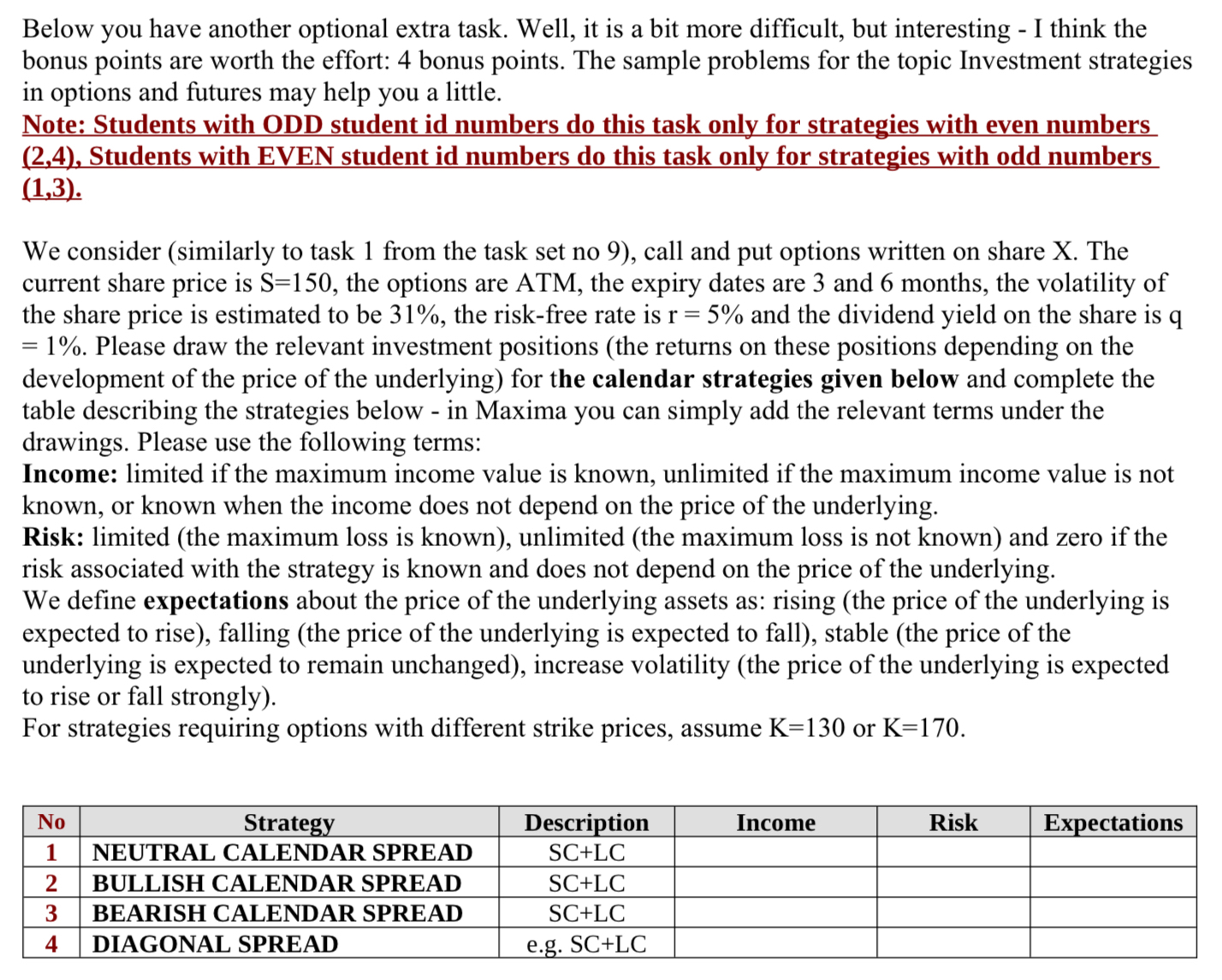

Question: Below you have another optional extra task. Well, it is a bit more difficult, but interesting - I think the bonus points are worth the

Below you have another optional extra task. Well, it is a bit more difficult, but interesting I think the bonus points are worth the effort: bonus points. The sample problems for the topic Investment strategies in options and futures may help you a little.

Note: Students with ODD student id numbers do this task only for strategies with even numbers Students with EVEN student id numbers do this task only for strategies with odd numbers

We consider similarly to task from the task set no call and put options written on share X The current share price is the options are ATM, the expiry dates are and months, the volatility of the share price is estimated to be the riskfree rate is and the dividend yield on the share is Please draw the relevant investment positions the returns on these positions depending on the development of the price of the underlying for the calendar strategies given below and complete the table describing the strategies below in Maxima you can simply add the relevant terms under the drawings. Please use the following terms:

Income: limited if the maximum income value is known, unlimited if the maximum income value is not known, or known when the income does not depend on the price of the underlying.

Risk: limited the maximum loss is known unlimited the maximum loss is not known and zero if the risk associated with the strategy is known and does not depend on the price of the underlying.

We define expectations about the price of the underlying assets as: rising the price of the underlying is expected to rise falling the price of the underlying is expected to fall stable the price of the underlying is expected to remain unchanged increase volatility the price of the underlying is expected to rise or fall strongly

For strategies requiring options with different strike prices, assume or

tableNoStrategy,Description,Income,Risk,ExpectationsNEUTRAL CALENDAR SPREAD,SCLCBULLISH CALENDAR SPREAD,SCLCBEARISH CALENDAR SPREAD,SCLCDIAGONAL SPREAD,eg SCLC

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock