxembourg. The 2017 Tax Act includes a mandatory one-time tax on accumulated earnings of foreign subsid- iaries, and as a result, all previously unremitted earnings for which no U.S. deferred tax liability had been accrued have now been subject to U.S. tax. Notwithstanding the U.S. taxation of these amounts, we intend to continue to invest most or all of these earnings, as well as our capital in these subsidiaries, indefinitely outside of the U.S. and do not expect to incur any significant, additional taxes related to such amounts. Deferred income tax assets and liabilities are as follows (in millions): December 31, 2016 Deferred tax assets(1); Loss carryforwards U.S. - Federal/States(2) $ 198 Loss carryforwards - Foreign (3) 1,062 Accrued liabilities, reserves, & other expenses 968 Stock-based compensation 1,073 Deferred revenue 330 Assets held for investment 66 179 Depreciation & amortization Other items 171 Tax credits(4) 39 2017 (6) $211 2,149 901 1,026 349 35 279 167 381 continued continued from previous page December 31, 2016 2017 (6) Total gross deferred tax assets 4,086 5,498 Less valuation allowance(5) (1,012) (2,538) Deferred tax assets, net of valuation allowance 3,074 2,960 Deferred tax liabilities: Depreciation & amortization (2,332) (2,568) Acquisition related intangible assets (226) (531) Other items (62) (58) Net deferred tax assets (liabilities), net of valuation allowance $ 454 $ (197) (1) Deferred tax assets related to net operating losses and tax credits are presented net of tax contingencies. (2) Excluding $18 million of deferred tax assets as of December 31, 2016, related to net operating losses that result from excess stock-based compensation. Beginning in 2017, losses resulting from excess stock-based compensation are now recognized immediately as a result of the adoption of new accounting guidance. (3) Excluding $9 million of deferred tax assets as of December 31, 2016, related to net operating losses that result from excess stock-based compensation. Beginning in 2017, losses resulting from excess stock-based compensation are now recognized immediately as a result of the adoption of new accounting guidance. (4) Excluding $659 million of deferred tax assets as of December 31, 2016, related to tax credits that result from excess stock-based compensation. Beginning in 2017, losses resulting from excess stock-based compensation are now recognized immediately as a result of the adoption of new accounting guidance. (5) Relates primarily to deferred tax assets that would only be realizable upon the generation of net income in certain foreign taxing jurisdictions and future capital gains. (6) We recorded a provisional adjustment to our federal deferred income tax assets and liabilities as of December 31, 2017 to reflect the reduction in the U.S. statutory federal corporate tax rate from 35% to 21% resulting from the 2017 Tax Act. As of December 31, 2017, our federal, foreign, and state net operating loss carryforwards for income tax purposes were approximately $226 million, $8.0 billion, and $858 million. The federal, foreign, and state net operating loss carryforwards are subject to limitations under Section 382 of the Internal Revenue Code and applicable foreign and state tax law. If not utilized, a portion of the fed- eral, foreign, and state net operating loss carryforwards will begin to expire in 2023, 2018, and 2019, respectively. As of December 31, 2017, our tax credit carryforwards for income tax purposes were approximately $1.1 billion. If not utilized, a portion of the tax credit carryforwards will begin to expire in 2021. As of December 31, 2017, our federal capital loss carryforwards for income tax purposes was approximately $359 million. If not utilized, a portion of the capital loss carryforwards will begin to expire in 2019. Tax Contingencies We are subject to income taxes in the U.S. (federal and state) and numerous foreign jurisdictions. Significant judgment is required in evaluating our tax positions and determining our provision for income taxes. During the ordinary course of business, there are many transactions and calculations for which the ultimate tax determination is uncertain. We establish reserves for tax-related uncertainties based on estimates of whether, and the extent to which, additional taxes will be due. These reserves are established when we believe that certain positions might be challenged despite our belief that our tax return positions are fully supportable. We adjust these reserves in light of changing facts and cir- cumstances, such as the outcome of tax audits. The provision for income taxes includes the impact of reserve provisions and changes to reserves that are considered appropriate. The reconciliation of our tax contingencies is as follows (in millions): 2015 $ 710 254 (22) 242 December 31, 2016 $1,181 355 (133) 308 2017 $1,710 223 (139) 518 Gross tax contingencies - January 1 Gross increases to tax positions in prior periods Gross decreases to tax positions in prior periods Gross increases to current period tax positions Lapse of statute of limitations (3) (1) Gross tax contingencies - December 31(1) $1,181 $1,710 $2,309 (1) As of December 31, 2017, we had $2.3 billion of accrued tax contingencies, of which $1.2 billion, if fully recognized, would decrease our effective tax rate. As of December 31, 2016 and 2017, we had accrued interest and penalties, net of federal income tax benefit, related to tax contingencies of $67 million and $107 million. Interest and penalties, net of federal income tax benefit, recognized for the years ended December 31, 2015, 2016, and 2017 was $18 million, $9 million, and $40 million. We are under examination, or may be subject to examination, by the Internal Revenue Service ("IRS") for the calendar year 2005 and thereafter. These examinations may lead to ordinary course adjustments or proposed adjustments to our taxes or our net operating losses with respect to years under examination as well as subsequent periods. As previously disclosed, we have received Notices of Proposed Adjustment ("NOPAs") from the IRS for transactions undertaken in the 2005 and 2006 calendar years relating to transfer pricing with our foreign subsidiaries. The IRS is seeking to increase our U.S. taxable income by an amount that would result in additional federal tax of approximately $1.5 billion, subject to interest. On March 23, 2017, the U.S. Tax Court issued its decision regarding the issues raised in the IRS NOPAS. The Tax Court rejected the approach from the IRS NOPAS in determining transfer pricing adjustments in 2005 and 2006 for the transactions undertaken with our foreign subsidiaries and adopted, with adjustments, our suggested approach. On September 29, 2017, the IRS filed a notice of appeal to the U.S. Court of Appeals for the Ninth Circuit. We will continue to defend ourselves vigorously in this matter. If the Tax Court decision were reversed on appeal or if the IRS were to successfully assert transfer pricing adjustments of a similar nature to the NOPAS for transactions in subsequent years, we could be subject to significant additional tax liabilities. (3) Certain of our subsidiaries were under examination or investigation by the French Tax Adminis- tration ("FTA") for calendar year 2006 and thereafter. In September 2012, we received proposed tax assessment notices for calendar years 2006 through 2010 relating to the allocation of income between foreign jurisdictions. In June 2015, we received final tax collection notices for these years assessing additional French taxes, interest, and penalties through September 2012. In December 2017, we set- tled this dispute with the FTA and included the impact thereof within our financial statements. In addi- tion, in October 2014, the European Commission opened a formal investigation to examine whether decisions by the tax authorities in Luxembourg with regard to the corporate income tax paid by certain of our subsidiaries comply with European Union rules on state aid. On October 4, 2017, the European Commission announced its decision that determinations by the tax authorities in Luxembourg did not comply with European Union rules on state aid. This decision orders Luxembourg to calculate and recover additional taxes from us for the period May 2006 through June 2014. We believe this decision to be without merit and will consider our legal options, including an appeal. In December 2017, Lux- embourg appealed the European Commission's decision. While the European Commission announced an estimated recovery amount of approximately 250 million, plus interest, the actual amount of addi- tional taxes subject to recovery is to be calculated by the Luxembourg tax authorities in accordance with the European Commission's guidance. Once the recovery amount is computed by Luxembourg, we anticipate funding it, including interest, into escrow, where it will remain pending conclusion of all appeals. We may be required to fund into escrow an amount in excess of the estimated recovery amount announced by the European Commission. We are also subject to taxation in various states and other foreign jurisdictions including Canada, China, Germany, India, Japan, Luxembourg, and the United Kingdom. We are under, or may be subject to, audit or examination and additional assessments by the relevant authorities in respect of these particular jurisdictions primarily for 2008 and thereafter. We expect the total amount of tax contingencies will grow in 2018. In addition, changes in state, federal, and foreign tax laws may increase our tax contingencies. The timing of the resolution of income tax examinations is highly uncertain, and the amounts ultimately paid, if any, upon resolution of the issues raised by the taxing authorities may differ from the amounts accrued. It is reasonably possible that within the next 12 months we will receive additional assessments by various tax author- ities or possibly reach resolution of income tax examinations in one or more jurisdictions. These assessments or settlements could result in changes to our contingencies related to positions on tax filings in years through 2017. The actual amount of any change could vary significantly depending on the ultimate timing and nature of any settlements. We cannot currently provide an estimate of the range of possible outcomes

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts