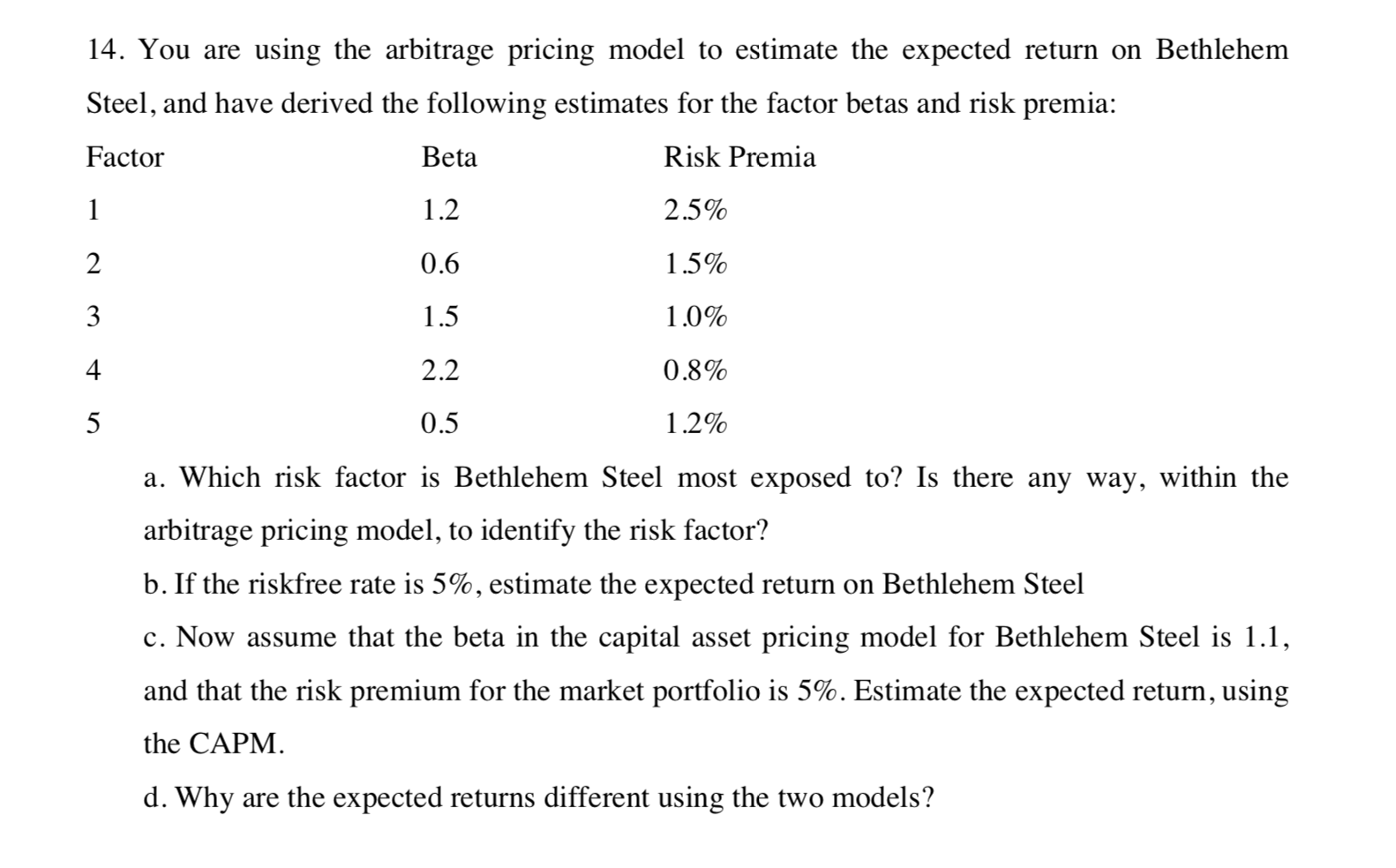

Question: Beta 1.2 14. You are using the arbitrage pricing model to estimate the expected return on Bethlehem Steel, and have derived the following estimates for

Beta 1.2 14. You are using the arbitrage pricing model to estimate the expected return on Bethlehem Steel, and have derived the following estimates for the factor betas and risk premia: Factor Risk Premia 2.5% 0.6 1.5% 1.0% 0.8% 0.5 1.2% a. Which risk factor is Bethlehem Steel most exposed to? Is there any way, within the arbitrage pricing model, to identify the risk factor? b. If the riskfree rate is 5%, estimate the expected return on Bethlehem Steel c. Now assume that the beta in the capital asset pricing model for Bethlehem Steel is 1.1, and that the risk premium for the market portfolio is 5%. Estimate the expected return, using the CAPM. d. Why are the expected returns different using the two models? Beta 1.2 14. You are using the arbitrage pricing model to estimate the expected return on Bethlehem Steel, and have derived the following estimates for the factor betas and risk premia: Factor Risk Premia 2.5% 0.6 1.5% 1.0% 0.8% 0.5 1.2% a. Which risk factor is Bethlehem Steel most exposed to? Is there any way, within the arbitrage pricing model, to identify the risk factor? b. If the riskfree rate is 5%, estimate the expected return on Bethlehem Steel c. Now assume that the beta in the capital asset pricing model for Bethlehem Steel is 1.1, and that the risk premium for the market portfolio is 5%. Estimate the expected return, using the CAPM. d. Why are the expected returns different using the two models

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts